Portuguese

Portuguese  English

English  Spanish

Spanish

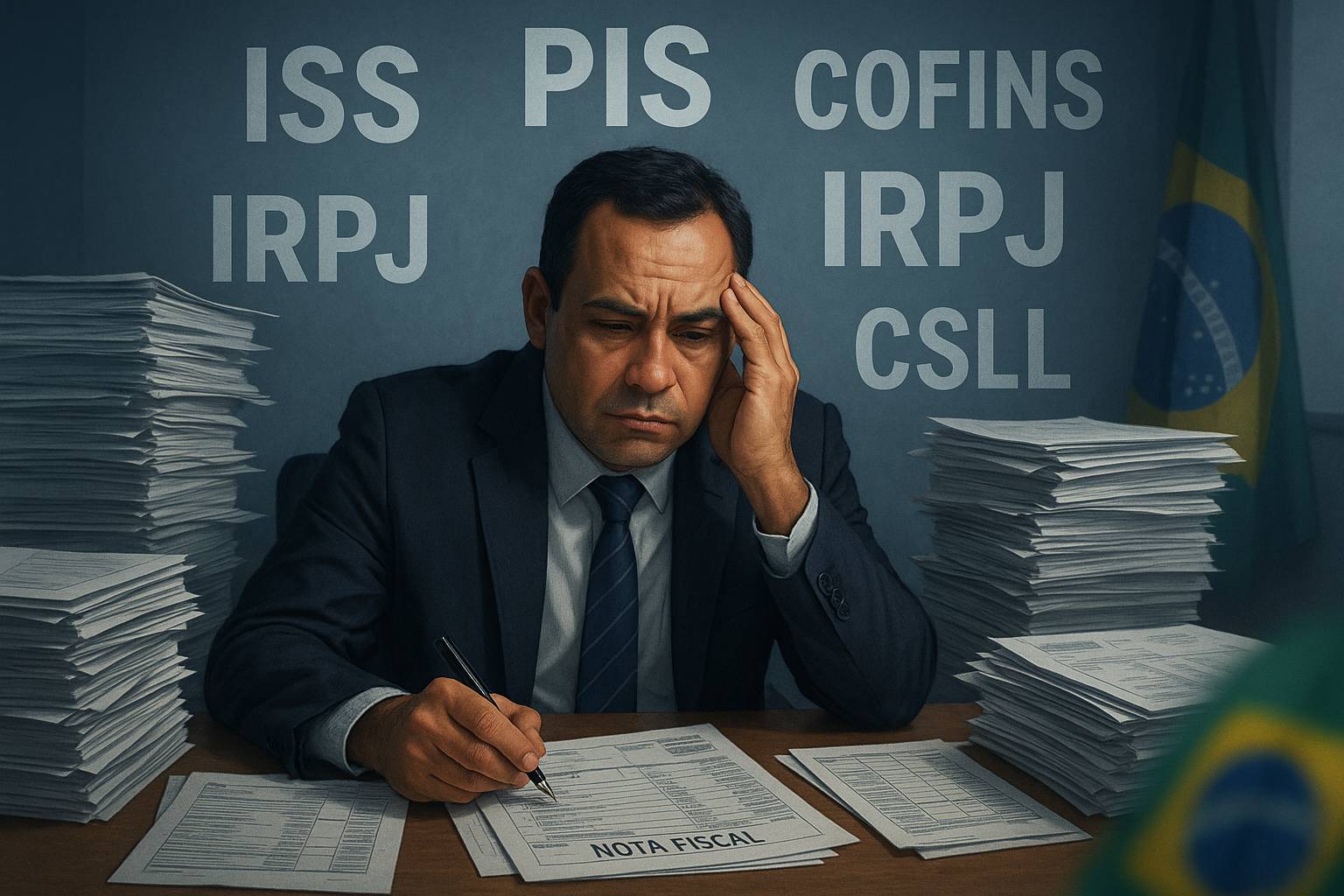

Discover How Much Your Company Really Delivers to the Government — and How Each Tax Affects Your Profit

Few people realize, but the tax burden on Brazilian companies goes far beyond the simple “invoice + tax”. Between municipalities, states, and the Union, five taxes shape the cost of existence: ISS, PIS, COFINS, IRPJ, and CSLL.

Each of these taxes has its own logic, calculation base, and specific exceptions. Together, they determine how much profit really remains at the end of the month, influencing financial and strategic decisions.

According to the Federal Revenue Service, over 95% of Brazilian companies choose Presumed Profit or Simple National, as they are less complex and bureaucratic regimes than Actual Profit, which requires detailed and controlled accounting.

-

Mothers and daughters come together, create an ‘express’ beauty salon and turn the idea into a network with 21 units, revenue of R$ 16.7 million and 12,000 subscribers.

-

End of the 6×1 schedule: how the reduction of hours can affect service companies, industry, and agribusiness.

-

Brazil Ignores Trump’s threats to BRICS, Buys 42 tons of gold and reduces the Dollar’s share by 6.45% in international reserves.

-

Havan buys historic football land in Blumenau for a million-dollar amount protected by a confidentiality clause and is already planning to change even the layout of streets to build a megastore in half-timbered style costing 80 million reais.

ISS – The Tax That Depends on Your Zip Code

The Service Tax (ISS) is municipal and applies to services listed in Complementary Law No. 116/2003, updated by LC 157/2016, which set a minimum rate of 2% and a maximum of 5%.

Each municipality defines the percentage within this range. When the service is exported and the result occurs outside the country, ISS is not charged, according to Article 2, sole paragraph of LC 116/2003.

This means that a Brazilian consulting firm providing services to a foreign company can be exempt from ISS, provided it proves that the result of the work was indeed enjoyed abroad.

PIS and COFINS – The Federal Duo on Revenue

These federal contributions apply to gross revenue and represent a significant part of the tax burden. The difference between them lies in the calculation regime and the ability to generate tax credits.

Companies under Presumed Profit follow the cumulative regime, paying 0.65% of PIS and 3% of COFINS on total revenue. Those under Actual Profit use the non-cumulative regime, with 1.65% and 7.6%, respectively.

Under the non-cumulative regime, businesses can generate tax credits on inputs, electricity, rent, and operational expenses. This compensation reduces the payable amount and encourages cost control.

There is also a relevant detail: financial income, such as earnings and investments, is subject to taxation of 4.65% in total (0.65% of PIS + 4% of COFINS), according to Decree 8.426/2015.

IRPJ – The Heart of the Profit Tax

The Corporate Income Tax (IRPJ) has a basic rate of 15% on profit, with a 10% additional on the portion that exceeds R$ 20,000 per month or R$ 60,000 per quarter.

According to the Income Tax Regulation of 2018 (RIR/2018), the IRPJ can be calculated under the regimes of Actual Profit, Presumed Profit, or Arbitrated Profit, depending on the company’s accounting structure.

The Actual Profit considers accounting profit adjusted for legal additions and exclusions. In contrast, the Presumed Profit applies fixed percentages on gross revenue, ranging from 8% to 32%, depending on the activity.

The STJ, in Theme 1008, decided in 2024 that ISS and ICMS compose the calculation base for IRPJ and CSLL under Presumed Profit, increasing the final tax amounts.

CSLL – The “Sister” of IRPJ

The Social Contribution on Net Income (CSLL) was created to finance social security and closely tracks the IRPJ, following the same bases and calculation methods.

The standard rate is 9%, but financial institutions and insurers pay 15%, according to the Federal Revenue Service. The calculation follows the same presumed percentages used for IRPJ under each regime.

Under Presumed Profit, the presumed base is 32% of revenue for services and 12% for commerce and industry. In contrast, in Actual Profit, it directly affects the adjusted net profit.

How Everything Connects

ISS taxes the service rendered, PIS and COFINS tax the revenue, while IRPJ and CSLL are levied on profit. Together, they form the core of the business tax burden.

The main difference between Actual Profit and Presumed Profit lies in how profit is calculated. The former considers the real accounting result, while the latter presumes fixed margins on revenue.

The presumed margins are defined by Law No. 9.718/1998 and range from 8% to 32%, depending on the sector. In contrast, Actual Profit allows for the deduction of expenses but requires detailed accounting structure.

Scenario 1: Service Company Under Presumed Profit

Imagine a consulting firm that bills R$ 900,000 per quarter. The municipality charges 5% ISS, resulting in R$ 45,000 on the total invoices issued.

The IRPJ, with a presumed base of 32%, generates R$ 288,000. Applying 15%, we get R$ 43,200, adding an additional R$ 22,800, totaling R$ 66,000 in quarterly tax.

The CSLL also applies to R$ 288,000, with a rate of 9%, generating R$ 25,920. The PIS and COFINS, combined, amount to 3.65% on R$ 900,000, resulting in R$ 32,850.

The total tax amount for the quarter is approximately R$ 169,770. It is important to remember that the ISS paid is still included in the calculation base for IRPJ and CSLL.

Scenario 2: Commerce Under Presumed Profit

A store that bills R$ 1,200,000 per quarter does not pay ISS but must collect IRPJ, CSLL, PIS, and COFINS. The calculation bases follow percentages defined by law.

The IRPJ has a base of 8%, totaling R$ 96,000. Applying 15%, it results in R$ 14,400, plus an additional of R$ 3,600, reaching R$ 18,000 for the quarter.

The CSLL uses a base of 12%, totaling R$ 144,000. Applying 9%, we get R$ 12,960. The PIS and COFINS, at 3.65%, correspond to R$ 43,800.

Adding everything up, the total burden reaches R$ 74,760 for the quarter. This amount may still vary with incentives, monophase regimes, or tax substitutions.

Scenario 3: Industry Under Actual Profit

A factory that bills R$ 1,500,000 and has costs of R$ 900,000 follows the non-cumulative regime for PIS and COFINS, allowing tax credits on the inputs purchased.

The debit is R$ 138,750 and the credit is R$ 83,250, resulting in R$ 55,500 net. The net profit, considering costs and expenses, is R$ 300,000.

The IRPJ, at 15%, generates R$ 45,000 and an additional of R$ 24,000, totaling R$ 69,000. The CSLL at 9% adds R$ 27,000, summing R$ 151,500 for the quarter.

And What If the Service is Outside Brazil?

In service exports, ISS does not apply, provided that the result occurs outside, according to Complementary Law 116/2003. This can significantly reduce the tax burden.

Even so, PIS, COFINS, IRPJ, and CSLL remain applicable, as they are federal taxes. The difference lies in how revenue is classified and evidenced in the accounting balance.

Companies in software, engineering, and design serving foreign clients often take advantage of this partial exemption, making their services more competitive globally.

The Cost of Complexity

The Brazilian tax system is among the most complex in the world. According to the World Bank, companies spend 1,501 hours per year just to comply with tax obligations.

This complexity weighs more on small businesses, which have less accounting structure. Without guidance, many end up paying more taxes than they should.

Tax planning is essential to reduce costs. With simulations and accounting control, it is possible to anticipate scenarios and choose the most advantageous regime for each type of business.

How Do the United States Tax Companies?

In the United States, the logic is the opposite. The system prioritizes direct taxes, mainly the Income Tax. Companies pay taxes based on net profit, not on revenue.

There is the federal Corporate Income Tax, with a fixed rate of 21% since 2018, plus state profit tax (averaging between 4% and 10%, depending on the state).

The Sales Tax, equivalent to our ICMS, exists but is much simpler — charged only at the final stage of sale to the consumer. This eliminates cumulative taxation and simplifies accounting.

See a comparison of tax collection from the 5 largest economies in the world (do not consider Brazil in this table):

| Country | Tax Burden (% of GDP) | Predominant Structure | Economic Observation |

|---|---|---|---|

| Brazil | 33.1% | Taxes on consumption and revenue (ISS, ICMS, PIS/COFINS) | High complexity and compliance costs; 1,501 hours/year to pay taxes (World Bank) |

| United States | 25.4% | Taxes on income and profits | Simple, digital, and predictable system; focus on direct collection and lower burden on consumption |

| China | 28.0% | Taxes on production and corporate income | Hybrid model focused on state-owned enterprises; strong centralized control |

| Japan | 31.4% | Taxes on income, consumption, and social security | Stable system with high funding for social security |

| Germany | 38.9% | Taxes on income, profits, and payroll | High taxation, but offset by a strong social welfare network |

| India | 18.0% | Taxes on goods and services (GST) and income | Unified system since 2017 (Goods and Services Tax), reducing bureaucracy and evasion |

Planning is Surviving

Understanding regimes and controlling cash flow helps to reduce the tax burden. Actual Profit allows for credits and deductions, while Presumed Profit offers operational simplicity.

Monitoring decisions from the STJ and STF is essential, as legal changes can significantly alter the calculation bases and profit margins.

Planning, simulating, and tracking case law is not a luxury. It is a survival strategy in a tax system that is constantly changing and directly impacts business profitability.

Official and Legal Sources

Federal Revenue Service of Brazil — guidance on IRPJ, CSLL, PIS, and COFINS. Complementary Law No. 116/2003 and LC No. 157/2016 — ISS rules. Law No. 10.637/2002 and No. 10.833/2003 — non-cumulative PIS and COFINS. Law No. 9.718/1998 — base for the cumulative regime. Decree No. 8.426/2015 — taxation on financial income. RIR/2018 — Income Tax Regulation. STJ (Theme 1008, 2024) — inclusion of ISS and ICMS in IRPJ and CSLL.

The Brazilian tax system is a true labyrinth, but understanding ISS, PIS, COFINS, IRPJ, and CSLL is the first step to escaping it. Planning and acting strategically is the secret to business survival.

Do you believe that the excess of taxes in Brazil is the result of poor management or a lack of political will to simplify the system?

Seja o primeiro a reagir!