Portuguese

Portuguese  English

English  Spanish

Spanish

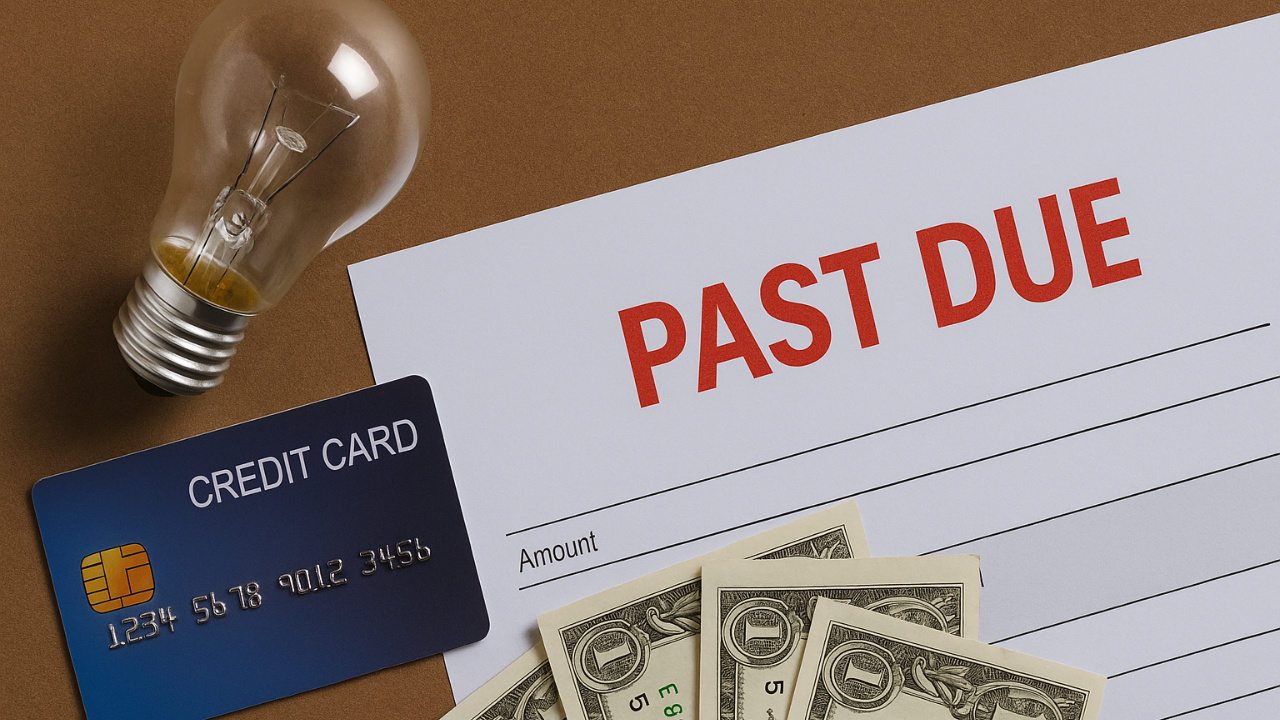

Household Debt Rises, Credit Card Becomes Income, and High Interest Rates Increase Default in Brazil.

The numbers tell one story while families feel another in Brazil.

While recently released indicators suggest a slight economic improvement, those dealing with accumulated bills report that the pressure remains.

According to experts, household debt remains high, driven by the increasing use of the credit card as a source of income, persistent default, and high interest rates, forcing millions of Brazilians to renegotiate debts as the only alternative.

-

A Brazilian city gains a factory worth R$ 300 million with the capacity to process 200 thousand tons of wheat per year, a mill of 660 tons per day, silos for 42 thousand tons, and an industrial area of 276 thousand m².

-

Havan will leave the shopping mall in Blumenau to inaugurate something the chain has never done before: a megastore in half-timbered style in the Historic Center of the city, which is expected to be ready in May and change the landscape of local retail.

-

Unemployment rises again to 5.8% at the beginning of 2026, raising alarms about the end of temporary positions and its impact on the Brazilian job market.

-

Document organization can cut invisible costs in small businesses, a simple step that prevents waste, rework, and losses in daily operations.

This phenomenon occurs across the country, affects all age groups, and gains momentum precisely now when inflation slows down and the first signs of statistical relief appear.

Debt Grows Even With Improvement in Indicators

According to Serasa, 80.4 million Brazilians are in debt, accumulating 321 million debts totaling R$ 509 billion.

The average debt per person exceeds R$ 6.3 thousand, while each individual debt is around R$ 1,584.96.

Despite a slight decrease in the aggregate index to 79.2% in November — the first drop in nine months — the gap between statistics and reality remains wide.

The CNC emphasizes that the situation is more severe among low-income families. Among those earning up to three minimum wages, 82.5% are in debt.

In the range of three to five minimum wages, the rate reaches 81.1%. Small financial imbalances are enough to compromise the entire budget.

Credit Card Becomes Income and Pushes Families into Default

In the daily lives of millions of Brazilians, the credit card has ceased to be just a means of payment and has become an immediate source of income.

When the salary doesn’t cover the bills, it is the one that sustains the pantry.

“The credit card has become a snowball. […] Nowadays, it’s used to buy food daily, because the money at the end of the month doesn’t cover all the bills,” reported freelancer Luiz Fernando Mamede, 23 years old.

The Selic rate at 15% per year and the accumulated inflation of 4.4% make credit expensive, especially for those needing to split basic expenses.

Even essential items have risen above average, reducing repayment capacity.

As a consequence, the share of income devoted to debt has reached 28.8%, the highest level in history, according to the Central Bank.

Interest alone consumes 10.23% of this income.

High Interest Rates Pressure Entrepreneurs and Increase Debt Renegotiation

The squeeze also affects small businesses. Micro-entrepreneur Vanda Cristina Pereira, mother of six, sums up the challenge:

“Sometimes taxes are so high, bills are so high, and difficulties are so great that in the end, I receive much less than my own employee.”

As a reflection, renegotiating has become routine. The credit limit, she says, serves as a “lifeline,” preventing the situation from escalating into default.

Debt Renegotiation Eases But Does Not Solve the Structural Problem

According to researcher Flávio Ataliba from FGV Ibre, the main driver of household debt is precisely the credit card.

“Almost over 90% of debts occur with credit cards,” he claims.

He warns that when the card starts to function as “continuous income,” the snowball effect is inevitable. By failing to pay the full bill, the consumer falls into revolving credit — a type with interest rates exceeding 400% per year — and the amount owed multiplies rapidly.

Even renegotiation initiatives, such as the Desenrola program, have limited reach. “The program was a temporary relief […] The structural trend remains,” Ataliba emphasizes.

The chief economist of CNC, Fabio Bentes, agrees. Debt renegotiation programs reduce immediate impact but do not solve the core issue: expensive credit and insufficient income.

Credit Insurance Emerges as a Little-Explored Buffer

When there is no financial margin, any unforeseen event pushes families into debt. In this scenario, credit insurance appears as a still underutilized alternative.

The president of Fenaprevi’s Risk Commission, Ana Flávia Ribeiro, highlights the potential of the sector:

“Today, in Brazil, around 6% of GDP corresponds to insurance operations […] the market has a lot of room to grow.”

The credit insurance can fully pay off or amortize debts in case of unemployment, illness, or death, acting as a “financial airbag.” The product already accounts for 49% of the sector’s premiums and 53% of indemnities.

Between Statistics and Real Life: The Brazil of Data and the Brazil of the Wallet

So, despite the signs of improvement, the routine of Luiz Fernando, Vanda, and millions of families shows that the struggle persists.

Experts point out that lower interest rates for an extended period, consistent income growth, and financial education are essential to reversing the scenario.

In the meantime, the credit card continues to be both an entry point for consumption and the main vector of household debt, default, and the growing dependence on debt renegotiation.

-

-

2 pessoas reagiram a isso.