Portuguese

Portuguese  English

English  Spanish

Spanish

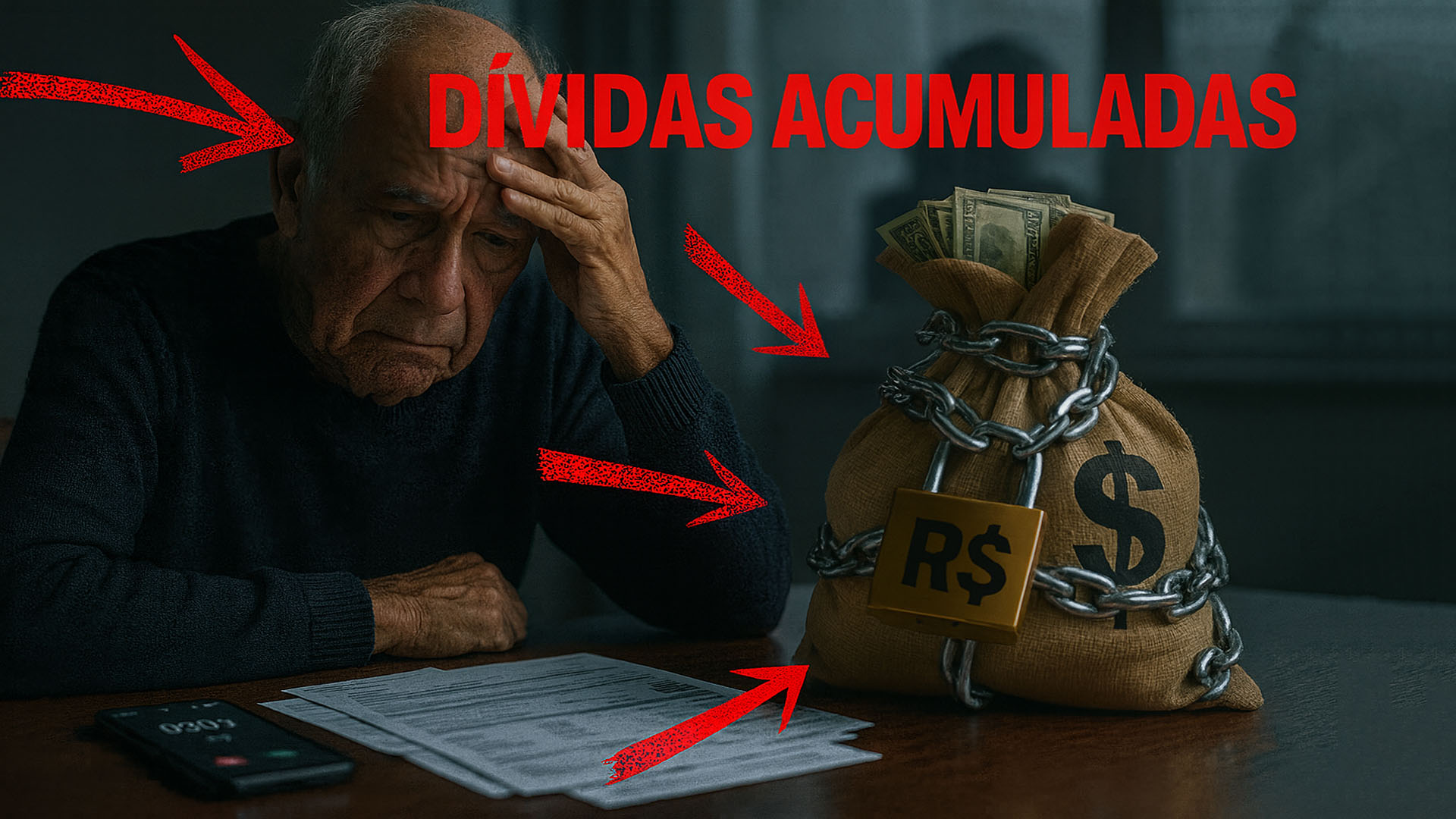

The 2021 Law Strengthened Information Duties and Created Debt Rescheduling, but Aggressive Telemarketing, RMC/Payroll Loans, and Refinancings Continue to Pressure Retirees

Law 14.181/2021 amended the Consumer Protection Code to prevent over-indebtedness and enable global debt rescheduling. The rule reinforced transparency duties, prohibited harassment in credit offers, and protected the “existential minimum.” According to the official text, it is prohibited to harass or pressure the consumer, with special focus on the elderly.

In practice, the procedure includes a first stage of conciliation between the debtor and all creditors, and if there is no agreement, it allows the judge to review contracts and integrate abusive clauses. Courts detail this procedure in two phases, both anchored in Arts. 104-A and 104-B of the Consumer Protection Code.

Since 2022, the federal government and the CNJ have been coordinating actions to enhance the application of the law, with training for consumer protection agencies and outreach efforts. The institutional cooperation was formalized in 2024 to scale up renegotiations.

-

The noise law will no longer be in effect at 10 PM starting in June with a new rule valid during the 2026 World Cup.

-

The Chamber opens a debate on driver’s licenses at 16 years old as part of a reform that includes around 270 proposals to change the Brazilian Traffic Code and may redesign rules for licensing, enforcement, and circulation in the country.

-

The new Civil Code could revolutionize marriages in Brazil with “express divorce” and changes that could exclude spouses from inheritance.

-

Banco do Brasil sues famous influencer for million-dollar debt and intensifies debate on delinquency, risks of seizure, and direct impact on Gkay’s credibility.

Consumer protection agencies report significant outcomes when the case reaches the conciliation table. In São Paulo, Procon reports a high success rate and a significant reduction in charges after hearings at the Over-Indebtedness Center.

Elderly Remain Vulnerable to Payroll Loans

Retirees and pensioners from the INSS have allowable payroll deduction of up to 45% of the benefit: 35% for loans, 5% for credit cards, and 5% for benefit cards. This division arises from legal changes approved in 2022 and detailed by Congress.

This structure facilitates hiring but also increases risk when there is aggressive selling and inadequate information. The Consumer Protection Code now requires transparency regarding total effective cost, interest rates, and the consequences of delays, precisely to reduce traps in credit contracts.

Even so, telemarketing and persistent approaches remain under scrutiny from authorities. Anatel continues to implement measures against abusive calls and recommends registering in the “Do Not Disturb” service to block payroll loan offers; over a thousand companies have already had their access blocked. In August 2025, the agency relaxed the mandatory use of the prefix 0303, reigniting the debate on oversight.

Delinquency among individuals aged over 60 years remains significant in the country. Data from Agência Brasil based on Serasa’s Report indicates that at the end of 2024, the elderly represented about one-fifth of those in default.

The Loopholes: RMC/Payroll Loan, Portability, and “Change” in Refinancing

A recurring source of litigation is the Payroll Margin Reserve (RMC) linked to payroll loans, when the discount on the paycheck persists as the “minimum” of the card without the elderly realizing the revolving nature of the debt. Recent rulings have suspended discounts and in some cases converted the RMC into traditional payroll loans based on average rates.

The portability of payroll loans, useful for reducing interest, has been exploited by players competing for clients with aggressive offers. In 2024, the government recorded a spike in portability operations, as well as refinancing with “change”, which releases funds into an account and extends the total term. These movements increase the stock and can mask indebtedness.

The problem worsens when the consumer does not receive clear information about total cost and remaining time after migration. The Over-Indebtedness Law requires this detailing and forbids advertising that leads to the belief of credit “with no interest” or “without evaluation.” Complying with this rule is the supplier’s obligation, not a courtesy.

Without proper verification of payment capacity, retirees end up compromising the existential minimum, precisely what the law seeks to safeguard. In case of abuse, the path is to document the offer, keep prints and statements, and contact Procon or the judiciary to stop discounts.

Rates and Volume of Payroll Loans: Where We Stand in 2025

The National Social Security Council raised the ceiling for INSS payroll loan interest to 1.85% per month in March 2025. This level reflects the trajectory of the Selic and pressures the net income of those already operating at the margin limit.

In parallel, the volume of operations surged in 2024. Official data from Social Security shows a significant increase in portabilities and refinancings, indicating that competition among banks has shifted to the battle for already indebted clients.

In consumer credit, the Central Bank recorded double-digit expansion in 2024, highlighting higher-cost modalities. The environment reinforces the importance of checking CET, terms, and avoiding multiple contracts “adding up payments” on the same paycheck.

The combination of interest rates, extensions, and products like payroll loans creates a “debt treadmill” difficult to interrupt without institutional intervention or structured renegotiation with all creditors. This is where the law can make a difference.

What to Do If You Are Over-Indebted

Those who are already over-indebted can request rescheduling at Procon or in court, presenting a payment plan that preserves the existential minimum. Global conciliation tends to reduce fines, charges, and organize the liability into a viable timetable.

To curb persistent calls and proposals, use the “Do Not Disturb” service and report abusive calls to Anatel. Keep protocols, and in case of contracting over the phone without consent, request a recording and a copy of the contract.

Before signing, compare CET, term, and embedded insurance. Be wary of easy “change” offers and promises to pay off old debts without increasing the total cost. The rule is simple: if the installment fits because the term has been extended, confirm that the total amount payable has not exploded.

If there is an undue discount due to RMC/payroll loan, immediately request cancellation and seek Procon to suspend the charge and assess judicial measures. Several courts have recognized consent defects in contracts with the elderly.

We Want to Hear From You: the prefix 0303 became non-mandatory in 2025. Did this make life easier for consumers or open the door to more credit harassment? Share your experience with payroll loans, RMC, and portability in the comments and point out what practices need to change.

Great article, thank you for sharing these insights! I’ve tested many methods for building backlinks, and what really worked for me was using AI-powered automation. With us, we can scale link building in a safe and efficient way. It’s amazing to see how much time this saves compared to manual outreach.