Portuguese

Portuguese  English

English  Spanish

Spanish

The Social Security Reform of 2019 Created 50% and 100% Tolls That Allow Those Who Had Already Contributed Before to Escape the New Minimum Age of the INSS, Complete Time with Additional Years, and Retire Using Transition Rules That Are More Lenient Than the Definitive Ones for Workers in the RGPS of the Private Sector Overall

Since November 13, 2019, when the Social Security Reform came into effect, retirement under the General Regime started to require a minimum age of 62 for women and 65 for men, along with new contribution times. At the same time, transition rules were created for those who were already in the market and could be affected by the new minimum age of the INSS.

In these transitional rules, mechanisms such as the 50% toll and the 100% toll emerged, designed precisely for insured individuals who were close to completing the contribution time under the old rules. In several cases, especially for those who already had a long contribution history before 2019, these tolls allow escaping the age progression and maintaining more favorable retirement conditions.

What Changed in Retirement After the Reform

The general rule established by the reform for private sector workers provides:

-

Brazilian city bets on the business environment to generate jobs and attract investments in the energy sector — secretary reveals strategy at Macaé Energy 2026.

-

50 viaducts, 4 tunnels, 28 bridges, and 40 kilometers of bike paths: BR-262 in Espírito Santo will receive 8.6 billion reais for the largest engineering project in the state’s history, inspired by the Immigrant Highway in São Paulo.

-

Brazil produces too much clean energy and doesn’t know what to do with it: over 20% of solar and wind capacity was wasted in 2025 while investors flee and 509 renewable generation projects were abandoned in the last year.

-

Piauí will produce a new fuel that replaces diesel without needing to change anything in the truck’s engine and reduces pollutant gas emissions by half: truck drivers from all over the Northeast are already celebrating the news that will arrive later this decade.

Women: minimum age of 62 and at least 15 years of contribution

Men: minimum age of 65 and, in general, 20 years of contribution

These parameters became definitive, while the gradual adjustments were concentrated in the transition rules.

The logic was to separate those who entered the system after 11/13/2019, who are directly subject to the new requirements, from those who had already been contributing and gained access to intermediate paths to soften the impact of the changes.

Transition Rules for Those Who Had Already Contributed Before 11/13/2019

For insured individuals who were already contributing to the INSS in November 2019, the reform structured a set of transition rules.

Among them, three modalities appear more frequently in practice:

Point Rule: adds age and contribution time, requiring 30 years of contribution for women and 35 for men, with a minimum score that increases year by year

Minimum Age Rule with Contribution Time: combines a fixed number of years of contribution with ages that gradually rise until reaching 62 years for women and 65 for men

Age Rule: maintains 15 years of contribution, with a minimum age of 62 for women and 65 for men, which has been stabilized since 2023

In addition to these, the 50% and 100% toll rules come into play, which have their own functioning and are directly linked to how much time was left, on 11/13/2019, to complete the minimum contribution time of the old rule (30 years for women and 35 for men).

How the 50% Toll Works

In the 50% toll, the starting point is the time that was missing, on 11/13/2019, to reach the minimum of 30 years of contribution (woman) or 35 years (man) of retirement for contribution time before the reform.

The rule works like this:

It checks how much time was missing on 11/13/2019 to reach 30/35 years

On this remaining period, a 50% additional is applied

The insured must complete the minimum contribution time added to this toll

There is no minimum age requirement in the 50% rule

In practice, those who already had a lot of contribution time accumulated before the reform can complete the toll without submitting to the new minimum age of the INSS, as long as they reach the required time plus the 50% increase on the period that was still due in November 2019.

How the 100% Toll Works

The 100% toll also starts from the time that was missing, on 11/13/2019, to reach 30 years of contribution (woman) or 35 years (man).

The difference is in the percentage and the age requirement:

The same minimum time of 30/35 years of contribution is required

The insured needs to contribute for an additional period corresponding to 100% of the time that was missing on the date of the reform

There is a fixed minimum age: 57 years for women and 60 years for men

These ages do not increase year by year, remaining stable in the toll rules

In other words, the ages of 57 and 60 years in the 100% toll do not follow the progression of the new minimum age of the INSS, which keeps the transition frozen for those who fit into this model.

Who Escapes the New Minimum Age in the Toll Rules

The most common question among insured individuals who had already contributed before 2019 is whether it is still possible to avoid the increase in the age required for retirement.

By the design of the rules, those who had, in November 2019, a high contribution time can stay out of the age change in the two transitions by toll.

Objectively, the text highlights that those who had 28 years and 1 day of contribution in November 2019 were already sufficiently close to the 30 years required for women under the old rule.

In these cases, the calculation of the toll starts from a relatively small missing time, which makes it feasible to meet the requirement without depending on the annual age progression in the other rules.

In both toll modalities, the basic mechanism remains:

50% Toll: does not require a minimum age, and this absence of age does not change over the years

100% Toll: requires 57 years for women and 60 years for men, and these ages are fixed, without annual increase

Thus, those who met the necessary conditions on 11/13/2019 can, in many cases, fulfill the toll and retire without facing the new minimum age of the INSS applied to the definitive rules.

Practical Timeline After the Social Security Reform

To understand the path of those who intend to use the toll rules, the process can be seen in successive stages:

Before 11/13/2019

The insured contributed normally, accumulating contribution time under the old legislation, which allowed retirement by contribution time without minimum age in certain modalities.

11/13/2019 – Entry into Force of the Reform

The reform came into effect, establishing the new minimum age of the INSS and creating the transition rules, including the 50% and 100% tolls. On this date, the benchmark was defined for calculating how much time was left to reach 30/35 years of contribution.

After 11/13/2019 – Planning

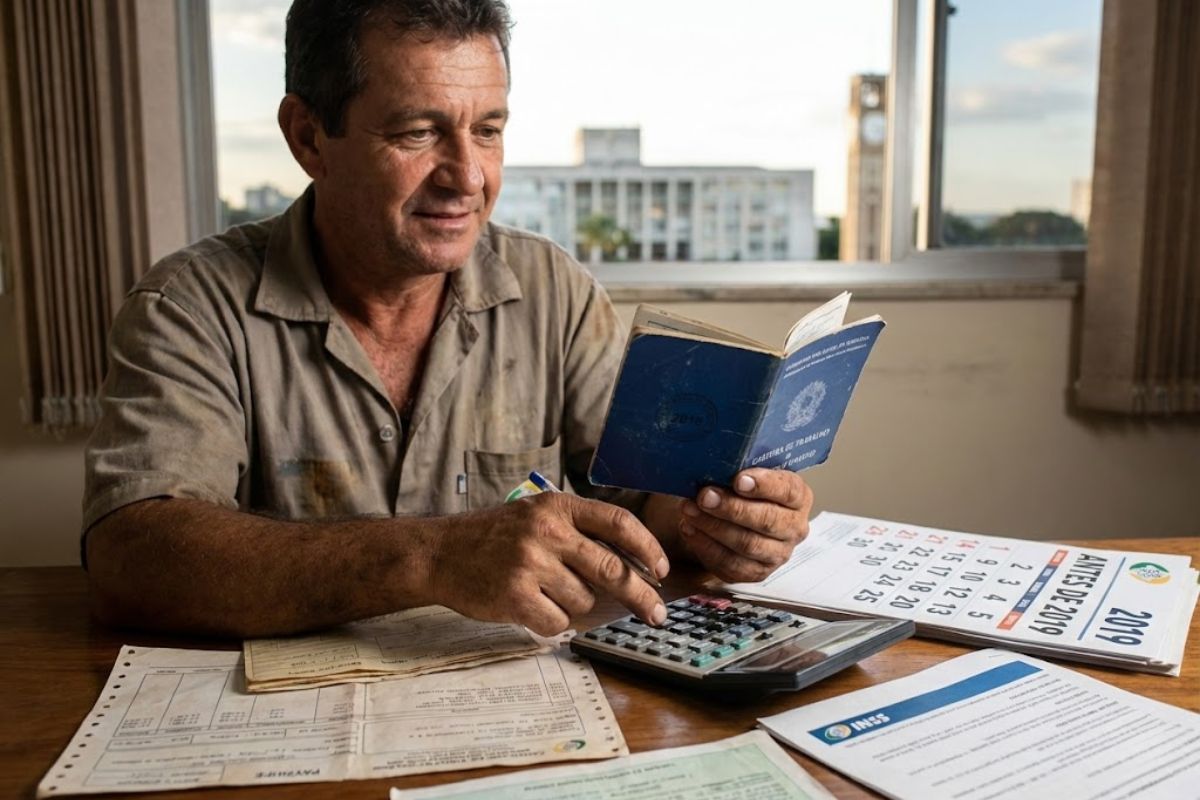

The insured needs to check the CNIS and the Meu INSS system to accurately verify how much contribution time they had until 11/13/2019. From there, they calculate:

- How much was missing to reach 30 years (woman) or 35 years (man)

- What will be the toll to fulfill, of 50% or 100%, on that missing period

Complementary Contribution Period

The insured continues to contribute until:

- Completing the minimum time of 30/35 years plus the 50% or 100% toll

- In the case of the 100% toll, also reaching the fixed minimum age of 57 years (woman) or 60 years (man)

In this interval, they can compare the toll with other transition rules, such as points or gradual minimum age, to identify which scenario tends to offer the most advantageous benefit.

Close to Retirement – Data Verification

With the requirements almost complete, the insured returns to Meu INSS and uses the “Simulate Retirement” feature to check if they already meet any transition rule or the general rule.

At the same time, they review the CNIS, correct links, salaries, or missing periods, and gather documents such as work cards, payment slips, and reports.

Request and Benefit Analysis

When they believe they have fulfilled the time and, if applicable, the minimum age required by the toll, the insured submits the retirement application through Meu INSS or Central 135.

The institute analyzes the history, checks compliance with the chosen rule, and may require additional documents.

Granting or Denial

If everything is regular, the benefit is granted with a defined start date and value.

In case of denial, the insured can present an administrative appeal within the INSS itself or seek legal advice to discuss the eligibility in court.

How to Choose the Most Advantageous Rule in Practice

With several modalities in effect, the choice between toll, points, or gradual minimum age is no longer automatic.

The simulation in Meu INSS is a central tool, as it considers age, gender, contribution time, and possible scenarios, including the transitions created after 11/13/2019.

However, the simulation is only reliable if the CNIS is correct, without missing links or underreported salaries.

Therefore, adjusting registration data has become part of retirement planning, especially for those who intend to use the 50% or 100% toll to escape the new minimum age of the INSS and preserve retirement conditions closer to the old rules.

In a scenario with so many possibilities, in your assessment, is it better to persist with the toll rule to maintain a lower retirement age or accept the new minimum age of the INSS in exchange for a potentially higher benefit calculation?

Qual a ideologia do desses políticos picaretas ? Se o o povo é o escravo do sistema que gira o motor da máquina pública para quê se aposentar mais cedo se expectativa de vida aumentou (dizem eles) mas na verdade temos que trabalhar mais para compensar as fraudes e roubos do INSS (que ninguém nunca vai preso) aí cada ano inventam uma regra nova para confundir a cabeça do povo !!! No futuro bem próximo só vai se aposentar quem for político ou quem tem um bom advogado !!! Esperta mesmo foi a Dilmis que antes do Impeachment deu uma canetada e se aposentou mais cedo e o honesto Lulis a chamou para ser Presidente dos BRICS para ganhar 100 mil por mês !!! Conclusão quem vota e apoia esses pilantras assina na testa a escrita “**** FELIZ” !!!

Para quem tem 16 anos de contribuição do é meu INSS

A segunda opção. Mas como a vida é incerta melhor a primeira. Kkk