Portuguese

Portuguese  English

English  Spanish

Spanish

The Rapid Ascent of China as an Electric Power Challenges Petro-States, Alters Trade Flows and Repositions Global Energy, Technology and Carbon Emission Chains, Launching a New Era of Disputes Around Electrification.

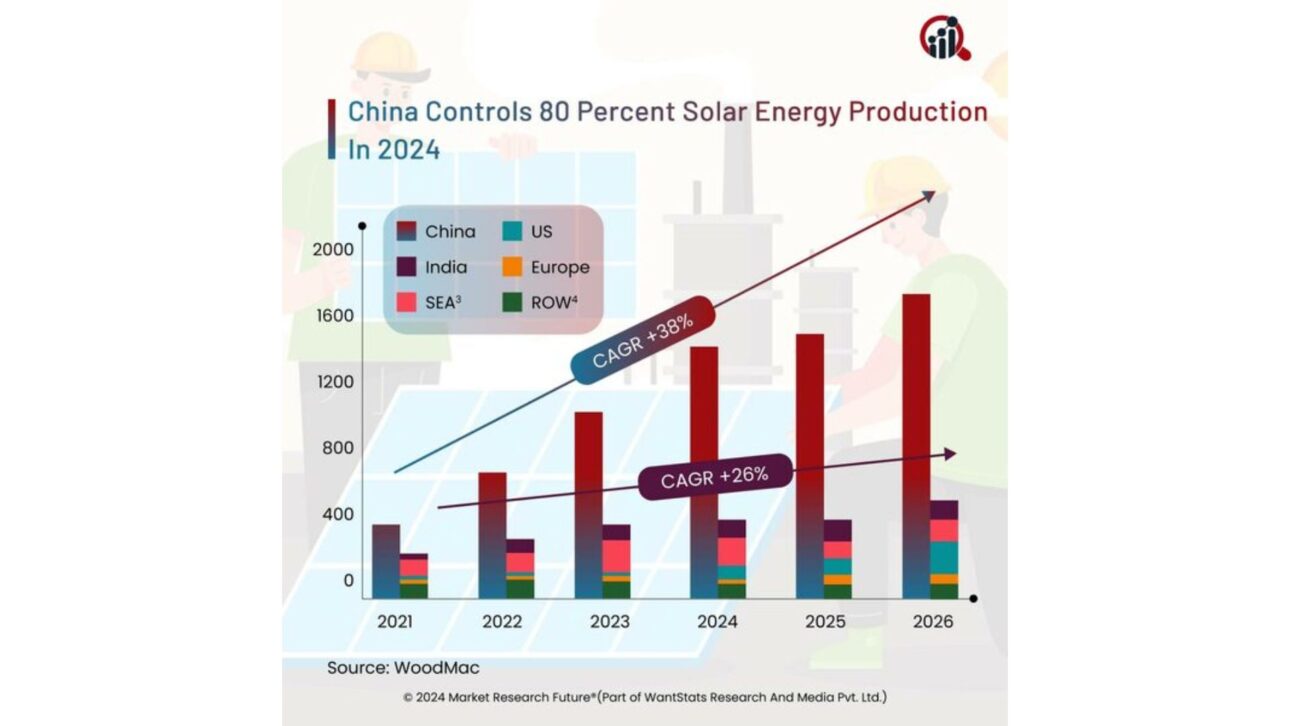

China has consolidated, in just a few years, an unprecedented position in the global energy order: it has become an “electrostate”, anchoring economic and geopolitical power in cheap electricity, clean technology supply chains, and an aggressive industrial policy.

This shift did not arise from climate altruism but from strategic calculation to reduce vulnerabilities in oil and gas while projecting influence through equipment, standards, and financing tied to electrification.

The movement is already translating into lower emissions by 2025 and direct pressure on the business model of petro-states.

-

The government requests the Federal Revenue Service for a new system to automate the income tax declaration, reducing errors, time, and bureaucracy for millions of Brazilians.

-

Pix in installments, international Pix, and contactless payment without internet: the Central Bank revealed the new features coming to the tool that is already used by almost every adult in Brazil.

-

Mercado Livre has just started selling medications with delivery in up to three hours to your door, and this move could completely change the way Brazilians buy medicines on a daily basis.

-

In Dubai, rising tensions from the war in the Middle East are causing super-rich individuals to leave the Gulf and direct their fortunes to a new financial refuge in Asia.

From Oil to Electrons: The Strategic Turn

The change comes from a decade of state planning.

In 2015, the government launched the Made in China 2025 program to elevate high-tech manufacturing and reduce external dependencies in critical sectors.

The chosen axis was large-scale electrification, with coordinated expansion of wind, solar, batteries, and electric vehicles, supported by industrial targets and public credit.

The priority was energy and technological security, not moral carbon goals.

What The Data Shows: Clean Generation and Emissions

Recent numbers help to gauge the turnaround.

In April 2025, the combined share of wind and solar reached 26% of the electricity generated in the country, a monthly record.

In 2024, the annual share of these two sources was 18%, reinforcing a trajectory of accelerated growth.

Meanwhile, 38% of total electricity came from low-carbon sources.

This dynamic contributed to a 1% drop in CO₂ emissions in the first half of 2025, extending the trend that began in March 2024.

Exports That Reduce Emissions Outside China

The spillover effect is already measurable.

Recent analysis estimates that Chinese exports of clean technologies in 2024 — solar panels, batteries, electric vehicles, and wind turbines — reduced 1% of annual CO₂ emissions in the rest of the world, close to 220 million tons.

The “embedded” emissions from the manufacturing of these products in China were offset in less than a year of use, given the carbon savings they provide at destination.

Pressure on Petro-States: When The Customer Changes Course

The Chinese energy reconfiguration directly affects hydrocarbon exporters.

Crude oil imports fell by 1.9% in 2024 compared to 2023, the first annual decline in two decades outside the pandemic period.

Projections from the International Energy Agency indicate that Chinese oil demand is expected to peak around 2027, as the rise of electric vehicles and efficiency reduces fuel consumption for transportation.

For countries like Russia and Saudi Arabia, the inflection of the main demand growth engine of the last decade is a game changer.

Coal Still Matters — And Is Being Repositioned In The Matrix

Despite the renewable leap, coal remains central to the Chinese power system.

New plants were commissioned in 2025, a result of the backlog of projects approved after the supply crises of 2021–2022.

At the same time, the average utilization rate of coal-fired power plants was around 50% in 2024, a sign of idle capacity that provides flexibility to meet demand peaks.

Since 2022, energy guidelines have directed that new units operate in a “support” or “regulatory” role — providing flexibility to the grid, rather than as inflexible baseload.

This movement has been reinforced by a capacity payment mechanism, introduced at the end of 2023 and operational from 2024.

In practice, the change is still gradual and coexists with contradictory incentives and inflexible dispatch rules.

Electrostates x Petro-States: A Map In Transformation

The Chinese rise inaugurates a provisional duality.

On one side, petro-states remain based on hydrocarbon exports, subject to price volatility and geopolitical shocks.

On the other, “electrostates” leverage renewables, storage, grids, and control of battery and panel supply chains to reduce costs and project power through exports of goods and technical standards.

This architecture tends to redistribute energy sovereignty: any country with sun and wind can generate its own electricity, mitigating dependence on imports and shielding itself from commodity fluctuations.

Europe is rushing to reduce industrial and supply bottlenecks, but starts from a less integrated position than China’s — thus facing higher transition costs.

The Sticking Point: Chemicals and Sectoral Emissions

However, there are friction points.

The advancement of the chemical industry — which converts coal into fuels and chemicals — added about 3% to China’s total emissions between 2020 and 2024.

The segment is growing to reduce imports of oil derivatives and secure strategic inputs, but it is carbon-intensive and hinders structural emission reductions in industry.

Even so, the contraction in emissions from the electricity sector and the slowdown in construction helped offset part of this increase in 2025.

What Changes For The Planet

The Chinese reorientation accelerates global decarbonization through practical pathways.

By reducing equipment costs and expanding supply, China universalizes access to key technologies that allow developing countries to install solar and wind generation, electrify fleets, and redesign electricity systems with storage.

At the same time, the outlook for peak oil demand makes long-term investments in exploration and refining riskier, rebalancing energy geopolitics.

Instead of barrels, power is now measured in installed gigawatts, control of critical minerals, and manufacturing capacity for batteries and semiconductors.

Against this new landscape, which countries will be able to convert cheap and stable electricity into lasting competitive advantage?

A China é o futuro, isso é um fato o incontornável.