Portuguese

Portuguese  English

English  Spanish

Spanish

Debts Settled with Agreement Appear as “Loss” in the Central Bank’s SCR, Raising Alarm Among Banks and Blocking New Loans, Says Lawyer Antonio Galvão.

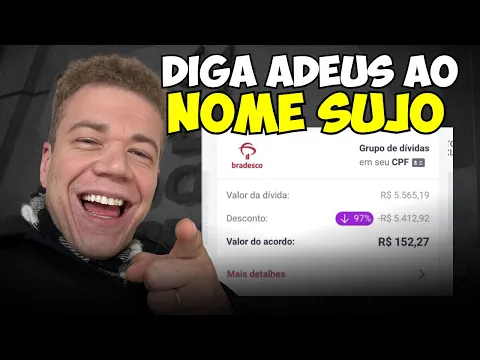

A debt of R$ 1,000 settled for R$ 200 may seem like a great relief, but the reality is that banks register the unpaid amount as a “loss” in the Central Bank’s Credit System (SCR). This means that, even with a clean record in agencies like SPC and Serasa, credit requests may be denied without a clear explanation.

According to lawyer Antonio Galvão, a consumer defense specialist, this mechanism affects thousands of Brazilians who agreed to negotiate overdue debts.

The SCR history does not disappear and banks continue to consult these records to block access to credit, even years after settlement.

-

BRICS is building its own payment system that could be operational by 2030, and experts say it could increase trade between the countries by up to 10% per year and add 3% to the GDP of each member of the bloc.

-

Government suspends over 3 million traffic fines in Brazil and drivers breathe a sigh of relief.

-

Iran has just approved toll charges for ships in the Strait of Hormuz and has completely prohibited the passage of vessels from the United States and Israel in the world’s most important maritime route for the global energy market.

-

Government cancels R$ 25 million “celebration” for Brasília’s anniversary and allocates funds to health.

What Is the SCR and How Banks Use It

The SCR is an official report from the Central Bank that compiles all credit operations associated with the consumer’s CPF.

Unlike services like SPC and Serasa, the SCR keeps records for up to 5 years, even when the debt has already been settled.

In practice, banks use the SCR as a central risk assessment criterion.

Any record of loss is interpreted as a sign of distrust, which is why many consumers with a high score and clean name continue to be denied loans and credit cards.

How the Loss Record Arises

When a customer accepts an agreement and pays only part of the debt, for example, R$ 200 of a R$ 1,000 debt, the bank registers the settlement but informs the Central Bank that it suffered a loss of R$ 800.

This amount appears in the SCR and becomes a negative mark for the financial system.

Even after settlement, banks consider that the customer did not fulfill the contract in full. This results in silent blocks that extend for years and reduce the chances of obtaining new credit.

How to Check If There Are Records Against Your CPF

The consumer can check their situation on Registrato, a tool from the Central Bank accessed with a Gov.br login.

The report shows which banks have had a relationship with the customer and identifies debts that are current, overdue, or classified as losses.

According to Antonio Galvão, it is essential to check if there are amounts recorded as losses and identify which institution made the record.

Only then can the consumer understand the real reason for denials in loans and take action to correct it.

How to Contest Loss Records with Banks

If the report points out records that block credit, the way is to file a complaint with the Central Bank’s Ombudsman.

The procedure is done online and should include proof of settlement and evidence that the name is clean in other credit services.

According to Galvão, many banks accept to correct the information administratively after the filing. When this does not happen, there are court decisions that compel the removal or alteration of the history in the SCR, giving consumers a new chance to access the financial market.

Is It Worth Accepting Discount Agreements?

This is the question for thousands of Brazilians. For those who do not intend to seek credit in the short term, the discount may be an immediate solution.

However, for those who need financing, the agreement may result in long-term blocks.

“The problem is not negotiating, but not knowing that this discount generates a loss and blocks credit in banks,” warns Galvão.

The ideal is always to evaluate the future impact before accepting proposals that seem advantageous in the present.

The situation of the R$ 1,000 debt settled for R$ 200 reveals how banks deal with information that affects financial life even after settlement.

The SCR works as an invisible history, used to deny credit to those who have faced difficulties.

And you? Do you think it’s fair that banks record “loss” even after payment?

Leave your opinion in the comments—we want to hear from those who have experienced this problem firsthand.

-

-

-

-

9 pessoas reagiram a isso.