Português

Português  Inglês

Inglês  Espanhol

Espanhol

Reflections of Central Banks’ Behavior on Global Oil Demand

The global oil market dynamics is a constant and unpredictable dance of supply and demand. Recently, surprising expectations, U.S. crude oil stocks increased by 7.9 million barrels last week. In contrast, a Reuters poll projected a reduction of 510,000 barrels, presenting a discrepancy of over 8 million barrels. Refineries, in the meantime, are operating at full swing, at 93.7% of their capacity, producing 10.2 million bpd of gasoline and 5 million bpd of distillate.

The Central Bank Game and Its Reflections on the Oil Market

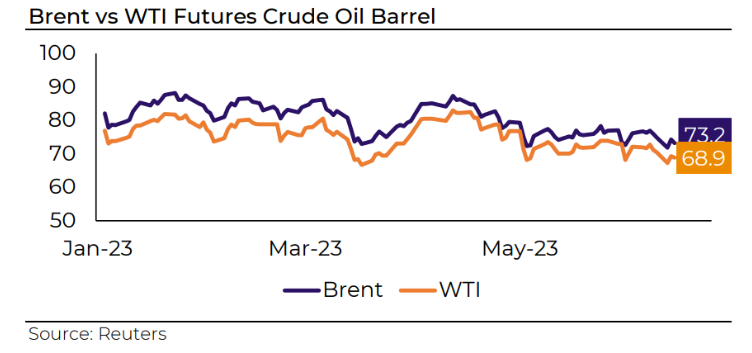

Although the U.S. Federal Reserve kept interest rates unchanged in its last meeting, a more aggressive (hawkish) stance from monetary authorities surprised the market, signaling possible interest rate hikes later this year, if necessary. This outlook resulted in a reaction in oil benchmarks, with Brent closing at US$73.20 (-1.47%) and the U.S. WTI oil barrel at US$68.27 (-1.66%).

However, the maintenance of interest rates in the U.S. helped to balance the game, resulting in gains of 2.55% and 2.29% at the end of last week, respectively.

-

Oncorp wins auction and enables biodiesel and gas thermal plants in Brazil, with strategic projects in Suape and Xavantes Aruanã.

-

Raízen Recovery: Shell Cosan May Reduce Control After R$ 65 Billion Debt

-

Outback Montes Claros: Chain Confirms First Unit in Northern Minas in 2026

-

Inpasa Creates Advisory Council and Brings José Olympio to Strengthen Corporate Governance

In parallel, on the political front, the Biden administration expressed its intention to repurchase at least 12 million barrels of oil for the Strategic Petroleum Reserve (SPR) in 2023. This measure responds to the sale of over 200 million barrels that took place the previous year, after Russia’s invasion of Ukraine, aimed at stabilizing oil markets and managing high prices at the pumps.

The European and Asian Scenario: Divergent Policies and Direct Impacts

Europe, in turn, is taking a different route. The European Central Bank raised interest rates by a quarter point, reaching the highest level in 22 years, and signaled that a new hike in July is very likely. As a result, the euro strengthened against the dollar, causing a spike in EU 2-year bond yields. In a chain of events, a weaker dollar makes oil cheaper for holders of other currencies.

Meanwhile, in Asia, the People’s Bank of China surprised with a cut in the short-term lending rate for the first time in months. This is an attempt by monetary authorities to restore market confidence and boost the local economy. This maneuver, in a weakened real estate and construction sector, makes the recovery of diesel demand more challenging, while the economic situation pressures demand related to travel for gasoline and kerosene.

Looking ahead, new counter-cyclical adjustments are expected as the Chinese government seems committed to providing stimulus and sustaining the country’s growth. It is important to highlight that refinery production in China increased by 15.4% in May compared to the previous year, with crude oil imports totaling 47.447 million metric tons (equivalent to 11.22 million bpd).

At the end of a busy week, speeches from monetary authorities, particularly from the Fed, leaving room for a possible interest rate hike, shook the markets. However, the sentiment that the contractionary monetary cycle is coming to an end, combined with optimistic news from China, fueled hopes for a more favorable outlook for global demand. Both oil benchmarks had a small weekly gain after declines in the last two weeks. Brent rose by 94 cents to US$76.61 (2.55%) and U.S. WTI gained $1.16 to US$71.78 (2.29%).

Credits: Press Advisory Content Communication

Seja o primeiro a reagir!