Portuguese

Portuguese  English

English  Spanish

Spanish

The Changes in NFS-e and the Cross-Checking of Tax Data Have Made the Choice Between Working as an Individual or MEI a Strategic Decision That Directly Impacts Taxes, Profit, and Risk of Audit in the Coming Years

With the recent changes in the issuance of the Electronic Service Invoice (NFS-e) and the advancement of digital auditing, understanding whether it is more advantageous to work as a self-employed professional or as a Microentrepreneur (MEI) has ceased to be just a bureaucratic formality. Today, this choice directly influences the amount of taxes paid, the level of exposure to the tax authorities, and even how profit can be utilized in day-to-day professional life.

The information was disclosed in an article signed by André Rangel, who analyzes how the national standardization of NFS-e and the increasing data cross-checking by the Federal Revenue and municipalities are changing the game for service providers. In this new scenario, decisions made “automatically” can be costly as early as 2026.

Moreover, the method of formalization impacts not only the tax burden but also the ancillary obligations, financial control, and the fiscal security of the professional. Therefore, understanding the tax difference between self-employed and MEI has become essential for those looking to pay less tax within the law.

-

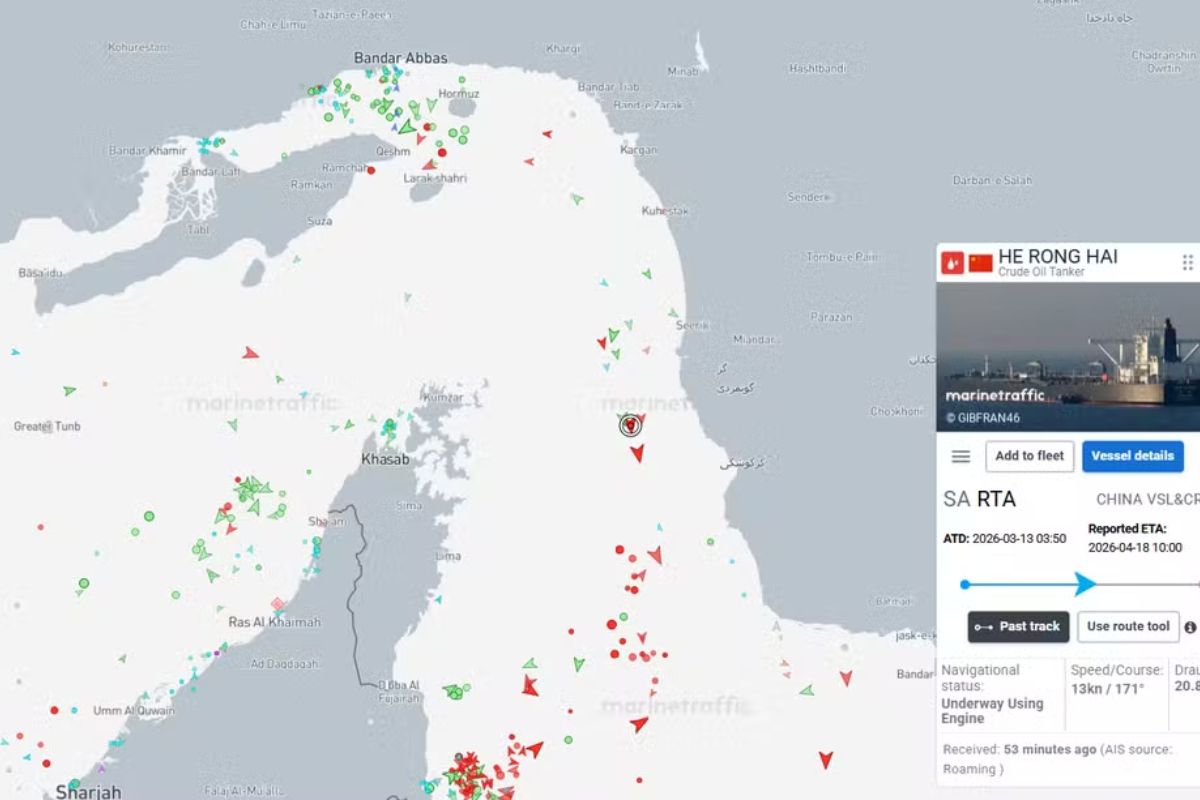

Two Chinese supertankers chartered by Asia’s largest refiner have just crossed the Strait of Hormuz and may be the first to leave the Persian Gulf since the ceasefire between the United States and Iran on a route that still has mines and uncertainties.

-

While Havan earns R$ 50 million per day throughout the year, Cacau Show managed six times more in just 24 hours, totaling half a billion reais in two days of Easter.

-

Weak dollar or strong real? The American currency plummets for the third day, approaching R$ 5 and surprising the market with global inflation and tensions in the Middle East that continue to create global uncertainty.

-

China’s investments in Brazil in factories, energy, oil, electric cars, and new industrial projects double to $4.2 billion, making the country the 3rd largest global destination for Chinese capital.

What Is the Tax Difference Between Self-Employed and MEI in Practice

The keyword in this debate is precisely the tax difference between self-employed and MEI. The self-employed professional who operates as an individual and issues receipts or NFS-e faces a fragmented tax structure. They must simultaneously deal with the monthly Income Tax via the carnê-leão, the social security contribution to INSS, and, in many cases, the collection of ISS directly to the municipality.

Each of these taxes follows its own rules, with distinct rates and, in the case of Income Tax, progressive percentages. This not only raises the tax burden but also increases the complexity of financial control and the risk of errors in monthly assessments.

In the case of MEI, the logic is completely different. Instead of multiple taxes calculated on revenue, the microentrepreneur pays a fixed monthly amount through the DAS. This document already encompasses the contribution to the INSS and the ISS or ICMS, depending on the activity performed. In practice, this simplifies management and significantly reduces the predictability of tax costs.

How Taxation of the Self-Employed Works in Detail

Those who work as self-employed and receive income from individuals are required to report the carnê-leão on a monthly basis. In this model, the Income Tax can reach the maximum rate of 27.5% on the taxable base, depending on the amount received in the month.

Additionally, there is the contribution to the INSS, which generally varies between 11% and 20%, depending on the classification, type of contribution, and whether or not the social security cap is applied. In many municipalities, the ISS still needs to be collected separately, following specific local rules.

This combination of taxes can create a significant burden, especially for those who do not maintain strict control over deductible expenses. Without organization, the professional risks paying more tax than necessary or falling into inconsistencies detected in data cross-checks between the Federal Revenue and city halls.

Why MEI Usually Pays Less Tax and Offers More Predictability

When analyzing the tax difference between self-employed and MEI, MEI often presents a clear advantage for those earning within the annual limit, currently around R$ 81,000, unless there are legislative changes. Within this ceiling, the value of the DAS is fixed and predictable, regardless of monthly revenue.

In the MEI regime, the main taxation occurs at the corporate level. When transferring funds to their personal account, part of the revenue can be classified as tax-exempt profit, as long as the rules of the Federal Revenue are followed. This reduces or even eliminates the incidence of personal Income Tax, something impossible for the self-employed who pays carnê-leão month after month.

This model makes MEI especially attractive for service providers who need to issue invoices frequently and wish to simplify tax payments without sacrificing formality.

The Impact of Monthly Accounting and NFS-e on Fiscal Control

Many professionals still underestimate the importance of monthly accounting, especially in MEI. Without proper bookkeeping, the Federal Revenue applies standardized percentages to estimate exempt profit: 8%, 16%, or 32% of revenue, depending on the activity performed.

The amount that exceeds these percentages may be taxed under the personal Income Tax. On the other hand, with accounting oversight, it is possible to prove the actual profit through balance sheets and reports, allowing for profit distribution with total exemption from Income Tax, even above the presumed percentages.

With the national standardization of NFS-e, data cross-checking became more efficient. Both MEIs and self-employed professionals need to be extra cautious to avoid issues such as duplicate ISS, registration errors, and inconsistencies between issued invoices and tax declarations.

When to Choose MEI or Continue as Self-Employed

In practice, MEI tends to be more advantageous for those engaged in permitted activities, earning within the legal limit, and looking to simplify tax obligations. The self-employed model may make sense in very specific situations, such as sporadic income or activities that do not qualify for MEI.

Deciding on a “feeling” basis, however, has become a risk. With auditing becoming increasingly digital, each month without planning can represent more money paid to the tax authorities and less profit in one’s pocket. Reassessing the classification, monitoring revenue, and seeking specialized accounting support has ceased to be optional and has become a financial survival strategy.

-

-

-

-

-

-

29 pessoas reagiram a isso.