Portuguese

Portuguese  English

English  Spanish

Spanish

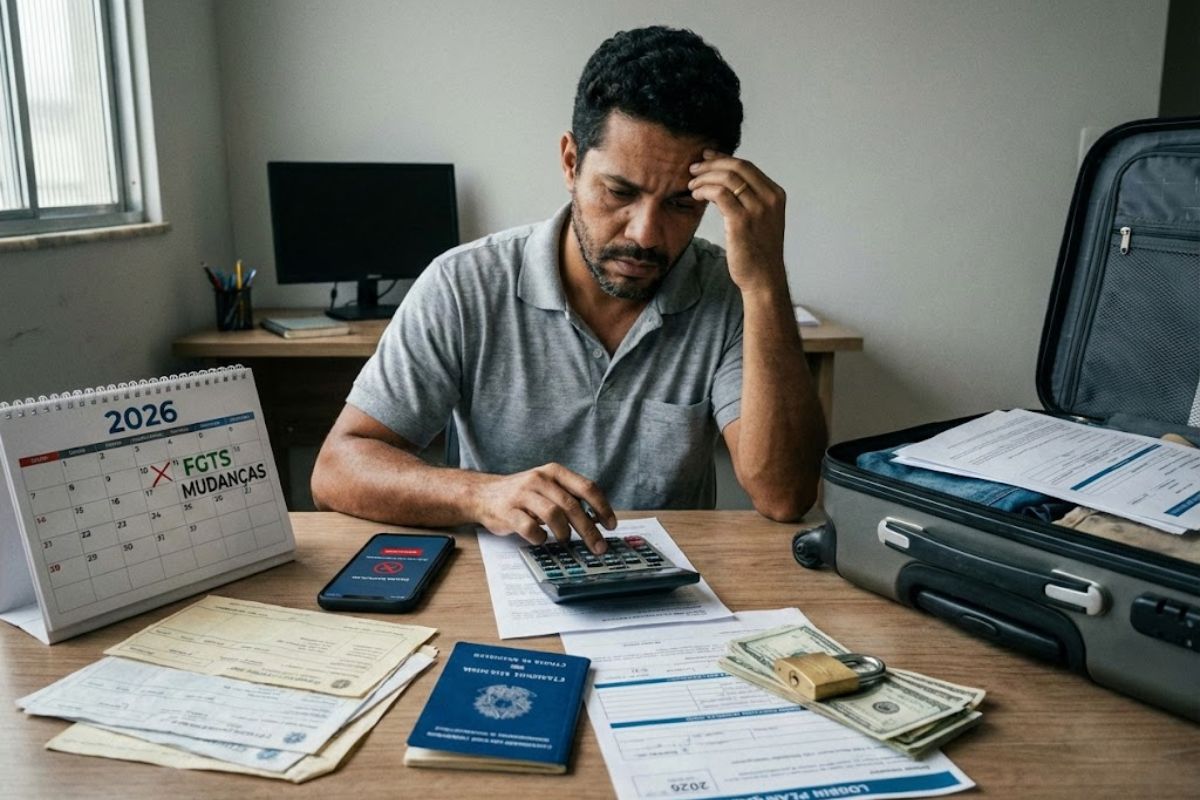

Starting in 2026, the FGTS will have new restrictions: the end of the block for dismissed workers, a limit of three installments of 500 reais in the anniversary withdrawal, a 90-day grace period, and only one loan per year, forcing workers to rethink their use of the fund and reduce the risk of over-indebtedness from anticipations.

In March 2025, Provisional Measure 1,290/2025 corrected a historical distortion of the FGTS, releasing the withdrawal of retained balances for about 12.2 million dismissed workers who were in the Anniversary Withdrawal modality, entitled to full withdrawal in case of dismissal without just cause. The measure ended the block that kept money idle precisely at the time of greatest financial vulnerability.

With this step completed, the government began to target 2026 as the year of stricter credit rules linked to the FGTS, especially regarding the anticipations from the Anniversary Withdrawal. Starting in November 2026, the system will limit the volume of installments that can be used as collateral, the amount per installment, and the number of operations per year, curbing the “easy credit spree based on the fund.”

How MP 1,290/2025 Unlocked Trapped Balances in the FGTS

The first structural change in the FGTS came with MP 1,290/2025, which addressed the retained balances of those who had chosen the Anniversary Withdrawal and were dismissed.

-

A new Brazilian shopping center worth R$ 400 million will be built in an area equivalent to more than 4 football fields, featuring 90 stores, 5 cinemas, a supermarket, a college, and parking for 1,700 cars, potentially generating 3,000 jobs.

-

Larger than entire cities in Brazil: BYD is building a 4.6 km² complex in Bahia with a capacity for 600,000 vehicles per year, but the discovery of 163 workers in conditions analogous to slavery has shaken the entire project.

-

With an investment of R$ 612 million, a capacity to process 1.2 million liters of milk per day, Piracanjuba inaugurates a mega cheese factory that increases national production, reduces dependence on imports, and repositions Brazil on the global dairy map.

-

Brazilian city gains industrial hub for 85 companies that is equivalent to 55 football fields.

Before the change, these workers could not withdraw the remaining balance in case of dismissal without just cause, being denied access to a significant portion of their own reserve in a critical scenario.

With the new rule, payments began in March 2025, allowing 12.2 million people to recover the money that remained blocked.

The MP consolidated the understanding that, in cases of dismissal without just cause, workers regain the right to the full withdrawal of the FGTS, regardless of previous options for the Anniversary Withdrawal.

At the same time, the two-year grace period that restricted withdrawal after dismissal was abolished, reinforcing the protective function of the fund in situations of job loss.

Limit of Three Installments of 500 Reais in the Anniversary Withdrawal

Having resolved the issue of trapped balances, the regulation for 2026 shifts attention to the use of FGTS as fuel for successive loans.

Starting in November 2026, financial institutions will only be able to anticipate three annual installments from the Anniversary Withdrawal, radically reducing the possibility of compromising several years of future receipts all at once.

In addition to the quantity limit, each anticipated installment will have a cap of R$ 500.00, which reduces the available credit volume and forces the worker to recalculate whether it is worth turning periodic withdrawals into debt.

In practice, those who planned to “zero out” the FGTS balance with successive anticipations to settle other bills will find a much more restricted scenario with less room to compromise the fund for long periods.

Who Can Still Withdraw FGTS After the Changes

Even with the new restrictions, the FGTS maintains priority groups with guaranteed access to the balance in specific situations.

In the case of workers dismissed without just cause, the 2025 MP confirmed the right to withdraw the remaining balance, even for those who opted for the Anniversary Withdrawal.

The system emphasizes the protective function in times of income loss.

The adherence to the Anniversary Withdrawal remains allowed for those wishing to receive an annual installment in their birthday month, but now under stricter credit rules.

As for retirement and serious illnesses, the conditions for full withdrawal remain unchanged, preserving the logic of addressing higher vulnerability situations.

In all cases, the worker must monitor the FGTS statement and the current rules to avoid confusing the right to withdraw with the credit limit.

90-Day Grace Period and Only One Credit Operation Per Year

Starting in 2026, the FGTS will incorporate a “cooling” mechanism for indebtedness decisions.

Those who choose the Anniversary Withdrawal will have to wait for a 90-day grace period before contracting any credit operation linked to the fund, preventing the option for the modality from being immediately followed by impulse loans.

Furthermore, the worker will be limited to only one credit operation per year, ending the practice of taking multiple small loans from different banks using the FGTS as collateral.

By centralizing the debt into a single annual operation, the new rule facilitates financial control and reduces the fragmentation of commitments that, in practice, raised the risk of silent over-indebtedness.

Safety Mechanisms Against Easy Credit and Over-Indebtedness

With this set of changes, the design of the FGTS in 2026 aims to balance access to the resource and the protection of assets.

By limiting installments, values, frequency of operations, and imposing grace periods, the regulator seeks to curb the use of the fund as a permanent extension of the credit card limit or overdraft, rather than as a reserve for emergencies and protection in case of termination.

In practice, over-indebted workers will be forced to reassess their plans before withdrawing the entire fund.

Instead of anticipating several years of the Anniversary Withdrawal at once, they will have to decide if a credit limited to three installments of R$ 500, with a grace period and only one annual operation, is sufficient to solve the problem or if it is necessary to seek other negotiation methods.

The Role of Digital Payroll Loans with FGTS as Collateral

Given the restrictions on the Anniversary Withdrawal, the government bets on Digital Payroll Credit via FGTS Digital as an alternative financing option.

In this modality, the FGTS serves as collateral for loans with payroll deductions, without the need to anticipate the annual withdrawal.

The idea is to offer credit with lower interest rates than those in the traditional market.

As the risk of default is covered by a guarantee fund linked to the system, the rates tend to be more competitive, while preserving the structure of the FGTS.

For the worker, the practical difference is that the money remains in the fund, while the bank has security to lend at a lower cost, provided the value and operation limits are respected.

What Changes for Workers’ Planning in 2026

With the new package of rules, the FGTS ceases to be an almost unrestricted source of credit and returns to its original function as a compulsory savings for critical moments.

In 2026, the combination of the limit of three installments of R$ 500, the 90-day grace period, and only one loan per year forces workers to plan each operation more carefully, instead of using the fund as an automatic cash source whenever the budget tightens.

For those already in debt, the scenario demands careful calculation: assessing whether the amount available under the new conditions truly resolves the issue, comparing it with other credit alternatives, and considering the impact of partially depleting a reserve that can be crucial in case of termination.

The use of the FGTS as collateral or as a withdrawal source becomes a matter of financial planning, not just an immediate escape valve.

In light of these changes, do you intend to continue using the FGTS as a source of credit or will you treat the fund primarily as an emergency reserve for dismissal and really extreme situations?

-

2 pessoas reagiram a isso.