Portuguese

Portuguese  English

English  Spanish

Spanish

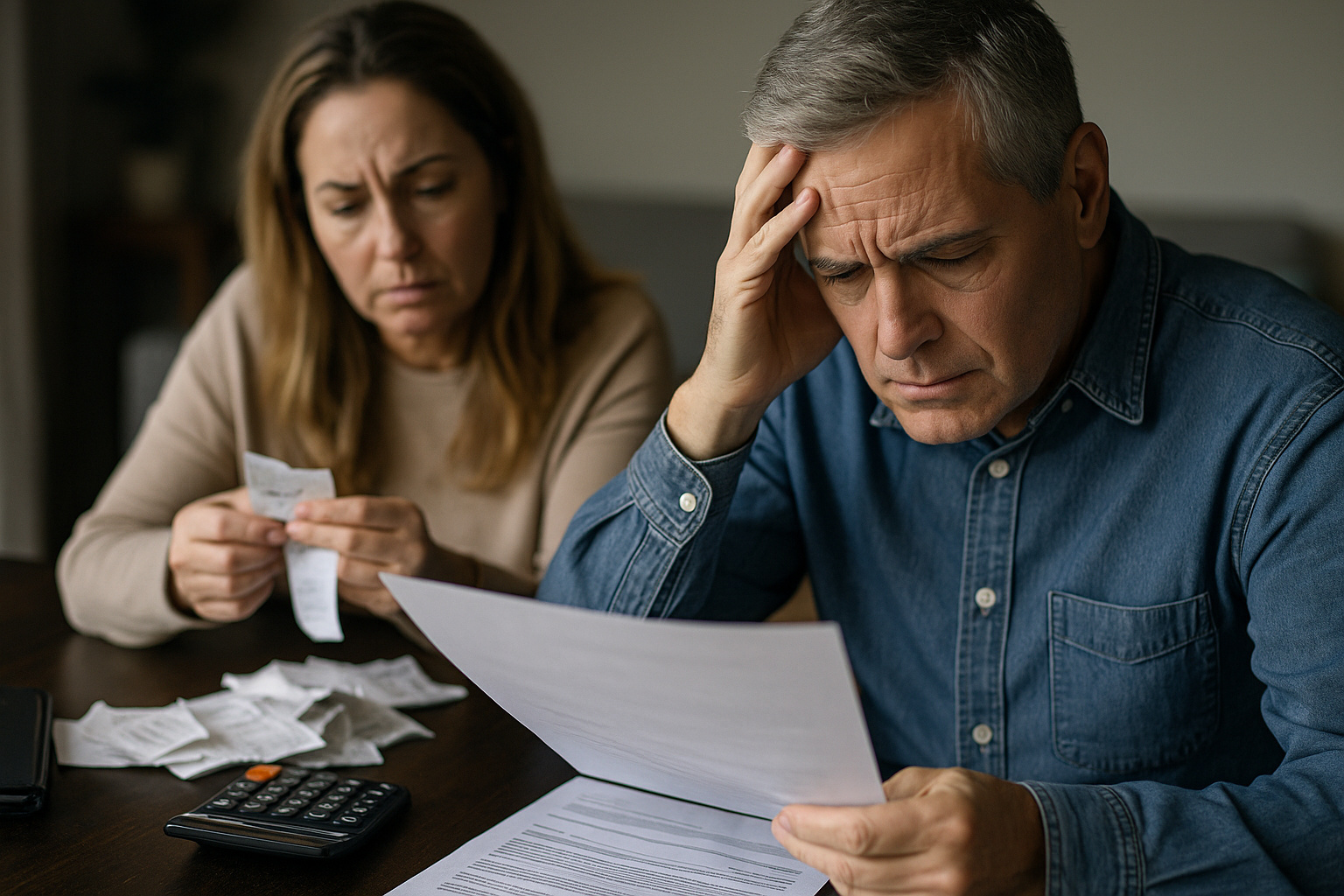

Understand Why Companies and Families Still Carry Debts Since 2020, How the Selic Rise Aggravated the Scenario, and What to Expect for 2026

Even with a record number of formal jobs and high average income, Brazil has 8.1 million negative CNPJs and 78.8 million people in default, according to Serasa Experian (Aug/2025).

This scenario is a result of debts inherited from the pandemic and a rise in interest rates from 2% (Aug/2020) to 15% (Jun/2025).

This increase made credit more expensive and debt repayment more difficult.

Therefore, the expectation is that defaults will persist in 2026, even with cuts to the Selic. The rate is expected to end the year at around 12%, which still impacts income and hiring.

Evolution of the Number of Defaults

According to the Serasa Default Map, the total number of defaults increased continuously in 2025, rising from 74.6 million in January to 78.8 million in August.

Each person in default owes, on average, R$ 6,267.69, distributed across four debts of about R$ 1,578.23 each.

The main sources of debts are banks and cards (27.27%), utilities (20.83%), and financial institutions (19.51%).

Pressure on Brazilian Families

The Inter Bank (2025) points out that household indebtedness, excluding mortgage financing, stands at 30.6% of income.

The average commitment reaches 26.3%. According to Flávio Ataliba Barreto (FGV/Ibre), after the pandemic, Brazil reached a new level of indebtedness.

This increase was driven by high interest rates, non-consigned loans, and constant use of revolving credit. Between 2017 and 2025, the number of indebted families rose from 58% to 79%, while defaults reached 30%.

Even with declines in unemployment, increases in average income, and the Desenrola Program (ended in 2024), the improvement was insufficient.

-

The institute that trained the greatest aerospace engineers in Brazil has just opened its first campus outside São Paulo after 75 years: ITA Ceará will have R$ 445 million, new courses in energy and systems, and classes are expected to start in 2027.

-

Luciano Hang, owner of Havan, goes to Juiz de Fora after the tragedy in February, brings R$ 1 million, hands out R$ 2,000 cards, and donates up to R$ 15,000 to victims in the region.

-

The Brazilian passport allows legal residence in dozens of countries without the need for a prior visa, and most Brazilians are unaware that they can apply for residency directly upon arriving in nations in South America, Africa, and even Europe.

-

Petrobras sends a message to Brazilian truck drivers after fuel collapse and reveals plan to have 100% domestic diesel.

Timeline and Official Sources

• 2017–2020: Fall of the Selic and stagnant real income after the impeachment (Source: FGV/Ibre).

• 2020–2022: Pandemic, inflation, and unemployment compress income (Sources: FGV/Ibre, Serasa).

• Aug/2020–Jun/2025: Selic rises from 2% to 15%, increasing the cost of credit (Source: Central Bank).

• 2025: 78.8 million in default (Source: Serasa).

• 2026: Selic projected at 12%, keeping credit tight (Sources: FGV/Ibre, Serasa Experian).

Companies Also Face Indebtedness

While families struggle with tight budgets, Brazilian companies face record defaults, worsening the economic scenario.

In August 2025, Serasa Experian registered 8.1 million negative CNPJs, a significant increase from 7.1 million in January and 6.9 million in August 2024.

Additionally, the country has 24.5 million active companies, and the average value of debts rose from R$ 21.6 million (2024) to R$ 24.6 million (2025).

Corporate debts are concentrated in services (31.9%) and banks, cards, and financial institutions (23.4%). According to Camila Abdelmalack (Serasa Experian), reduced margins, weak demand, and tight credit since 2022 limit investments and hiring.

Thus, defaults are expected to remain high in 2026, especially among micro and small enterprises, which account for 93% of active businesses.

How to Balance the Budget in 2026

Given the high interest rates, it is essential to replan the household budget consciously. Experts recommend renegotiating debts, avoiding revolving credit, buying in cash, and creating an emergency fund, which increases financial security.

According to Barreto (FGV/Ibre), financial education will be key to containing the increase in defaults and restoring balance.

Therefore, understanding where to cut expenses and how to adjust consumption is crucial to rebuilding the financial health of Brazilian families.

Seja o primeiro a reagir!