Portuguese

Portuguese  English

English  Spanish

Spanish

The Simple Step That Can Save Your Finances in Critical Moments. Emergency Savings Are Your Main Ally to Face Unemployment, Unforeseen Circumstances, and Avoid Expensive Debts

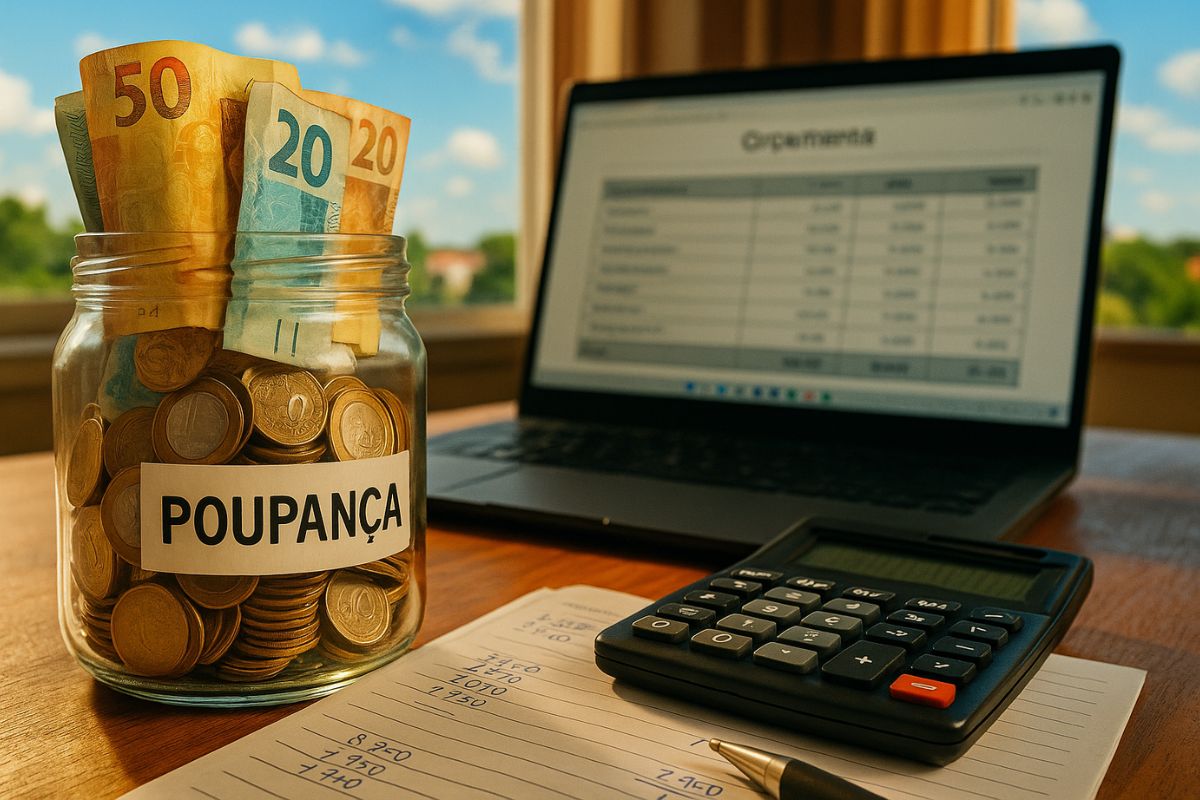

Maintaining a financial reserve is not just a good practice, but a necessity for anyone looking for stability. Having a fund prepared to save your finances in critical moments can mean the difference between navigating a period of instability with ease or falling into debt. Experts point out that a well-structured emergency fund provides security to cover essential expenses in situations such as job loss, health issues, or urgent repairs.

Despite its importance, many people do not know how to start building this financial protection. The process requires planning, discipline, and attention to details that ensure the money is available when truly needed, preserving the capital and avoiding unnecessary risks.

What Is an Emergency Fund and Why Have One

An emergency fund is an amount saved exclusively for unforeseen events. It acts as insurance against situations that can destabilize your budget, such as unexpected medical expenses or job loss.

-

The government requests the Federal Revenue Service for a new system to automate the income tax declaration, reducing errors, time, and bureaucracy for millions of Brazilians.

-

Pix in installments, international Pix, and contactless payment without internet: the Central Bank revealed the new features coming to the tool that is already used by almost every adult in Brazil.

-

Mercado Livre has just started selling medications with delivery in up to three hours to your door, and this move could completely change the way Brazilians buy medicines on a daily basis.

-

In Dubai, rising tensions from the war in the Middle East are causing super-rich individuals to leave the Gulf and direct their fortunes to a new financial refuge in Asia.

Without this resource, the solution is often to resort to expensive credit options, like credit cards and loans, which can further compromise financial health. Ideally, this amount should cover three to six months of essential expenses, providing time to reorganize life without immediate pressure.

How to Calculate the Ideal Amount for Your Fund

The first step is to understand how much it costs to maintain your basic standard of living per month. This includes housing, bills, food, transportation, and other essential expenses.

With this number in hand, multiply it by three, four, five, or six, depending on your desired level of security. Self-employed individuals or those with variable income should prioritize higher amounts, while stable workers can start with a smaller level.

Where to Keep Your Emergency Fund

The choice of where to keep this fund should prioritize liquidity, security, and capital preservation. Savings accounts, daily liquidity CDBs, and low-risk fixed income funds are the most recommended options.

Investments with long terms, volatility, or penalties for early withdrawal should be avoided. Remember: the goal is not to seek large profits, but to ensure that the money is quickly available in case of need.

Strategies to Start and Maintain the Fund

Starting is more important than waiting for the “ideal moment.” Set aside a fixed monthly amount, even if small, and treat it like a mandatory bill. Automating transfers at the beginning of the month helps create consistency.

Additionally, review the fund periodically. Adjust the amount according to changes in living costs and avoid spending the amount for reasons that are not truly emergencies. This discipline is what transforms a good intention into a solid resource for the future.

And you, have you already started building your emergency fund or are you still postponing it? What was the biggest challenge to save? Share your experience in the comments.

Seja o primeiro a reagir!