Portuguese

Portuguese  English

English  Spanish

Spanish

With the reopening of the oil market in Brazil in 1997, it was expected that new private investments would be made in the sector. New investments were anticipated in the refining park, and competition was hoped to bring gains in quality and prices. To allow Petrobras and private companies (Manguinhos and Ipiranga) to adapt to the free market, Law 9.478/97, known as the “Oil Law,” guaranteed market reserve for several years (Law 9.478/97, in its Articles 69 to 74, allowed for subsidies to private refineries and price and import controls by the Regulatory Agency for up to 5 years). This would, in a way, allow companies to transition to a competitive regime.

Indeed, shortly after, some market movements occurred that reinforced the initially imagined expectations. The Repsol YPF group, for example, acquired part of the control of the Manguinhos refinery. Later, it also acquired 30% of one of Petrobras’ refineries in Rio Grande do Sul. Furthermore, the Manguinhos and Ipiranga refineries submitted expansion plans for their units to the ANP. Two new private refineries emerged, Univen and Dax Oil. The restructuring of the sector and free competition seemed to be having the intended effect with the end of the monopoly. However, the following years showed that the difficulties for private refineries were immense. A brief analysis of each of them over the past decade demonstrates the scale of the challenge.

-

Crewless and capable of spending 16 whole weeks without surfacing, the German drone submarine Greyshark uses hydrogen, carries 17 sensors, and creates underwater maps with a resolution of less than 2 centimeters per pixel, while just six units controlled by a single person can scan the entire Strait of Hormuz in 24 hours.

-

A building that looks like an inverted ship draws attention in São Paulo: the Hotel Unique, with 84 meters, round windows, exposed concrete, and a red pool on top.

-

A building that looks like an inverted ship draws attention in São Paulo: the Hotel Unique, with 84 meters, round windows, exposed concrete, and a red pool on top.

-

New wave energy machine is placed in the sea in Spain and promises to convert wave motion into electricity during offshore tests

Manguinhos Refinery

Inaugurated in 1954, in the state of Rio de Janeiro (RJ), the Manguinhos Refinery was prevented from expanding its activities due to the state monopoly arising from the creation of Petrobras in 1953. As a result, its refining plant remained of low complexity and small size compared to other refining plants in Brazil. Thus, it always required light crude oils for proper processing in its factory. Until 1963, the refinery itself acquired imported light oil to meet its needs. From that year onwards, Petrobras also began to exercise a monopoly on the importation of oil and derivatives, even meeting the needs of the private refinery, a situation that persisted until the early 2000s. Considering that the refinery survived the monopoly period, it can be assumed that, throughout this time, it had some market reserve allowed by successive Governments, because, otherwise, it would have been acquired by Petrobras, as occurred with the refineries in Manaus (REMAN) and Capuava (RECAP), or it would have gone bankrupt at the time due to oil shocks and controlled prices in Brazil.

After 44 years of operation, a year after the end of the monopoly on refining activities in the country, in 1998, the Spanish group Repsol YPF acquired part of the shares of the Manguinhos Refinery, beginning to share control of the unit with the then-owner, Grupo Peixoto de Castro. With promises of new investments, the partnership presented itself as an opportunity to boost business at the refinery, although this did not actually happen in the following years.

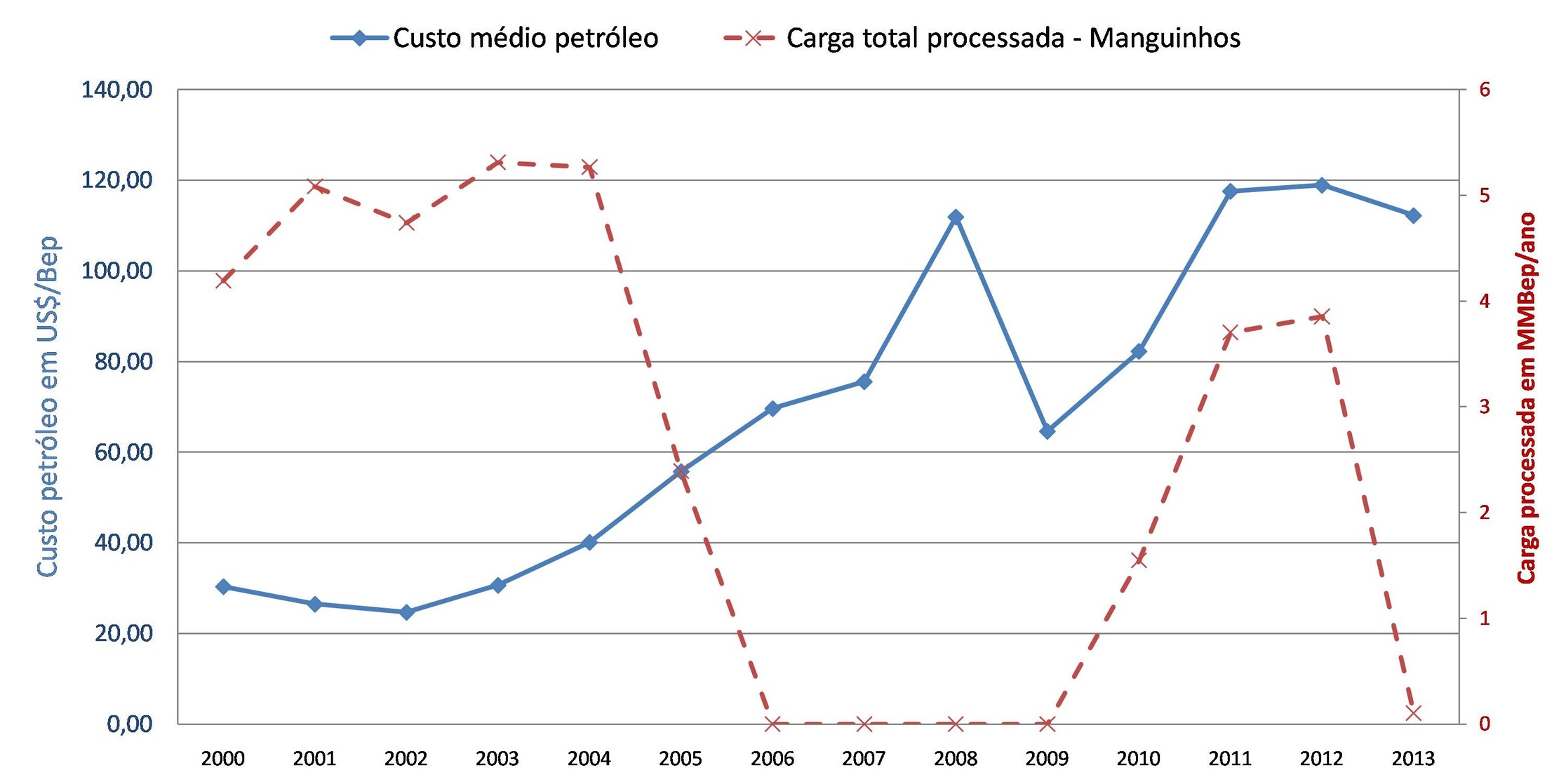

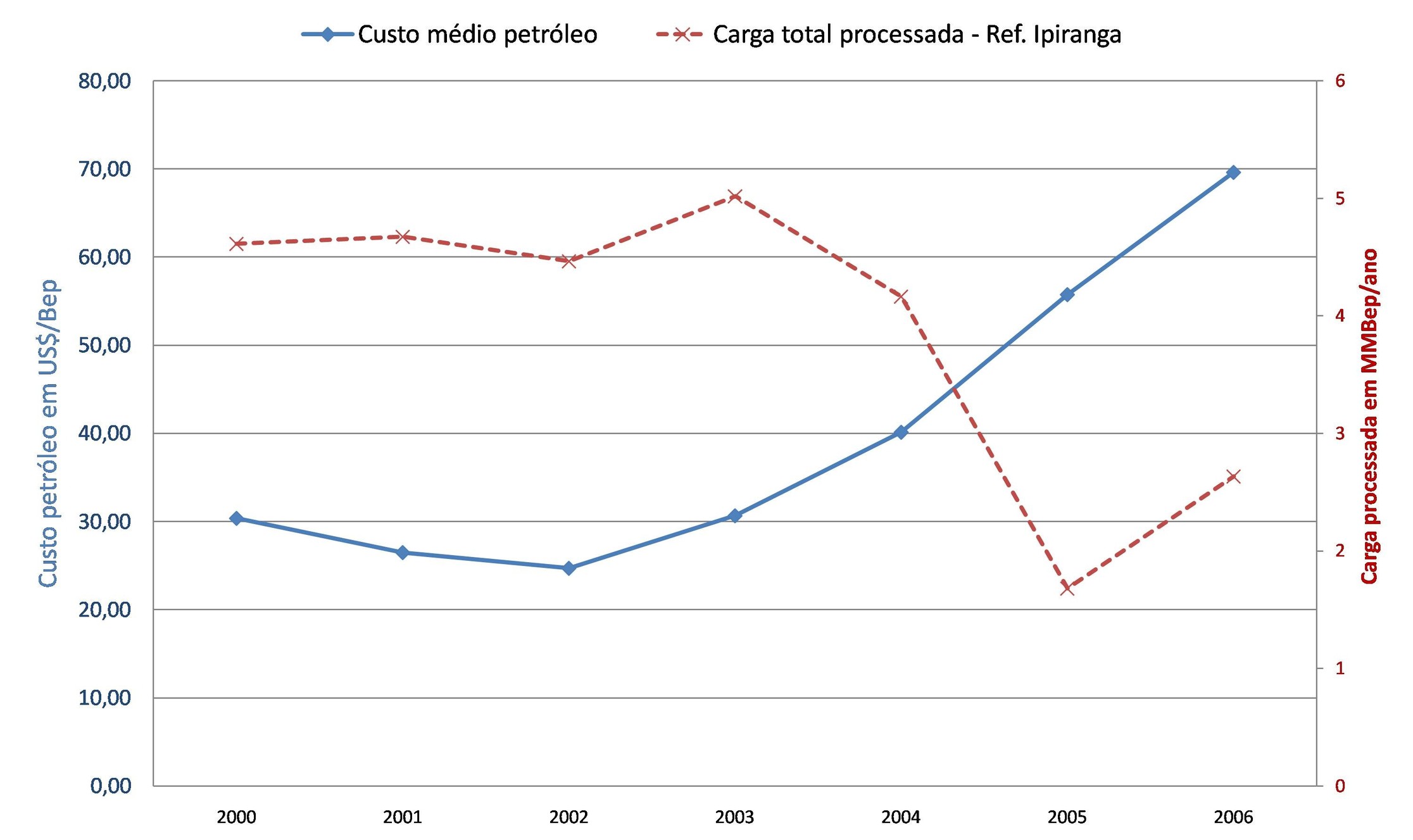

The investments, initially estimated by the new consortium, were reduced. There were several reasons for this. Repsol YPF began to face difficulties in Argentina, which had already been in crisis for almost a decade, and the operational results of the refinery were never encouraging. The price of oil in the international market skyrocketed, making Manguinhos’ refining margin negative, as the prices of fuels in the Brazilian domestic market were still defined by Petrobras, under indirect control of the Federal Government, which kept prices for long periods, not passing them on fully to the final consumer. From 2004 onward, the average price of oil in the external market began to rise in a constant upward trend, leading to a complete halt in the refinery’s production from 2006 to 2009, as observed in Figure 1.

Figure 1 – Average load processed in Manguinhos, in MMBep (millions of barrels equivalent of oil), and its relation to the price of crude oil (Source: own elaboration based on ANP, 2017)

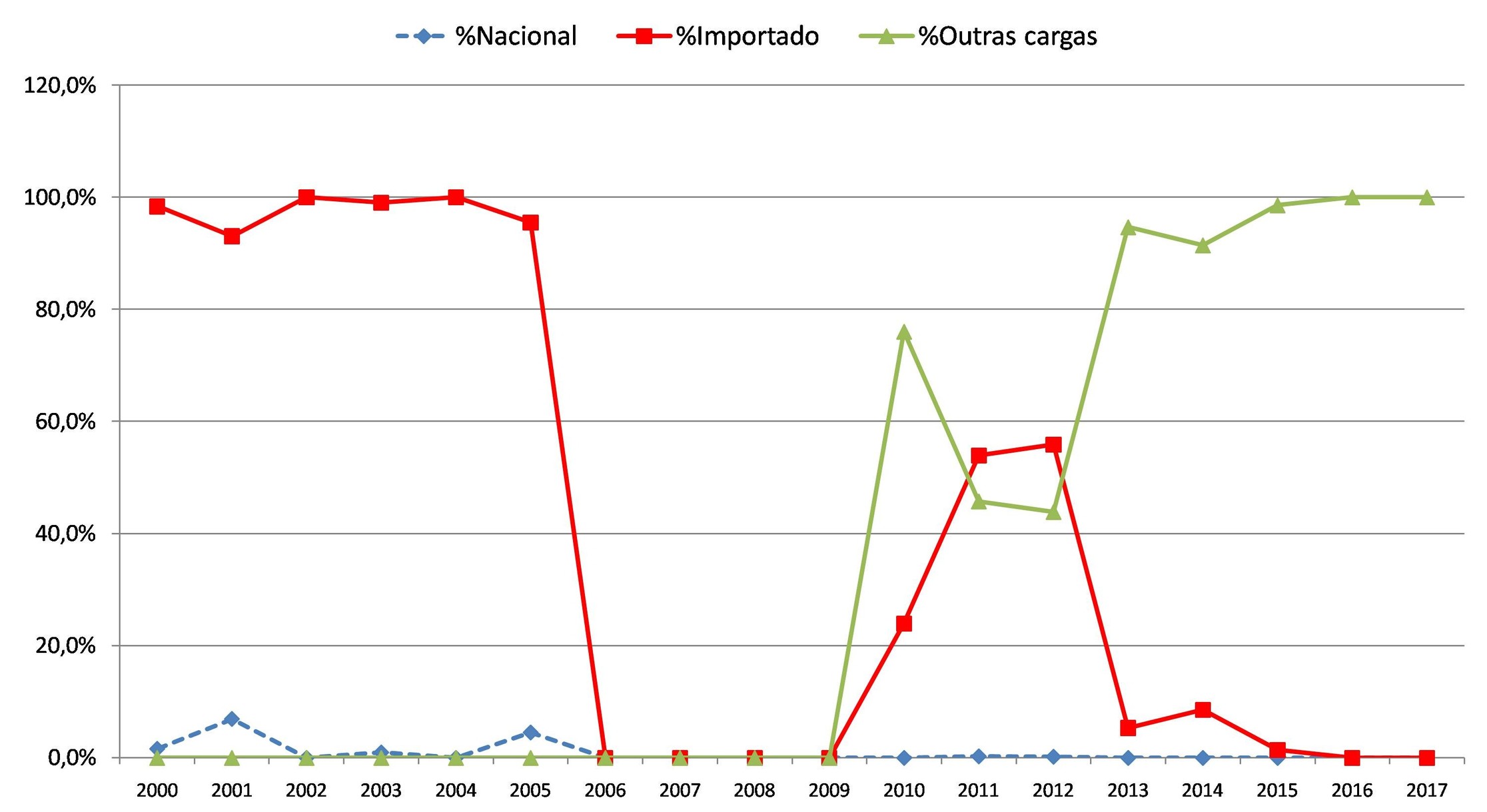

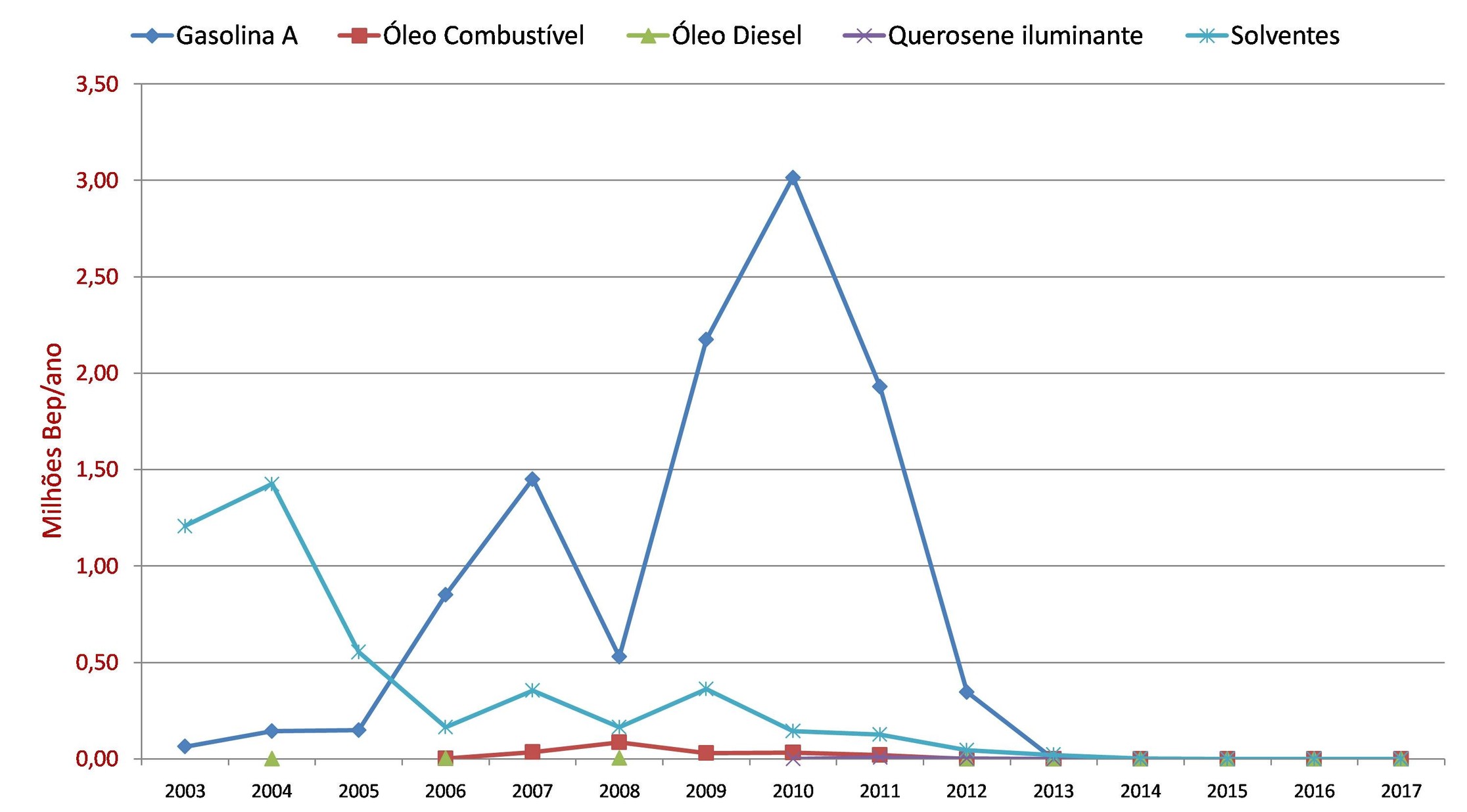

Unable to withstand a severe financial crisis, the refinery entered judicial recovery in 2008, when it was acquired by Grupo Andrade Magro, which was already active in the distribution of chemical products and fuels. When it resumed operations in 2010, a trend of reduced oil usage was observed in the following years (Figure 2), until, from 2013 onward, Manguinhos started processing other loads (such as naphtha and condensates) as a way to remain operational. Operational and financial results continued to be quite poor, and the refinery remained on the brink of bankruptcy. At the end of 2017, the refinery’s controller announced a name change for the unit, which became known as REFIT. Despite the name change, the challenges to resume oil refining were immense due to the age, size, and technology present at the refinery. Possibly, the refinery is now a more valuable asset as a fuel storage terminal than as a crude oil refining unit itself.

Figure 2 – Loads used in Manguinhos, in MMBep, from 2000 to 2016 (Source: own elaboration based on ANP, 2017)

Ipiranga Refinery

The Ipiranga Refinery began its operations in 1937, having adjusted its shareholding control the following year due to resolutions from the CNP, which stipulated that only natural-born Brazilians could be shareholders of refineries in Brazil. Similar to what happened with the Manguinhos Refinery, after the establishment of Petrobras’ monopoly, the private concession of Ipiranga was maintained, but it was also prevented from increasing its refining capacity throughout the entire period, being maintained through its market reserve over time.

The breaking of the monopoly in 1997, through Law 9.478, also guaranteed Ipiranga market reserve for five years so it could prepare for free competition. In 1998, the ANP ratified the ownership and rights related to the refining facilities of Ipiranga existing at that time, granting the refinery a refining capacity of 12,500 barrels/day based on the existing operational capacity. Although it was barred from expanding its activities during the monopoly, a significant improvement was implemented at Ipiranga Refinery in the 1970s, which was the installation of a Vacuum Distillation Unit. This gave Ipiranga a slightly greater flexibility than the Manguinhos refinery (which only had atmospheric distillation), allowing it to process somewhat heavier (and cheaper) oils.

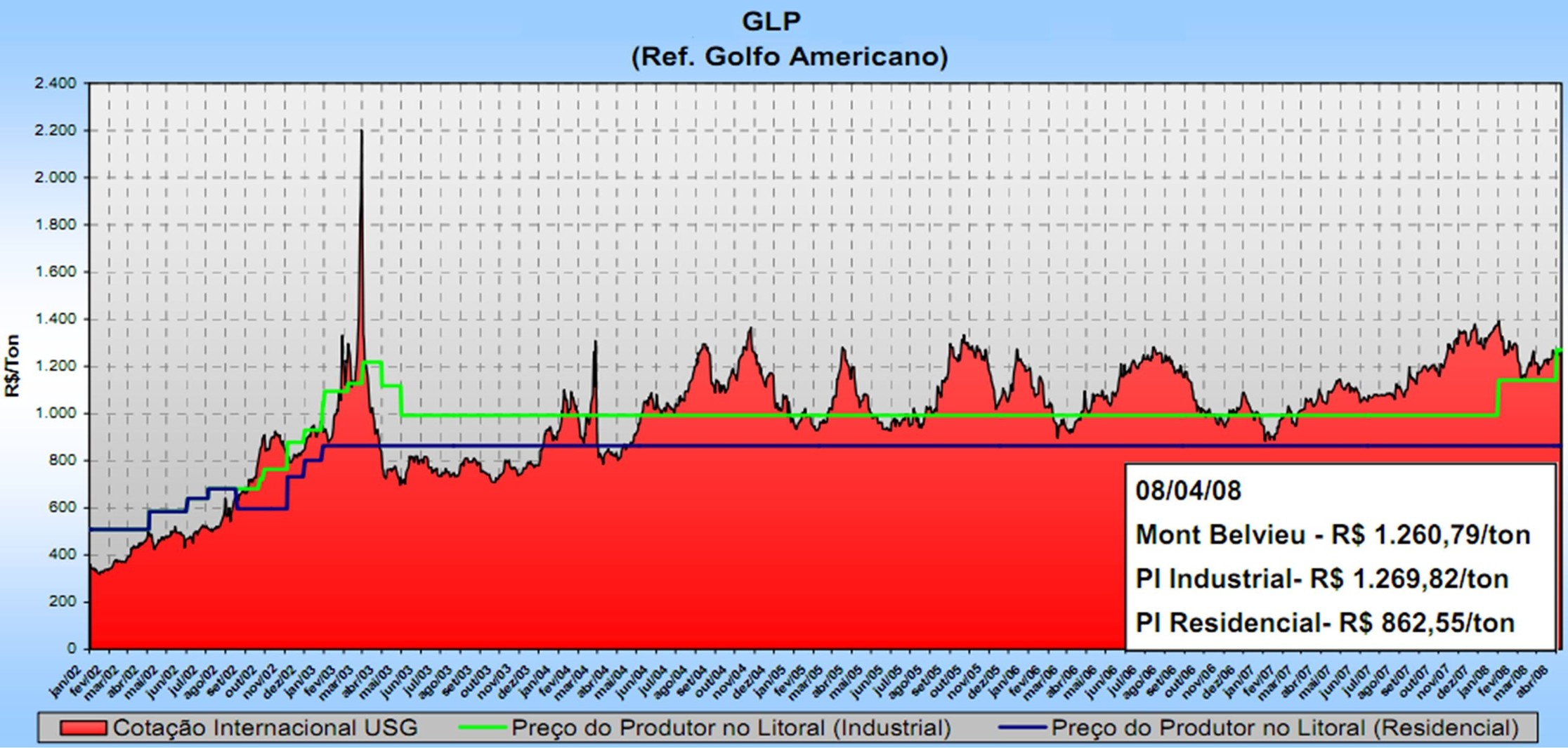

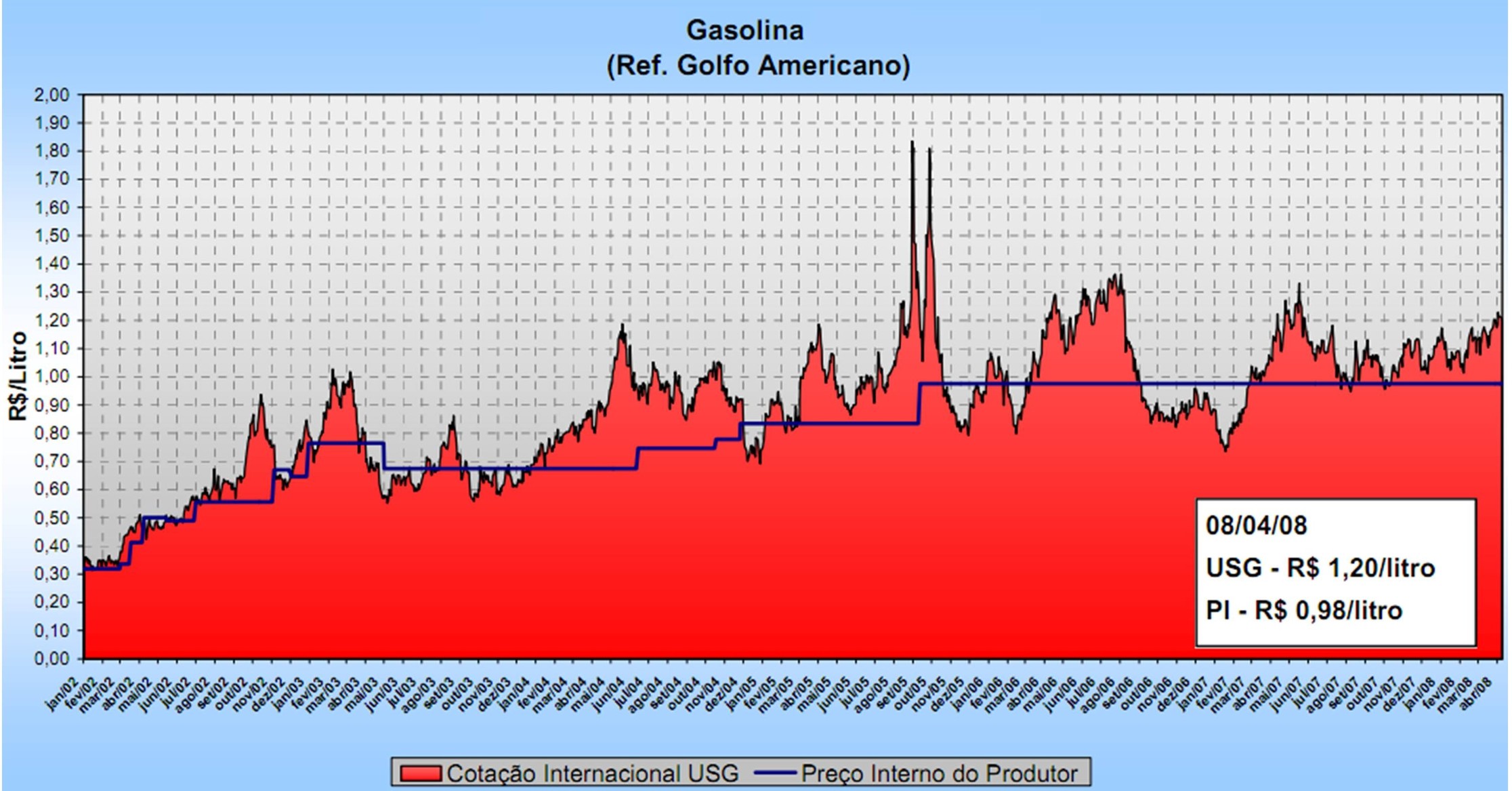

Envisioning growth and with the market opened, Ipiranga requested the ANP to increase its refining capacity to 17,000 barrels/day, which was authorized and effectively accomplished in 2002. In addition to increasing its capacity, the production profile was altered due to the ability to use more suitable raw materials, with the direct importation of more than half of the oil consumed starting in the second half of 1999 (RPR, 2014). However, difficulties soon emerged due to the escalating oil prices in the international market, associated with the lag in domestic prices of derivatives, mainly LPG, gasoline, and diesel, which made up Ipiranga’s portfolio. Figures 3 and 4 demonstrate the prices of LPG and gasoline, respectively, to illustrate the price lag recorded from the end of 2003.

Figure 3 – Evolution of LPG prices from 2002 to 2008 (Source: MME, 2008)

Graph Analysis: it is observed that from 2004 to 2008, the internal price (PI) of residential and industrial LPG remained below the international quotation, demonstrating the state subsidy for this fuel during that period.

Figure 4 – Evolution of gasoline prices from 2002 to 2008. (Source: MME, 2008)

Graph Analysis: it is observed that during various long periods, the internal price (PI) of gasoline was below the international quotation. Although at some points, the internal price was higher than the imported one, it was clear that it was under state subsidy for much longer.

In light of this scenario, between 2003 and 2006, the refinery reduced its operations by almost half, recording financial losses in its refining activity (RPR, 2014). The drop in production during these years can be seen in Figure 5.

Figure 5 – Average load processed at Ipiranga Refinery and its relation to the price of crude oil (Source: own elaboration based on ANP, 2017)

In 2007, control of the Ipiranga Group, whose assets included fuel distribution stations, petrochemical plants, and the Ipiranga Refinery, was acquired by a consortium involving Petrobras, Ultrapar, and Braskem. In 2009, the refinery changed its name to Refinaria de Petróleo Riograndense (RPR), in which each of the three controlling partners held 33.3% of the shares. From that point on, the refinery operated with some profit in its operations since Petrobras began to refine its own oil when the prices of crude and derivatives were causing losses to the unit. The future of this refinery is uncertain, due to the age of its facilities, load limitations, and small size.

Two New Small Refineries Emerge: Univen and Dax Oil

The paulista Univen and the baiana Dax Oil were two refineries created a few years after the opening of the oil market in Brazil. Aiming to occupy market niches or gaps left by Petrobras, they invested in small refining units compared to the state-owned giant refineries, to serve very specific markets with the production of special solvents. This model is, in fact, very common in the American market, which has over 100 small refineries spread across the country (TAVARES, 2005). Despite the promising start, the same problems faced by other private refineries soon emerged, exposed to high oil prices in the international market and domestic fuel price controls by the Brazilian Government.

Univen, a small refinery located in Itupeva, São Paulo, was founded in 1992 and acquired by the Vibrapar group in 1997. Initially, it produced only hexane, and in 2001, its industrial park was expanded, allowing it to also produce other special solvents. In 2003, it received authorization from the ANP to process and refine light crudes, petroleum condensate, naphtha, and other fractions of oil for the production of fuels and solvents (UNIVEN, 2014). In 2010, it was authorized to increase its processing plant from 6,919 barrels/day to 9,158 barrels/day (ANP, 2013).

The baiana Dax Oil is also a small private refinery located in the Camaçari Petrochemical Pole with a license to produce solvents since 2005, starting from the processing of naphtha and other petrochemical streams, which was expanded in 2010 to a refining capacity of 2,095 barrels/day (ANP, 2013). The unit was developed in partnership with the Federal University of Bahia (UFBA) and received support from the Government of the State and the Association of Oil and Gas Producers Extracted from Marginal Fields in Brazil (APPOM). It was a refinery designed to meet local production, allowing independent oil producers located in Bahia to market their oil production, which, being small, was not of interest to the larger companies.

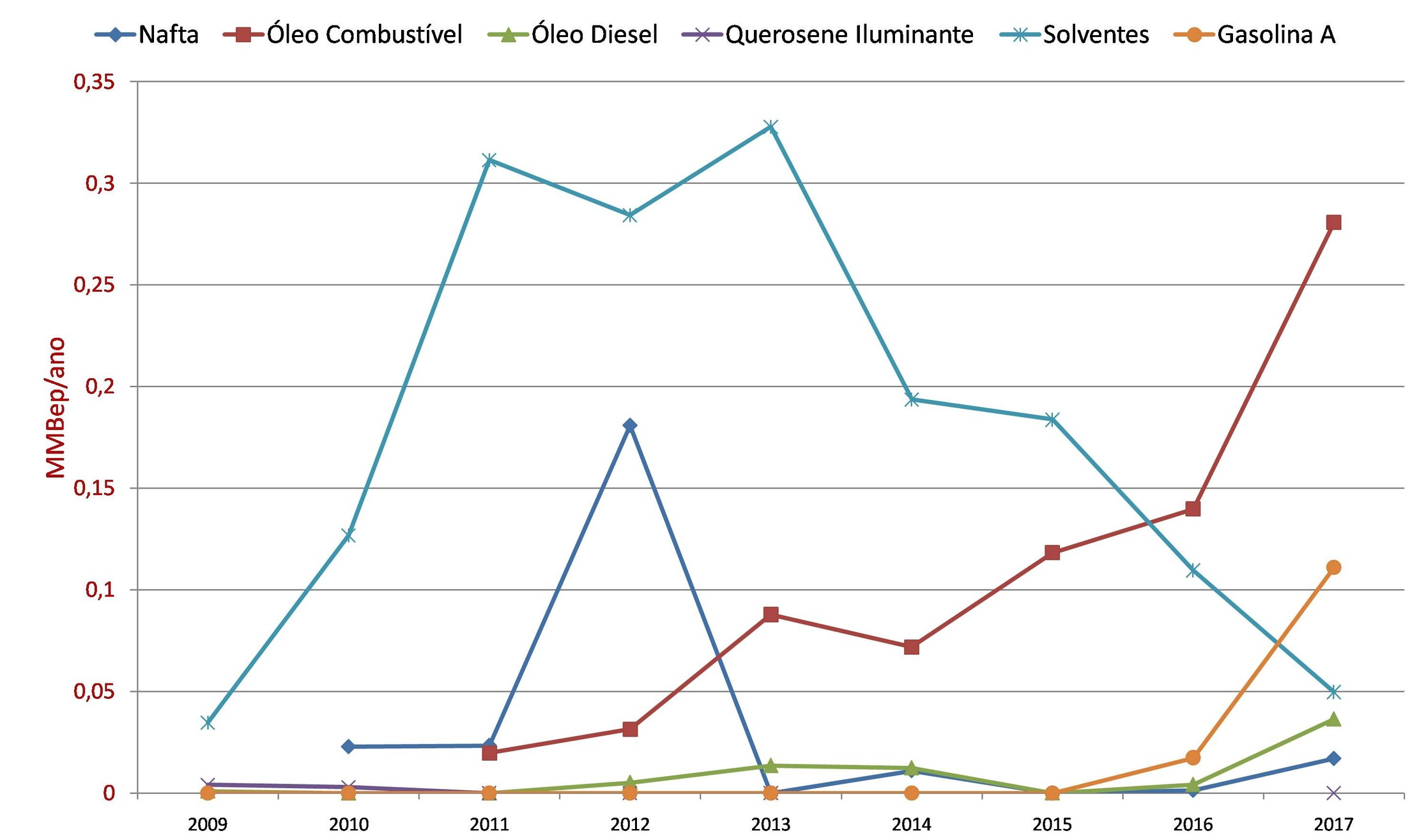

The two small refineries sought to adapt to market conditions. Univen, which initially produced more solvents in its unit, began to heavily invest in gasoline production starting in 2005 (Figure 6), with one caveat: it used the same method adopted by Manguinhos, paying the ICMS owed to the São Paulo treasury with government precatórios. Facing a price lag in the internal gasoline market compared to the international market, a strong dollar, and pressure from São Paulo’s treasury with respect to the ICMS, it began to produce less and less fuel, until halting operations in 2012 (the controller, Vibrapar Group, filed for bankruptcy and judicial recovery that same year). Meanwhile, Dax Oil, which initially produced solvents, shifted its focus to producing fuel oil (Figure 7) as a way to survive in the market. The small baiana refinery continues to operate, unlike its paulista counterpart, which has not operated since 2012.

Figure 6 – Historical profile of derivatives produced by Univen (Source: own elaboration based on ANP, 2017)

Figure 7 – Historical profile of derivatives produced by Dax Oil (Source: own elaboration based on ANP, 2017)

The Curious Case of REFAP

A curious case that well illustrates the difficulty of private refineries in Brazil is the joint-venture formed between Repsol YPF and Petrobras in 2001 at the Alberto Pasqualini Refinery (REFAP) in RS. As previously mentioned, the Spanish Repsol, as part of its strategy to expand its business in South America, acquired the Argentine state-owned YPF and part of the stock control of the Manguinhos Refinery (RJ) in Brazil. In 2001, in an asset exchange with Petrobras, Repsol acquired 30% of the Alberto Pasqualini Refinery (REFAP), in an operation that involved some refining, petrochemical, and fuel distribution assets on Argentine soil in favor of the Brazilian state-owned company.

One of Petrobras’s objectives at the time was to internationalize and dominate the market in the Southern Cone. REFAP then became an independent anonymous society (S/A), a subsidiary of Petrobras. With the new partnership, investments came for the expansion of its oil processing capacity in the subsequent years. Apparently, the Brazilian government was interested at that time in using the same business model in other Petrobras refineries, following the liberal economic trend that began in the 1990s. However, REFAP was the only refinery where this model succeeded as shortly afterward, in 2002, the then-president Lula’s government interrupted this trend.

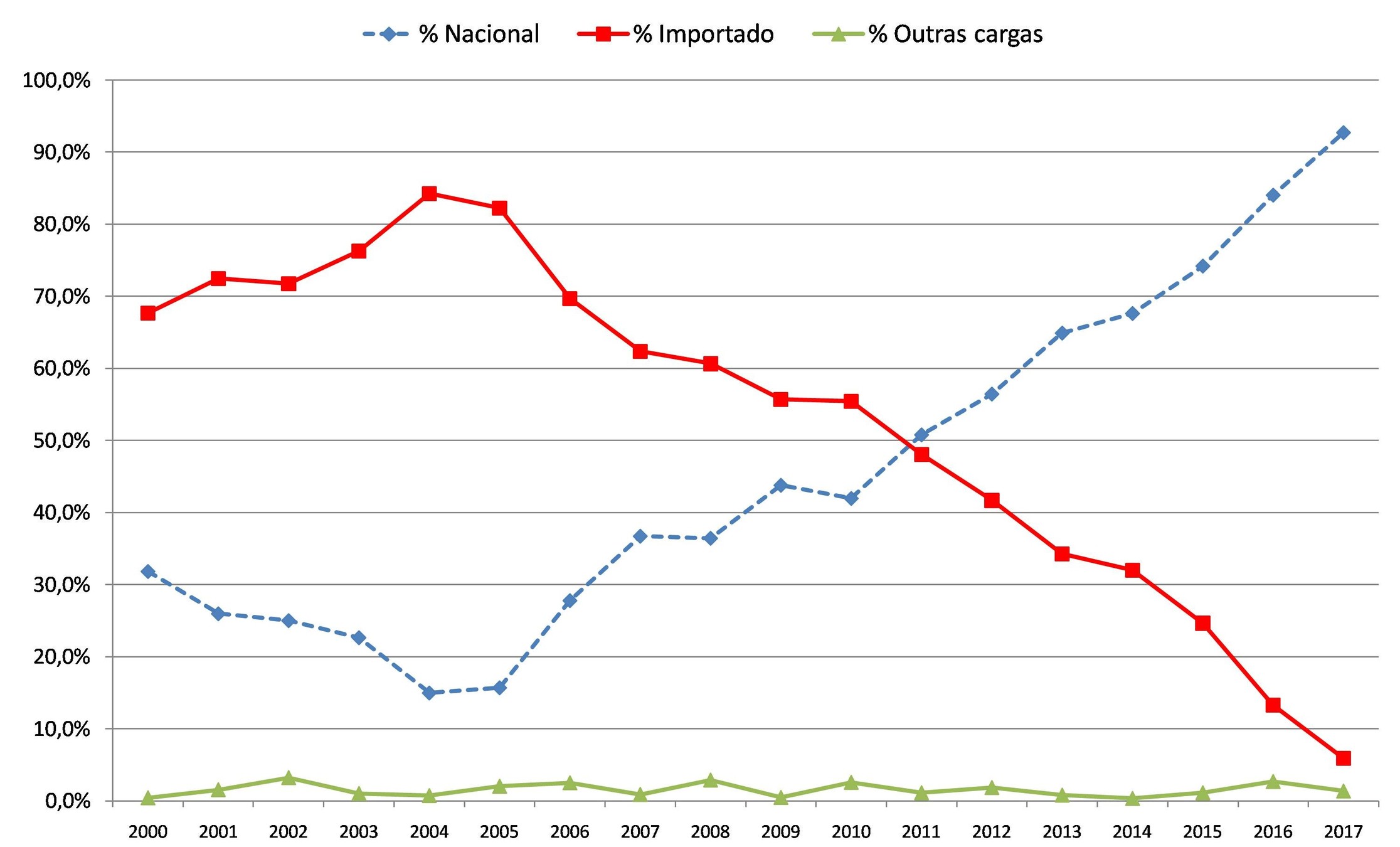

REFAP S/A, which at the time of its establishment already used 70% of imported light oil in its refining unit, began to import even more in the following three years (Figure 8), reaching 84% of the processed load in the year 2004. The priority at that moment was to obtain the highest possible production of light derivatives, which are known to have a higher added value. However, as previously discussed, the price of a barrel of oil in the international market began to rise steadily from 2003, significantly increasing the raw material costs, as was the case with other private refineries.

With heavy investments to recover what was referred to as the “barrel bottom” to reduce dependence on imported light oil, REFAP inaugurated, in 2006, its Delayed Coking Unit (UCR) and a Residue Catalytic Cracking Unit (RFCC), which allowed it to adjust its refining unit to Brazilian oil. It is noted that, in 2011, the use of national oil exceeded the imported oil in the oil blend used by the refinery, and in 2016 the use of national oil curiously reached 84% of the load (the same number recorded in 2004 with imported oil).

Figure 8 – Profile of oil used at REFAP (Source: own elaboration based on ANP, 2017)

Like other private refineries, with the increase in oil prices, REFAP began to experience negative refining margins. This was all compounded by the need for successive investments to modernize its plant and requirements for producing derivatives of better quality, with lower sulfur content. In light of this, at the end of 2010, after intense discussions regarding the need for new investments, which the partner did not agree to, Petrobras announced the repurchase of the 30% of shares held by Repsol, making the refinery once again 100% Petrobras. This curious case of REFAP demonstrates the difficulties faced by private refineries in the country since the reopening of the oil market in Brazil 20 years ago. SOURCE Marcelo Antunes Gauto, Industrial Chemist Petrobras

Be the first to react!