Portuguese

Portuguese  English

English  Spanish

Spanish

Central Bank Complaint List Exposes Worst Banks in Brazil, Highlights Fragility of Credit Guarantee Fund and Shows How Direct Treasury Works as a Safe Vault, While Investors Review Liquidity Risks, Trust Less in the Private System and Reinforce the Search for Simple Protection Throughout Brazil Today

In the most recent survey, the Central Bank made public the list of the worst banks in Brazil for customer service and problem resolution, based on complaints made directly to the agency and cases where the monetary authority concluded that the customer was right. Meanwhile, a troubling alert surfaced: the FGC has only 2.3% of the total it claims to guarantee, which means that the failure of a large bank or two small ones simultaneously would already be enough to put the protection system in jeopardy.

In a recent class, a specialist showed that, while individual investors delude themselves with the “automatic protection” of R$ 250 thousand per CPF, the Credit Guarantee Fund is not state-owned, is not obligated to cover everything it promises, and only pays if it has resources, contrary to popular belief. Given this scenario, the analysis converges to the same conclusion: The Direct Treasury today functions as the true safe vault of the Brazilian investor, by concentrating the risk on the sovereign issuer and not on individual banks.

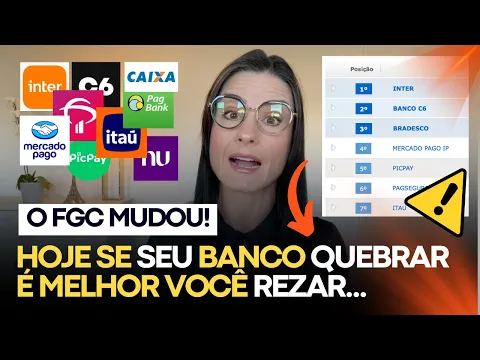

How the Central Bank Measures the Worst Banks in Brazil

The ranking released by the Central Bank does not address the financial health of the institutions, but rather their reputation in customer relations.

-

Brazilian city gains industrial hub for 85 companies that is equivalent to 55 football fields.

-

Peugeot and Citroën factory in Argentina cuts production by half and opens a layoff program for more than 2,000 employees after Brazil drastically reduced purchases of Argentine vehicles.

-

A Brazilian city gains a factory worth R$ 300 million with the capacity to process 200 thousand tons of wheat per year, a mill of 660 tons/day, silos for 42 thousand tons, and an industrial area of 276 thousand m².

-

Havan will leave the shopping mall in Blumenau to inaugurate something that the chain has never done before: a megastore in half-timbered style in the Historic Center of the city, which is expected to be completed in May and change the landscape of local retail.

The list considers formal complaints received by the BC and an index that weighs the number of complaints against the size of the customer base, to avoid the distortion of larger banks always appearing as worse just due to absolute volume.

In this context, the higher the index, the worse the bank appears.

Among the large banks, Nubank ranks at the bottom of the list, with an index of 12.67 and only 13 complaints for nearly 110 thousand customers, according to the cited class.

On the negative top are Bradesco, Banco C6, and Banco Inter, the latter with an index of 96.37 and a history of complaints such as undue charges on cards, duplicate transactions, non-recognition of invoice payments, and discrepancies between total expenses and total charged.

The specialist even reports personal access issues with the account, even with available balance, illustrating how operational failures can drag on for months.

The critical point is that, if a bank with a very bad reputation causes a run on withdrawals, the institution has no way to immediately return all the money, because it has loaned those resources to companies and individuals.

Bad reputation, therefore, can trigger liquidity risk, even if capital indicators are up to date.

Basel and Immobilization: The Numbers That Reveal the Bank’s Health

Before only looking at the rate of a CDB, the specialist recommends that the investor check two basic regulatory indicators: the Basel index and the immobilization index.

The Basel index measures the relationship between the bank’s capital and the volume of credit granted, serving as a cushion against mass defaults.

According to Central Bank regulations, the indicator must be above 11% for the institution to be considered safe.

In the example presented, Nubank has a Basel ratio of 15.8%, which means that for every R$ 100 lent, it has R$ 15.80 of its own capital.

The immobilization index shows how much of this capital is tied up in low liquidity assets, such as real estate and vehicles.

There, the number is 2.6%, and in this case, the lower the better, because it indicates that almost all capital is in assets that can be quickly converted into cash to pay customers.

The Central Bank considers it safe to keep this indicator below 50%.

An additional warning is that the issuing bank of your investment is not always the same bank of the application you use.

When buying a CDB through a platform like Nubank, for example, the money may be lent to Paraná Banco, PagBank, or another issuer.

It is this issuer that must have its Basel and immobilization evaluated, and not just the bank through which you accessed the product.

Why the FGC Has Only 2.3% of What It Promises to Guarantee

The class debunks another common belief in financial retail: that the Credit Guarantee Fund is an absolute shield for any banking application up to R$ 250 thousand.

In practice, the FGC is a private entity maintained by the banks themselves and, according to the data presented, has only 2.3% of the total time deposits it claims to guarantee.

This means that, if a single large bank fails or two small banks fail together, there is not enough money to reimburse all customers within the theoretically promised limit.

The fund’s own statute makes it clear that it only covers if there are available resources, with no legal obligation to fully honor all losses.

With the change in coverage limit from R$ 70 thousand to R$ 250 thousand and the explosion of fintechs, the number of institutions has increased, as has the chance of isolated problems.

Another point that often goes unnoticed is that, unlike deposit insurance in the United States, the FGC is not an arm of the Brazilian federal government.

If the fund runs out of resources, there is no automatic commitment from the National Treasury to recapitalize it just to protect retail investors who sought higher rates in fragile banks.

Therefore, the specialist emphasizes: do not use the FGC as a crutch to go hunting for interest rates at any bank.

Direct Treasury as the True Safe Vault for the Brazilian Investor

After highlighting the weaknesses of private protection, the specialist points to the Direct Treasury as the safest place for long-term money.

When buying Selic Treasury, IPCA Treasury, fixed-rate or Renda Mais, the investor is lending directly to the federal government, not to a specific bank.

The logic of safety here is different.

If the government does not have the cash to pay the bonds, it still has tools that a bank will never have: it can issue currency, seek loans from international organizations, roll over debts, or raise taxes to restore the payment flow.

Regardless of who is in power, the sovereign issuer concentrates instruments to honor commitments that no private institution can match.

That is why, in direct comparison, Direct Treasury is much closer to a public safe than any investment supported by the FGC.

How to Adjust the Strategy of Those Investing in Banks Today

The combination of the Central Bank list, the real limits of the FGC, and the robustness of the Direct Treasury suggests a shift in posture for individual investors.

Instead of blindly trusting private guarantees, the path is to diversify issuers, favor banks with good Basel ratios, low immobilization, and reasonable reputation, and reserve the most important part of the safety reserve for public bonds.

This does not mean completely abandoning CDBs, LCIs, and LCAs, but treating them as complements to seek extra returns, and not as the core of wealth protection.

The part you cannot afford to lose should preferably be in Treasury securities.

In times of banking noise and undercapitalized FGC, the Brazilian investor gains more by being a partner of the state through Direct Treasury than betting that all banks and all private guarantees will work at the same time.

Given this data on the worst banks, the real limit of the FGC, and the relative strength of the Direct Treasury, do you still feel comfortable keeping most of your reserve in medium banks and fintechs, or do you consider it more prudent to shift the “main vault” of your money to federal public securities?

-

-

-

3 pessoas reagiram a isso.