Portuguese

Portuguese  English

English  Spanish

Spanish

The Law In Effect In Brazil Allows For The Renegotiation Of All Debts At Once, Requires Banks To Participate In Hearings, And Ensures That The Debtor Maintains A Minimum Amount For Living With Dignity, Establishing A New Framework In The Relations Between Consumers And Financial Institutions.

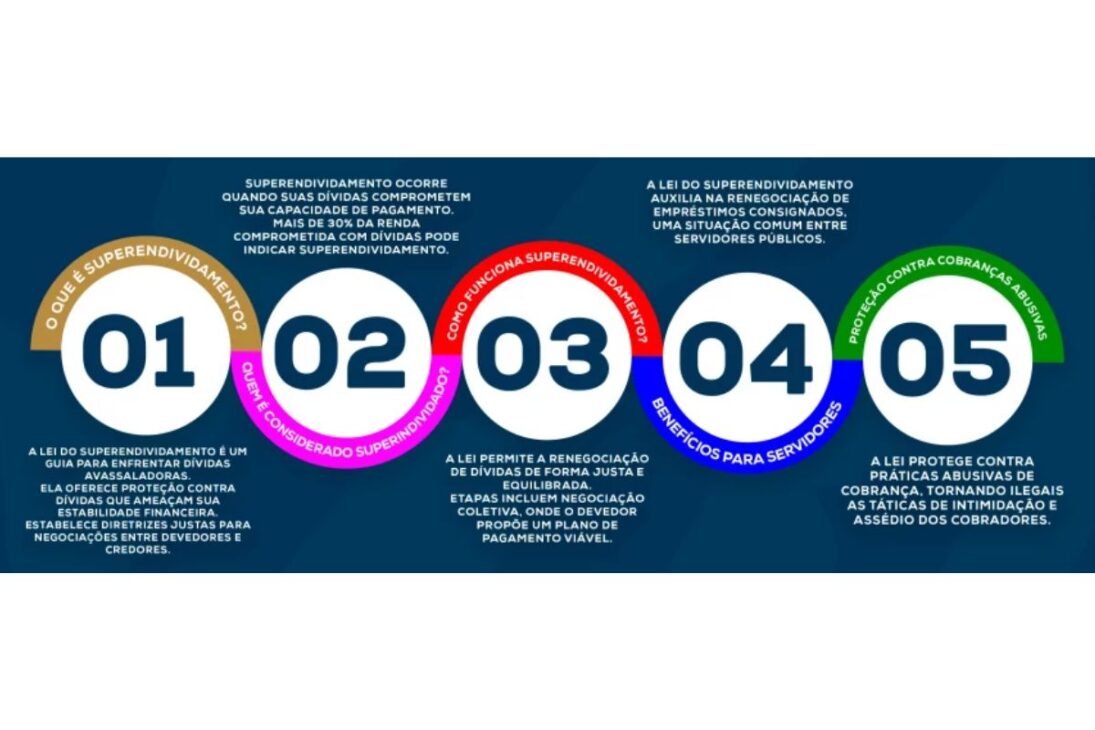

A law in effect in Brazil is changing the way over-indebted consumers deal with their debts. The so-called Superindebtedness Law (Law 14.181/2021) amends the Consumer Protection Code and creates mechanisms that allow for the renegotiation of all debts at once, similar to corporate reorganization.

The big news is the requirement for creditors to be present at conciliation hearings and the guarantee of what is called the “existential minimum”, an amount that must remain after the renegotiation to cover basic expenses such as housing, food, and health. The goal is to allow the debtor to regain their financial stability without losing the essentials for living with dignity.

How The Renegotiation Process Works

The consumer can seek the Judiciary, the Public Defender’s Office, or a credit protection agency to present a payment plan.

-

The Senate approves a bill that criminalizes misogyny, hatred, or aversion towards women, and includes the crime in the Racism Law with a penalty of up to 5 years.

-

Chamber Approves Bill That Allows Pepper Spray for Women Over 16 and Imposes Strict Rules for Purchase, Possession, and Use as Self-Defense

-

Chamber Approves Law to Combat Leucaena, Fast-Growing Plant That Dominates Land and Threatens Native Species in Various Regions of the Country

-

Asset Division: Know What Cannot Be Divided in Case of Divorce

In this plan, all consumer debts are included, such as loans, credit cards, and basic bills.

The judge then summons all creditors to a conciliation hearing. Banks and financial institutions are required to attend.

If they fail to show up without justification, they may be fined, and the judge has the power to approve the plan proposed by the debtor even without the presence of the institutions.

Payments can extend to five years, with a grace period of up to six months, and the amounts of the installments must respect the income and the existential minimum.

This ensures that the renegotiation is sustainable and does not push the debtor into a new cycle of default.

What The Existential Minimum Means

The existential minimum is the amount that must remain untouched in the debtor’s income, even after paying the debts.

According to a presidential decree from 2023, this limit is R$ 600, but there are discussions about updating it to more realistic amounts, considering inflation and the cost of living.

In practice, this rule prevents the citizen from being forced to choose between paying the bank or eating.

The principle of human dignity is the central axis of the law, which seeks to balance the relationships between consumers and creditors in a context of economic vulnerability.

Who Can Benefit From The Law In Effect

The law in effect serves well-meaning individuals, that is, those who incurred debts with the intention of paying, but lost financial control.

The focus is on protecting those affected by crises, unemployment, high interest rates, or increasing debts due to revolving credit and payroll loans.

Consumer debts such as electricity, water, and phone bills, personal loans, and credit cards can be included.

However, real estate financing, rural credit, alimony, and tax debts are excluded, as they have their own legislation.

Data That Shows The Severity Of Over-Indebtedness

Brazil currently has over 73 million indebted individuals, according to a 2024 survey by Serasa.

The National Confederation of Trade indicates that 30.2% of Brazilian families are in default, the highest rate since 2023.

Since the law was enacted, the number of legal proceedings increased by 8,530% between 2021 and 2024, jumping from 409 to 35,301 actions.

The financial sector is the main target of renegotiations, and courts have already determined that banks comply with payment plans imposed by the Justice system.

These figures show that the law not only provides a legal exit but represents a social response to chronic indebtedness that impacts the economy and well-being of families.

A New Balance Between Banks And Consumers

With the law in effect, the power of negotiation is no longer exclusive to financial institutions.

Now, banks must actively participate in the process, present counterproposals, and respect the debtor’s survival limit.

This change represents a step forward in consumer protection and helps prevent the financial collapse of entire families.

Experts point out that the law encourages more responsible credit practices, as the risk of default now also falls on those who grant loans in a disordered manner.

Challenges And Next Steps

Despite the advances, the practical application of the law still faces challenges.

Many consumers are unaware of their rights, and there are discrepancies regarding the calculation of the existential minimum.

Furthermore, courts in different states have varying interpretations regarding the scope of included debts.

Still, the consensus is that the law has brought hope to millions of Brazilians.

The combination of judicial negotiation, guaranteed minimum income, and mandatory participation of banks creates a more humane and balanced model of financial recovery.

Que atire a primeira pedra quem consegue viver com 600,00/mês.

Isso é um absurdo. Ao me aposentar passei a receber um valor do qual tenho que pagar 2.000 de plano de saúde para mim e minha esposa, os dois 60+, além de 2.000 de financiamento imobiliário que entram na negociação.

Comentário em INGLÊS?

COMO POSSO ENTENDER?

Com o Google Tradutor: “Com o Google Tradutor: “Devo dizer que este artigo é extremamente bem escrito, perspicaz e repleto de conhecimento valioso que demonstra a profunda expertise do autor no assunto. Agradeço profundamente o tempo e o esforço investidos na criação de um conteúdo de alta qualidade, pois ele não é apenas útil, mas também inspirador para leitores como eu, que estão sempre em busca de recursos confiáveis online. Continue com o bom trabalho e escreva mais. Sou seu seguidor.” Usuário marketing service éQé… Kkkk Sobre a matéria, devo pesquisar mais, porém é nítido planos desde lá como os publicados pelo Serasa, Desenrola Brasil e outros, embora não englobam em tudo o que a maioria diz o fazer da lei.”

Usuário marketing service éQé. Kkkk

Sobre a matéria, devo pesquisar mais, mas serviços como Serasa, Desenrola Brasil e outros tentam, embora não fazem o que diz na matéria o fazer da lei.

I must say this article is extremely well written, insightful, and packed with valuable knowledge that shows the author’s deep expertise on the subject, and I truly appreciate the time and effort that has gone into creating such high-quality content because it is not only helpful but also inspiring for readers like me who are always looking for trustworthy resources online. Keep up the good work and write more. i am a follower.