Portuguese

Portuguese  English

English  Spanish

Spanish

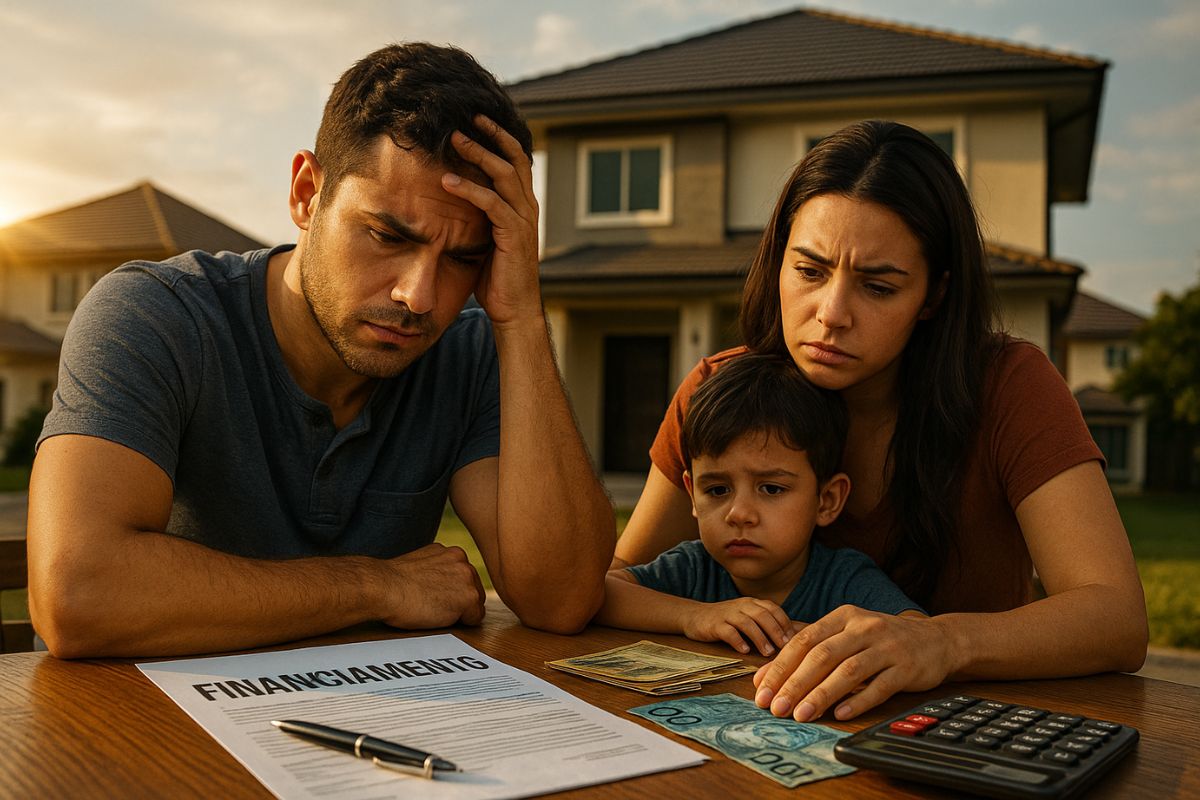

Every 1% Increase in Interest Rates Requires 8% to 10% More Income, Restricting Middle-Class Access to Home Financing, Warns Ricardo Floriano.

The home financing in Brazil is increasingly distant from the reality of the middle class. According to real estate credit specialist Ricardo Floriano, founder of CSM, every additional 1% in interest rates requires 8% to 10% more income for credit approval. This silent mechanism has expelled thousands of families from the system, creating an almost insurmountable barrier for those seeking to leave rental housing.

Although 2024 registered a record R$ 312 billion financed, with nearly 1.2 million properties, real estate credit remains stagnant at around 10% of GDP, far below countries like the United States (50% to 60%), Canada (55%), and the Netherlands (90%).

According to Floriano, the combination of high interest rates and limited funding keeps the sector stalled and weakens middle-class access to home ownership.

-

The largest food company on the planet, JBS, has just opened a 4,000 square meter laboratory in Florianópolis to develop customized proteins that modulate muscle mass gain, immune response, and metabolic performance.

-

After nearly 30 bids and competition among industry giants, a Spanish company purchases one of the largest airports in Brazil for almost R$ 3 billion and takes over the management of Galeão in a concession that will last until 2039.

-

The Federal Revenue Service now automatically cross-references everything you declare with data from banks, credit cards, brokerage firms, and insurance companies, and any discrepancy between your income and your expenses triggers an alert in seconds.

-

Amid global tensions, Brazil blocks the United States’ proposal at the WTO and paves the way for a trade crisis and possible retaliations.

Why Do Interest Rates Weigh So Heavily on Home Financing

In Brazil, current financing rates range from 11.29% to almost 14% per year, according to banks and modalities.

In comparison, European countries operate between 3% and 4%, the USA around 6%, and Chile between 6% and 7%. This difference puts Brazilian consumers at a disadvantage.

In practice, a property worth R$ 300,000 financed is heavily impacted: for each 1 percentage point increase in the rate, the family needs to prove about R$ 700 additional income.

For those already at the budget limit, this increase makes approval unfeasible. According to Floriano, this automatic effect is what has been silently expelling the middle class from home financing.

Stagnant Structure Since 1997

The current system was born with the fiduciary alienation law of 1997, which replaced mortgages and provided more security to banks for reclaiming properties in the event of default.

This change increased real estate credit from 2% to 10% of GDP, but nearly three decades later, the sector has stagnated at this level.

According to Ricardo Floriano, the architecture of the system has not evolved: real estate credit remains expensive, concentrated, and bureaucratic, without gaining sufficient scale to democratize access.

Meanwhile, middle-class families remain in a limbo without access to subsidies from Minha Casa, Minha Vida and without conditions to take on high rates in the traditional market.

The Role of Funding and Savings

Financing depends on three pillars: savings, FGTS, and the capital market. Savings is the main source, but in 2024 it recorded negative net inflow, and in the first months of 2025 had a net outflow of R$ 34.6 billion.

When this happens, banks turn to the capital market, where the cost is higher and passed on to the borrower.

The FGTS, in turn, subsidizes rates between 4% and 10.5% per year for Minha Casa, Minha Vida, but is restricted to low-income brackets.

The capital market accounts for about 40% of funding, but it is more expensive and volatile, increasing pressure on interest rates.

For Floriano, without expanding cheap sourcing, home financing will remain inaccessible to the middle class.

Extra Costs and Bureaucracy Increase the Bill

In addition to interest rates, consumers face notary fees and high taxes. In São Paulo, for example, a property worth R$ 400,000 generates about R$ 20.3 thousand in notary and ITBI expenses — more than 5% of the property’s value.

The average time for contract issuance ranges from 40 to 60 days, while in developed countries the process takes at most 20 days.

These barriers increase the total cost of credit, scare off buyers, and keep the real estate market less dynamic.

For Ricardo Floriano, the combination of high interest, expensive funding, and heavy bureaucracy creates a system that naturally expels the middle class.

Economic and Social Impact

The rising cost of home financing freezes the entire chain: families remain in rental housing, brokers stop selling, construction companies delay projects, and industries linked to the sector reduce production. In 2025, the forecast is for a 15% to 20% drop in real estate credit approvals, signaling a slowdown in the entire sector.

Floriano emphasizes that this is not just a government problem, but a structural flaw in the credit model, which has only received temporary solutions for years.

Without deep reforms that reduce the cost of money and increase predictability, the country will remain far from providing the middle class with real conditions to finance home ownership.

Ricardo Floriano’s analysis shows that every additional 1% in interest expels thousands of families from home financing, as it requires 8% to 10% more income for approval. This mechanism quietly distances the middle class, keeping real estate credit restricted and unequal.

And you? Do you believe that Brazil needs a structural reform in real estate credit to ensure access to home financing, or are targeted solutions already sufficient?

Leave your opinion in the comments — we want to hear experiences from those living this reality.

-

-

5 pessoas reagiram a isso.