Portuguese

Portuguese  English

English  Spanish

Spanish

The State Redefined The Housing Game By Transforming Housing Credit Into Financial Product (SFI + Securitization Purchased With FGTS), Creating A Cycle That Pushes Prices Up While Lengthening Terms (Up To 420 Months) And Elevating The Final Cost For The Generation That Wants It Most But Can Least Buy.

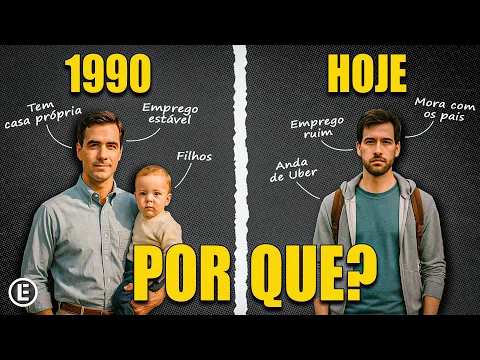

The narrative that young Brazilians “prefer to rent” does not hold up against the data. According to a survey cited by Canal Elementar, 93% of Generation Z still dream of owning their own home, and 68% of people between 21 and 34 years old declare that they prefer to buy rather than live in rental properties. The problem is not desire, but feasibility: the math simply does not add up for those entering the market in 2025.

The historical milestone of this process is 1997, when the Real Estate Financing System (SFI) was created.

What was once the State as a direct provider of housing became a financial cog: mortgages were transformed into securities, bought even with FGTS funds, feeding a cycle that artificially elevated real estate prices.

-

Brazilian city gains industrial hub for 85 companies that is equivalent to 55 football fields.

-

Peugeot and Citroën factory in Argentina cuts production by half and opens a layoff program for more than 2,000 employees after Brazil drastically harmed purchases of Argentine vehicles.

-

A Brazilian city gains a factory worth R$ 300 million with the capacity to process 200 thousand tons of wheat per year, a mill of 660 tons per day, silos for 42 thousand tons, and an industrial area of 276 thousand m².

-

Havan will leave the shopping mall in Blumenau to inaugurate something the chain has never done before: a megastore in half-timbered style in the Historic Center of the city, which is expected to be ready in May and change the landscape of local retail.

The practical result is a generation that desires to buy more, but ends up being pushed into renting.

How The Rent Generation Was Born

The SFI and securitization allowed banks to transform credit portfolios into securities sold to investors.

Between 2011 and 2016, Caixa Econômica Federal issued R$ 18.9 billion in securities, and a significant part was purchased by FGTS, a fund made up of workers’ money.

This operation freed up resources for new financing, but at the same time, stimulated increasingly higher prices, as the available credit grew along with property values.

In practice, young Brazilians began facing more expensive properties, extended terms for up to 420 months, and interest rates that average around 10% per year.

This means that the final cost of a property can double in three decades.

The financing model became a barrier to entry, making home buying unfeasible for a large part of the active population.

The Impact of The Pandemic and The Price Surge

The health crisis of 2020 worsened the problem. The cost of construction materials skyrocketed over 50% in two years, with spikes of nearly 90% in steel and 88% in PVC.

Meanwhile, remote work increased the demand for larger homes and shifted demand towards the countryside, leading to further price increases.

An example cited in the study: São José do Rio Preto recorded a 136% increase in sales and 255% in launches in 2024.

Brazilian real estate inflation continued to rise above the global average.

In 2024, property values increased by 7.7%, nearly triple the global average (2.6%) and at the fastest rate since 2013.

This appreciation, combined with expensive credit, widened the gap between the dream and reality for the rental generation.

Young People With No Escape: Homeownership Distant, Renting As The Norm

The statistics show the dilemma: 31% of Generation Z still live with their parents because they cannot afford rent or to buy.

Only 45% of young people between 18 and 34 years old say they are fully financially independent.

Meanwhile, those who rent see their income dwindle: paying R$ 2,500 monthly for 30 years equals R$ 900,000—almost two apartments, but with no assets at the end.

Research reinforces this picture: 62% of young people believe it is harder to buy a property today than for previous generations.

Still, 73% still dream of owning their own home. What changes is the way they seek to get there: alternatives like remote work for foreign companies and generating income in strong currencies (dollar/euro) emerge as strategies to overcome the limitations of local income and form a down payment.

Speculation and Vacant Properties

Another factor exacerbating the rental generation crisis is the retention of inventories. In São Paulo alone, there are nearly 600,000 closed properties awaiting appreciation, according to the survey.

Meanwhile, those who need housing are pushed towards increasingly distant outskirts, where transportation and public services do not keep up with population growth.

This phenomenon reveals how housing has ceased to be merely an essential good and has come to be treated as a financial asset.

The result is an artificial scarcity of affordable properties and the perpetuation of an inflated market.

In almost three decades, the Brazilian State has stopped being a builder of homes to become the organizer of a market that favors banks, funds, and investors, while pushing millions of young people into the rental generation.

Still, the majority still dream of buying their own home, even if they need to seek strategies outside the traditional framework.

And you, do you believe Brazil should reconsider the use of FGTS and change the way it finances the housing sector, or is the current model the only possible way to sustain the market?

Leave your opinion in the comments—we want to hear from those who experience this firsthand.

Então, de 1997 pra cá só tivemos 4 anos de governo da direita, o restante foi da esquerda dita socialista e defensora das classes menos favorecidas. Analisem, de forma isenta sem fanatismo e ideologias, de quem é a responsabilidade.

Simples; Construir casa pro “pobre” não dá voto…