Portuguese

Portuguese  English

English  Spanish

Spanish

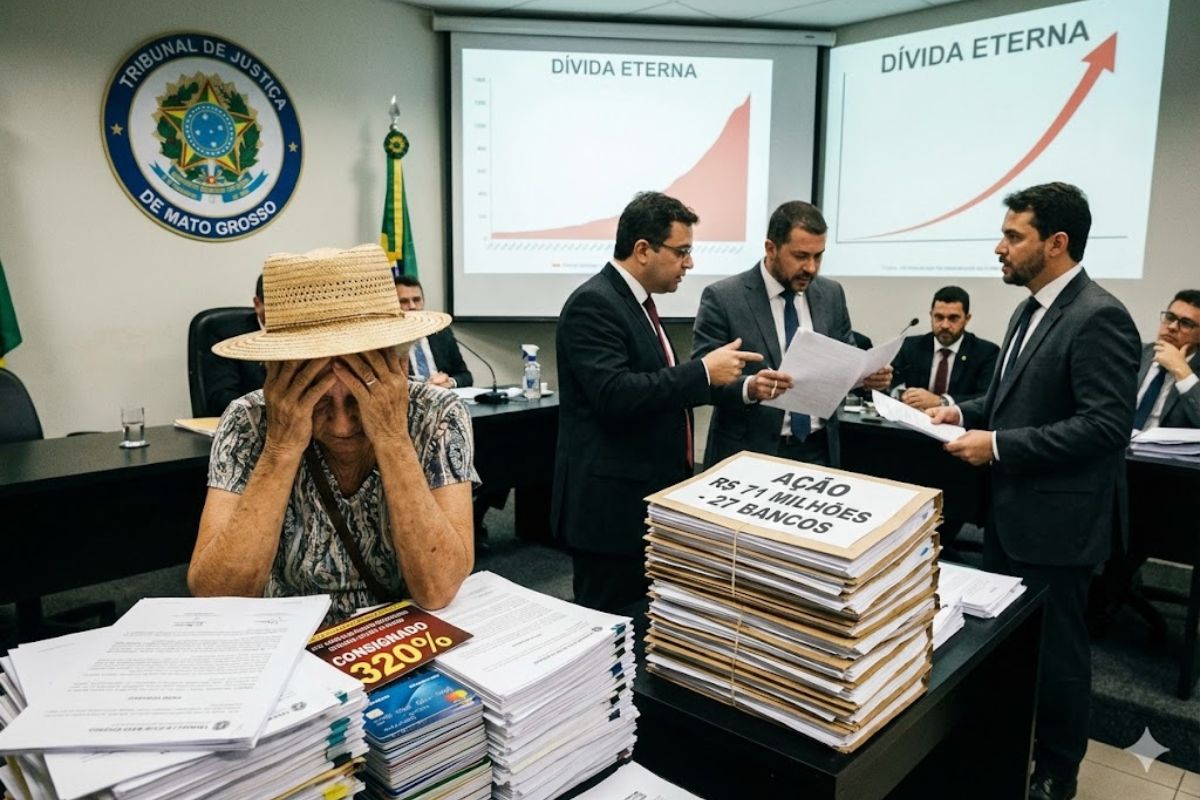

In Billion-Dollar Class Action, Consumers Association Claims 27 Banks Use Consigned Card to Expropriate Retirees’ Income in Mato Grosso, Encourage Over-Indebtedness with Permanent Rotating Credit, and Violate Basic Rights to Transparency, Contractual Balance, and Food Income Protection Nationwide According to the Entity.

The civil class action proposed by the Brazilian Association for the Defense of Clients and Consumers of Financial and Banking Operations (Abradeb), with a claim amount of R$ 71 million, directly targets the income of retirees and pensioners in Mato Grosso. According to the petition, the combination of consigned card, Consigned Margin Reserve (RMC), and Benefit Consigned Card (RCC) created a mechanism of continuous collection that empties pension benefits and salaries, under contracts signed on a large scale over the past few years, including operations carried out between 2015 and 2025.

The case, which is pending in the Specialized Court for Class Actions in Cuiabá, accuses 27 banks and financial institutions of structuring a model that, in practice, makes credit an almost inevitable path to over-indebtedness. Abradeb argues that the contractual engineering was designed to keep retirees and other vulnerable consumers trapped in the payment of charges, without any real prospect of fully settling their debts.

How the Action Describes the Scheme Against Retirees

According to Abradeb, the core of the problem lies not only in the interest rates but in the way the consigned card is offered and operationalized.

-

50 viaducts, 4 tunnels, 28 bridges, and 40 kilometers of bike paths: BR-262 in Espírito Santo will receive 8.6 billion reais for the largest engineering project in the state’s history, inspired by the Immigrant Highway in São Paulo.

-

Brazil produces too much clean energy and doesn’t know what to do with it: over 20% of solar and wind capacity was wasted in 2025 while investors flee and 509 renewable generation projects were abandoned in the last year.

-

Piauí will produce a new fuel that replaces diesel without needing to change anything in the truck’s engine and reduces pollutant gas emissions by half: truck drivers from all over the Northeast are already celebrating the news that will arrive later this decade.

-

A new Brazilian shopping center worth R$ 400 million will be built in an area equivalent to more than 4 football fields, featuring 90 stores, 5 cinemas, a supermarket, a college, and parking for 1,700 cars, potentially generating 3,000 jobs.

The product is presented as an easy credit extension, with direct payroll deductions, which gives a sense of safety and control.

In practice, the action claims that the contractual structure induces retirees and pensioners into a situation where the approved limit far exceeds the available income. The entity asserts that:

the automatic deduction from benefits, limited to 5% of income for each consigned card, coexists with credit limits that reach 160% of the benefit amount

by simultaneously contracting RMC and RCC, the potential income commitment can reach up to 320%, a level that Abradeb classifies as “arithmetically unfeasible”

According to the petition, in this scenario, the minimum repayment deducted from payroll does not significantly reduce the outstanding balance, pushing retirees into over-indebtedness and extending the dependence on rotating credit indefinitely.

Consigned Card, RMC, and RCC: From the Promise of Ease to Over-Indebtedness

The action claims that the consigned card was incorporated into the market through regulatory frameworks without robust legislative debate, which would have allowed for the creation of a product with high risk for retirees.

Abradeb contends that, in the current design:

the consumer is led to believe they are contracting a conventional loan, but in reality, they enter a rotating credit modality attached to the consigned card

immediate withdrawals become the rule, not the exception, consuming much of the consigned margin

the bill is structured so that the minimum installment, deducted directly from the benefit, is not sufficient to amortize the principal, only to keep the contract active

Data cited by the entity, based on information from the National Consumer Secretariat, indicates that 97.4% of consigned card contracts involve immediate withdrawals and that, among users who use the product only for withdrawals, the total default rate on bills reaches 92.5%.

In the authors’ view, this dynamic reinforces the thesis that over-indebtedness is not an accident but part of the product’s logic, especially when directed at retirees and other hyper-vulnerable consumers.

Why Abradeb Talks About “Eternal Debt”

The central point of Abradeb’s critique is the absence of a clear horizon for settlement. The entity claims that the current model of credit consigned in the form of a consigned card:

does not foresee a certain and reasonable deadline for extinguishing the debt

allows the debt to extend for years, with successive renewals and recomposing the limit

turns payroll deductions into a permanent income capture mechanism for retirees, pensioners, and public servants

The petition asserts that when the limit of the consigned card is continuously reoccupied by new charges, fees, and interest, the consumer lives in a state of “eternal debt”, in which the minimum installment deducted guarantees the revenue flow for the 27 banks, but does not guarantee the holder any concrete perspective of recovering their own financial capacity.

For Abradeb, this scenario constitutes “expropriation of food income”, as pension income, which should ensure the minimum essential, becomes drained to sustain a credit operation structured around the over-indebtedness of retirees on a large scale.

What the Action Asks the Justice Against the 27 Banks

The civil class action does not limit itself to requesting one-time compensations. It seeks to structurally change the way credit via consigned card is offered and charged to consumers. Among the requests directed at the Judiciary, Abradeb seeks the recognition of:

the practice of irresponsible credit granting, inducing over-indebtedness of retirees and other vulnerable groups

the obligation that the bill for the consigned card be fully paid within the legal limits of the consigned margin, preventing the debt from being indefinitely pushed to the rotating credit

the prohibition of withdrawals exceeding the legally prescribed consigned margin

the automatic blocking of the card when the credit limit cannot be met within the legal margin, preventing the rotating balance from growing uncontrollably

In the indemnity field, Abradeb requests:

R$ 17,000 in individual moral damages for vulnerable consumers

R$ 20,000 in individual moral damages for hyper-vulnerable individuals, such as the elderly, illiterate, or persons with disabilities

collective moral damages calculated at R$ 218 per affected consumer

social damage equivalent to 10% of the interest revenue from the consigned card portfolio between 2015 and 2025

If accepted, these requests could generate a billion-dollar impact on the 27 banks defendants, in addition to redefining the conditions for offering credit consigned nationwide.

Social Impact in Mato Grosso and Beyond the State

Although the process is concentrated in the Specialized Court for Class Actions in Cuiabá, Abradeb argues that the contracting standard described is replicated in different regions of the country.

In Mato Grosso, the focus is on retirees and pensioners who had their income compromised at a percentage far exceeding the legal limit, often without a full understanding of the product’s risks.

The petition emphasizes that the combination of low income, advanced age, low level of education, and contractual complexity makes these consumers prime targets for aggressive offers of consigned card.

Instead of a tool for financial inclusion, credit consigned becomes, according to the action, a vector of structured over-indebtedness.

By legally questioning the conduct of the 27 banks, Abradeb seeks to pave the way for a broader review of the protection rules for retirees and other people who depend on pension income to survive.

The outcome of the case could serve as a parameter for future class actions in other states.

For you, retirees who fall into debt that never ends because of consigned card and poorly explained credit are primarily the fault of those who sell the product or those who sign without understanding the entire contract?

Seja o primeiro a reagir!