Portuguese

Portuguese  English

English  Spanish

Spanish

Proposal Presented on September 19, 2025 Seeks to Exempt Teachers and Other Education Professionals from Income Tax. Measure Is Not Yet Valid and Depends on the Entire Process in Congress.

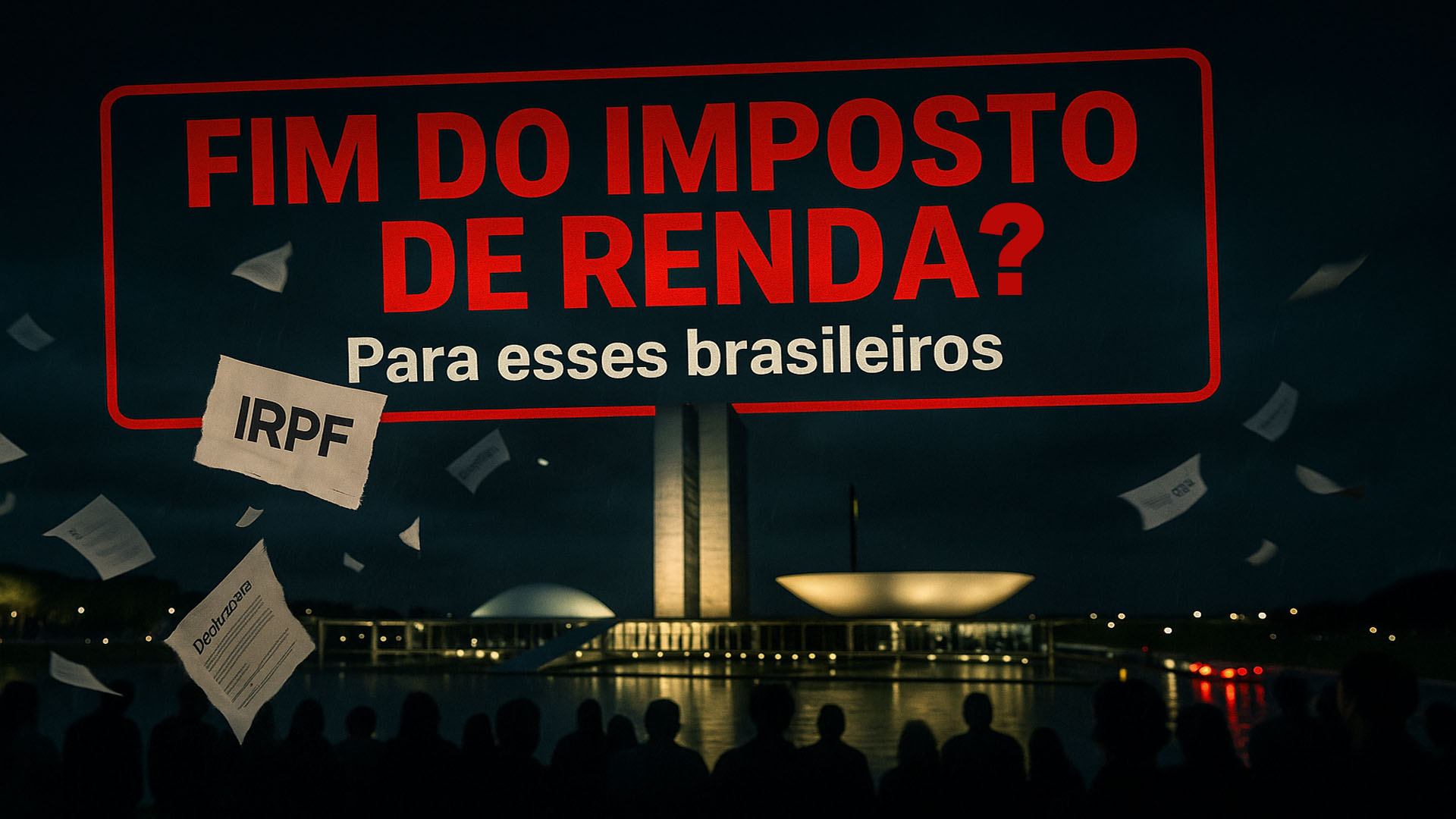

The Chamber of Deputies received, on September 19, 2025, Bill 4687/2025, authored by Deputy Professor Luciene Cavalcante (PSOL-SP), which exempts the Personal Income Tax (IRPF) on the earnings of teachers and technical and administrative workers in basic and higher education. The proposal amends provisions of Law 7.713/1988. Currently, the bill is “Awaiting Dispatch from the President of the Chamber”.

According to the justification, the exemption recognizes the strategic role of education professionals and seeks to reduce the tax burden on salaries considered low. The text refers to Article 61 of the LDB, which defines who is included in the group of “education professionals.”

It is worth noting that there is not yet a confirmed end to the Income Tax for this group, as reported by some sources. The initiative is a proposal and must go through all stages of the legislative process before becoming law.

-

The noise law will no longer be in effect at 10 PM starting in June with a new rule valid during the 2026 World Cup.

-

The Chamber opens a debate on driver’s licenses at 16 years old as part of a reform that includes around 270 proposals to change the Brazilian Traffic Code and may redesign rules for licensing, enforcement, and circulation in the country.

-

The new Civil Code could revolutionize marriages in Brazil with “express divorce” and changes that could exclude spouses from inheritance.

-

Banco do Brasil sues famous influencer for million-dollar debt and intensifies debate on delinquency, risks of seizure, and direct impact on Gkay’s credibility.

What Does Bill 4687/2025 Say and Who Would Benefit

The bill proposes a total IRPF exemption on income received by teachers and technical/administrative professionals working in educational institutions, both basic and higher. The text suggests adjustments to Law 7.713/1988, a regulation that currently lists exempt cases for individuals, but does not encompass an entire professional category like education.

The LDB defines who the education professionals are. According to Article 61, it includes teachers, professionals with pedagogical training, and other members of the school staff, in effective exercise. This legal basis is what the bill uses to expand the scope of the exemption beyond the classroom.

In the justification, the author lists low remuneration, disinterest in the career, and dropout of professionals as issues that the exemption would help mitigate. There is also a public campaign with a petitions encouraging support for the project.

Project Not Yet Valid: Understand the Stages of Processing in Congress

Currently, the bill awaits dispatch for distribution to thematic committees. Afterward, it goes through merit analysis and can receive amendments. If approved, it proceeds to the Plenary and then to the Federal Senate. Once voting is completed in both Houses, the text goes for presidential sanction. Until then, nothing changes for taxpayers.

Projects can proceed in a conclusive manner in committees, but the proposal can be brought to the Plenary by appeal. After any changes, there may be revision in the other House and, ultimately, sanction or veto either totally or partially by the Executive.

This process tends to be long and depends on political agreements and available space on the agenda. Thus, any deadline or “effective date” publicized outside the official stages is not valid.

How the Proposal Relates to Other Changes in Income Tax

At the same time, the Senate approved in the CAE (Sept. 24, 2025) a text that raises the income tax exemption threshold to up to R$ 5 thousand (Bill 1.087/2025). This measure is not specific to education and still depends on legislative processing. They are distinct fronts: one sectoral (education) and another broad (all taxpayers).

There are also other proposals on education in the Chamber, such as Bill 1162/2025, which exempts earnings of teachers (with different cuts and related adjustments). This shows an active legislative environment, but uncertain regarding the final model.

While the projects are in process, the exemptions already provided in Law 7.713/1988 continue to apply, such as for retirement benefits for individuals with serious illnesses, according to guidance from the Federal Revenue. Active professionals do not fall under these current provisions.

In your opinion, is it fair to exempt the entire education category or should it be to expand the exemption threshold for all taxpayers? Comment below.

-

-

-

9 pessoas reagiram a isso.