Portuguese

Portuguese  Spanish

Spanish

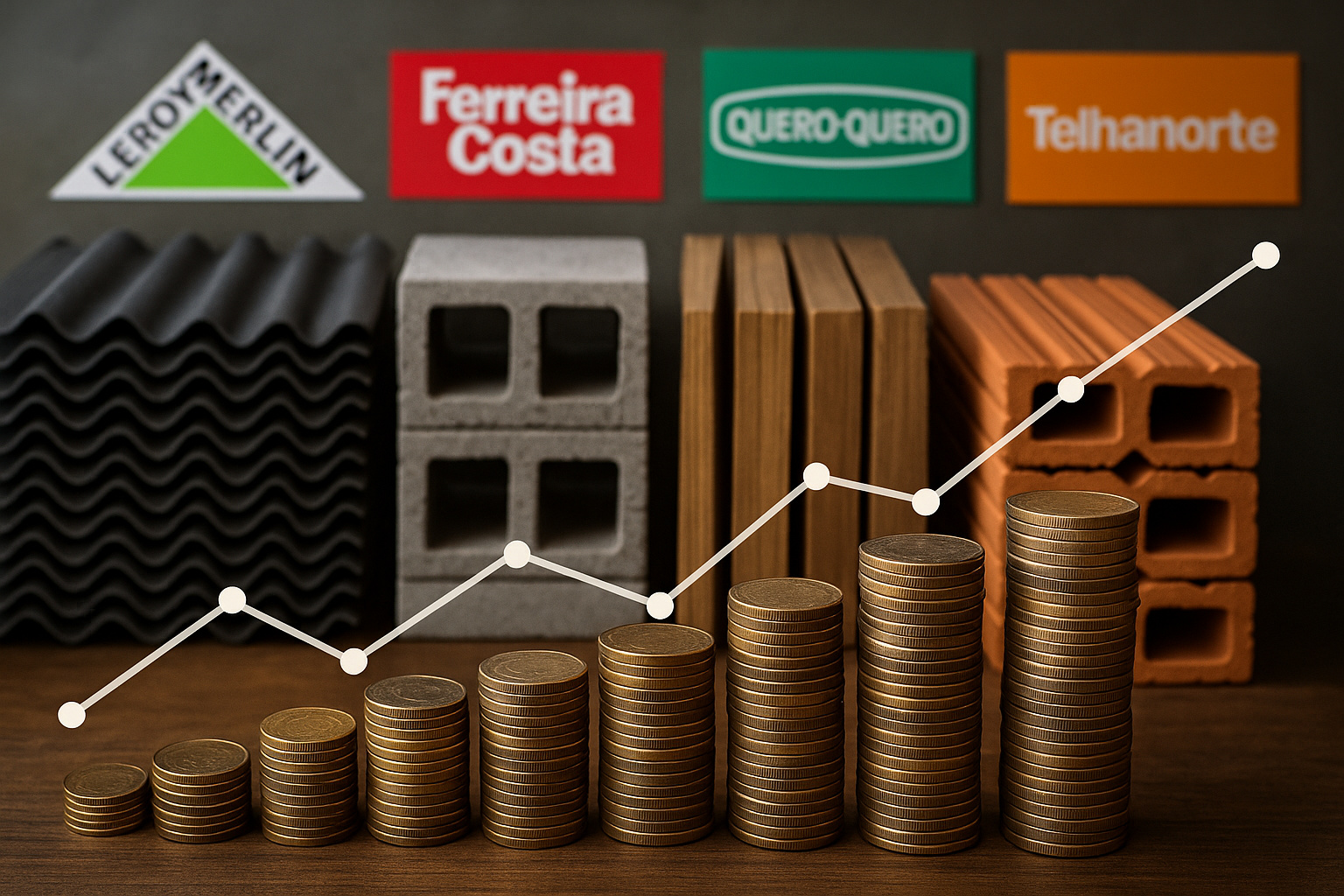

Over R$ 25 billion in sales registered in 2024 reveal the weight of construction material networks in Brazilian retail, highlighting home centers and wholesale.

A survey by the IRT Institute, published in 2024, showed that the construction material sector generated R$ 25.3 billion, with a modest growth of 6.2% compared to 2023.

Although the segment represents only 2% of national retail, it stands out for its operation model in large surface stores and regional concentration.

According to the data, 13 companies in the sector ranked among the 300 largest retailers in 2024, confirming its relevance.

Nonetheless, expansion remains moderate, impacted by macroeconomic conditions and high interest rates.

Economic Impacts and Post-Pandemic Scenario

During the pandemic of 2020 and 2021, the sector grew rapidly, driven by homes adapting to home office and domestic leisure. However, starting in 2022, this trend lost strength, and the pace slowed. In 2024, consolidated growth was halted by high interest rates, which made credit more expensive and reduced the public’s interest in investing in construction and renovations.

-

The urgent need to implement a severe cut in public spending and a massive increase in taxes, in addition to drastically compromising the quality of basic services and the purchasing power of the population, could result in social unrest in the country, with the population leading protests, strikes, and frequent disturbances.

-

FIRJAN’s mega plan of R$ 526.3 billion for Rio de Janeiro aims to revive Brazil’s largest industry, with two-thirds of the investments going to oil and gas.

-

China signals an increase in beef imports, Brazil has already consumed 70% of the 1.106 million ton quota and seeks to renegotiate the tariff that jumps from 12% to 55%, while demand from the US also skyrockets.

-

Food inflation rose 302% in 20 years in Brazil, but the supermarket changed: purchasing power yielded 87% more mortadella and 31% less fruit, and ultra-processed foods took over the cart.

This scenario confirms that, although the sector remains relevant, demand depends on financing conditions and family consumption behavior.

Business Strategies and Highlighted Formats

Additionally, home centers have consolidated as the dominant model, offering a wide variety of products in large megastores. However, wholesale also grew, mainly targeting the professional audience.

This is the case of Obramax, a chain of Grupo Adeo (which controls Leroy Merlin). In 2024, the company operated nine stores between São Paulo and Rio de Janeiro, focused on volume purchases. This format proved to be strategic for serving builders and contractors seeking more competitive prices.

At the same time, regionalization remains a central characteristic of the sector.

Nine of the main networks operate with a strong presence in local markets, limiting national expansion but ensuring proximity to the consumer.

Ranking of the Largest Companies in 2024

According to the IRTT survey, the ranking of leaders in 2024 was as follows:

- Leroy Merlin: maintained the leadership, with R$ 8.97 billion in sales and 54 stores in Brazil. Its strength lies in the megastore model and high average revenue per unit.

- Ferreira Costa: secured the second position, with R$ 2.4 billion in sales and only nine stores, but with efficiency per unit above the sector average.

- Quero-Quero: finished in third place, with R$ 2.17 billion in sales and 573 stores, located mainly in small and medium-sized cities.

- Telhanorte (Saint-Gobain Group): in fourth, achieved R$ 1.88 billion in sales in 2024, with 68 stores, investing in digitalization, logistics, and customized solutions.

- Sodimac Brasil (Falabella Group): closed the top 5 with R$ 1.75 billion in sales and 52 stores, consolidating its position in the Brazilian market.

Financial Challenges and Consumer Behavior

According to experts, high interest rates were one of the main obstacles in 2024. Expensive credit limited financing and reduced appetite for consumption. This impact was especially felt in the renovation market, which lost strength after the pandemic years.

Still, the main networks invested in logistics, technology, and expansion. The pursuit of efficiency and competitiveness became a priority, and according to the IRTT, this movement is expected to mark the sector in the coming years.

What Does the Future Hold for the Sector?

Based on the performance in 2024, analysts believe that the construction material sector will remain relevant. However, it will face challenges to sustain continuous growth. The sustainability of operations will depend on innovative strategies, digitalization, and adaptation to regionalized consumption.

Moreover, the competition between home centers and wholesalers is likely to intensify.

Meanwhile, regional networks should expand their presence in strategic markets.

What do you think: should the construction material sector in Brazil invest in national expansion with large networks or in regional models and wholesalers?

Be the first to react!