Portuguese

Portuguese  English

English  Spanish

Spanish

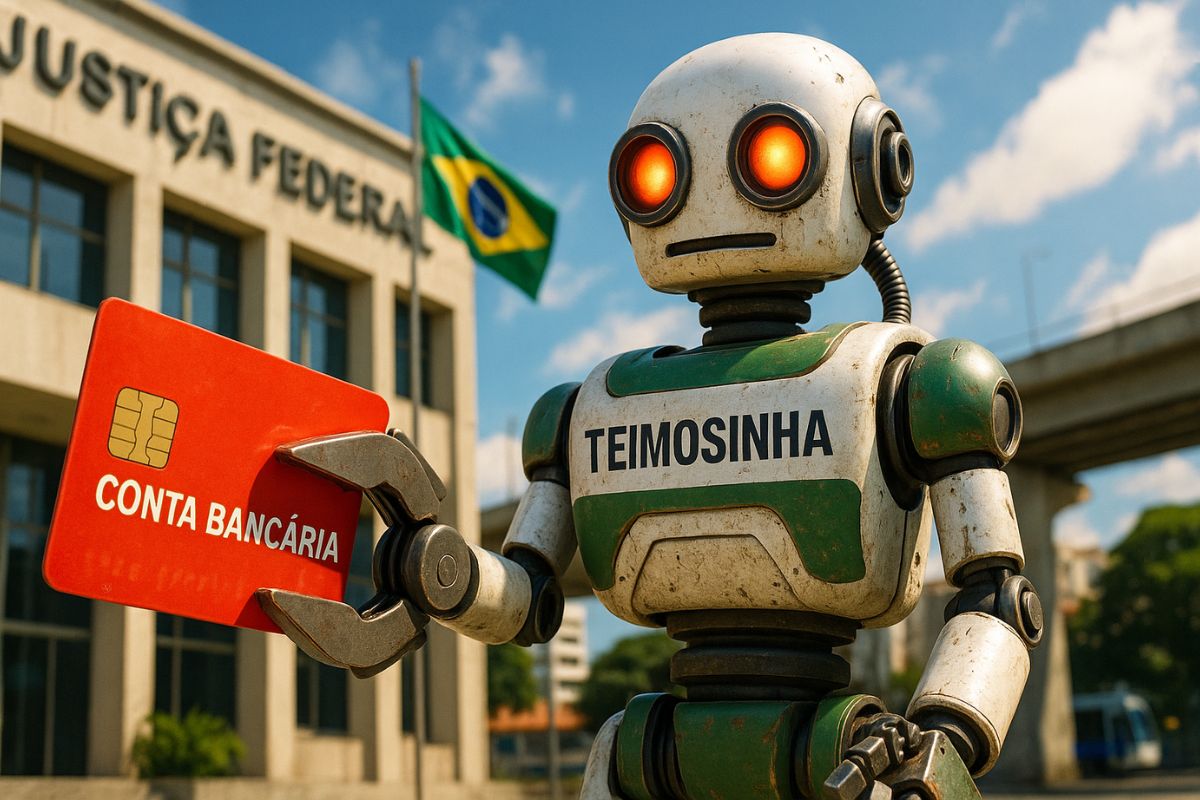

The Brazilian Judiciary Uses the Automated System “Teimosinha,” Which Searches and Blocks Amounts in Bank Accounts Daily for Up to 30 Days, Making Judicial Collection More Efficient and Hindering the Concealment of Assets by Debtors

The Brazilian Judiciary has incorporated automation technology in debt enforcement through the robot “Teimosinha,” a feature of the Asset Search System of the Judiciary (Sisbajud). The mechanism, approved and controlled by court order, repeats daily attempts to block amounts in a debtor’s accounts for up to 30 consecutive days, increasing the effectiveness of online garnishments.

Unlike the previous model, which only conducted a one-time search, “Teimosinha” maintains continuous surveillance over bank accounts. With each new credit received, the system automatically identifies and blocks the amount, until it reaches the total debt determined in the judicial process.

How “Teimosinha” Works in Practice

The operation of “Teimosinha” is simple but highly strategic.

-

Larger than entire cities in Brazil: BYD is building a 4.6 km² complex in Bahia with a capacity for 600,000 vehicles per year, but the discovery of 163 workers in conditions analogous to slavery has shaken the entire project.

-

With an investment of R$ 612 million, a capacity to process 1.2 million liters of milk per day, Piracanjuba inaugurates a mega cheese factory that increases national production, reduces dependence on imports, and repositions Brazil on the global dairy map.

-

Brazilian city gains industrial hub for 85 companies that is equivalent to 55 football fields.

-

Peugeot and Citroën factory in Argentina cuts production by half and opens a layoff program for more than 2,000 employees after Brazil drastically reduced purchases of Argentine vehicles.

After the creditor’s request and the judge’s authorization, Sisbajud initiates an automated routine to search for financial assets linked to the debtor’s CPF or CNPJ.

For 30 days, the system checks daily the current accounts, savings, and investments of the debtor in all financial institutions in the country.

If it detects available balance, it blocks the amount and transfers it to a judicial account.

The process is confidential, and the debtor is not notified in advance, precisely to prevent them from withdrawing or concealing the resources.

Practical Examples of Blocking with “Teimosinha”

In a common case of civil debt of R$ 10 thousand, for example, the first attempt to block may not find available balance.

Fifteen days later, the system detects the debtor’s salary payment, blocks R$ 5 thousand immediately, and continues monitoring until the total amount owed is reached.

The same mechanism is widely used in alimony actions, ensuring that the amount is retained as soon as the money enters the account.

In labor lawsuits against companies, the system may block part of the payments received from clients, ensuring that the worker receives the amount recognized by the Judiciary.

There are also situations where the debtor tries to move or withdraw amounts quickly.

However, “Teimosinha” works with short intervals of scanning, managing to intercept the deposit before the money is withdrawn.

Advantages of Using Judicial Automation

The main advantage is the efficiency in executing judicial decisions.

With the robot, the Judiciary reduces the time between the ruling and the enforcement of the payment order.

Previously, each attempt to block required a new order from the judge, which delayed the process.

The system also saves time and resources, eliminates bureaucracy, and increases the success rate of garnishments.

Another important feature is the surprise effect, essential for preventing financial maneuvers.

According to recent decisions, “Teimosinha” does not violate banking secrecy rights, as it depends on judicial authorization and follows the legal parameters of the National Justice Council (CNJ).

Judicial Limits and Care

Despite its efficiency, the use of “Teimosinha” is limited to 30 days per cycle. After this period, the creditor needs to request new authorization to continue searches.

Moreover, amounts protected by law, such as salaries up to the minimum limit, savings below 40 minimum salaries, and food benefits, cannot be blocked.

There are also discussions about the use of the tool in cases of companies in judicial recovery, where automatic blocking might compromise the functioning of economic activity.

In these cases, case law recommends caution and individualized analysis.

What Changes for the Debtor and the Creditor

For the creditor, the system represents a leap in the effectiveness of judicial collection.

The chances of recovering amounts increase, and the execution time is significantly reduced.

For the debtor, the scenario requires greater attention and transparency, as financial transactions are under constant judicial surveillance.

Lawyers emphasize that the best way to avoid surprises is to seek agreements before the garnishment.

Once “Teimosinha” is activated, any credit received can be automatically blocked, including deposits from third parties or transfers between accounts.

A teimosinha foi inicialmente implementada pelo Banco do Brasil, no início dos anos 2000, para cobrar dívidas de clientes. Agora o processo se popularizou.

Parabéns ao Banco do Brasil pela invenção.

Existe também a raspadinha… 😂

Tb invenção do BB.👏👏👏