Portuguese

Portuguese  English

English  Spanish

Spanish

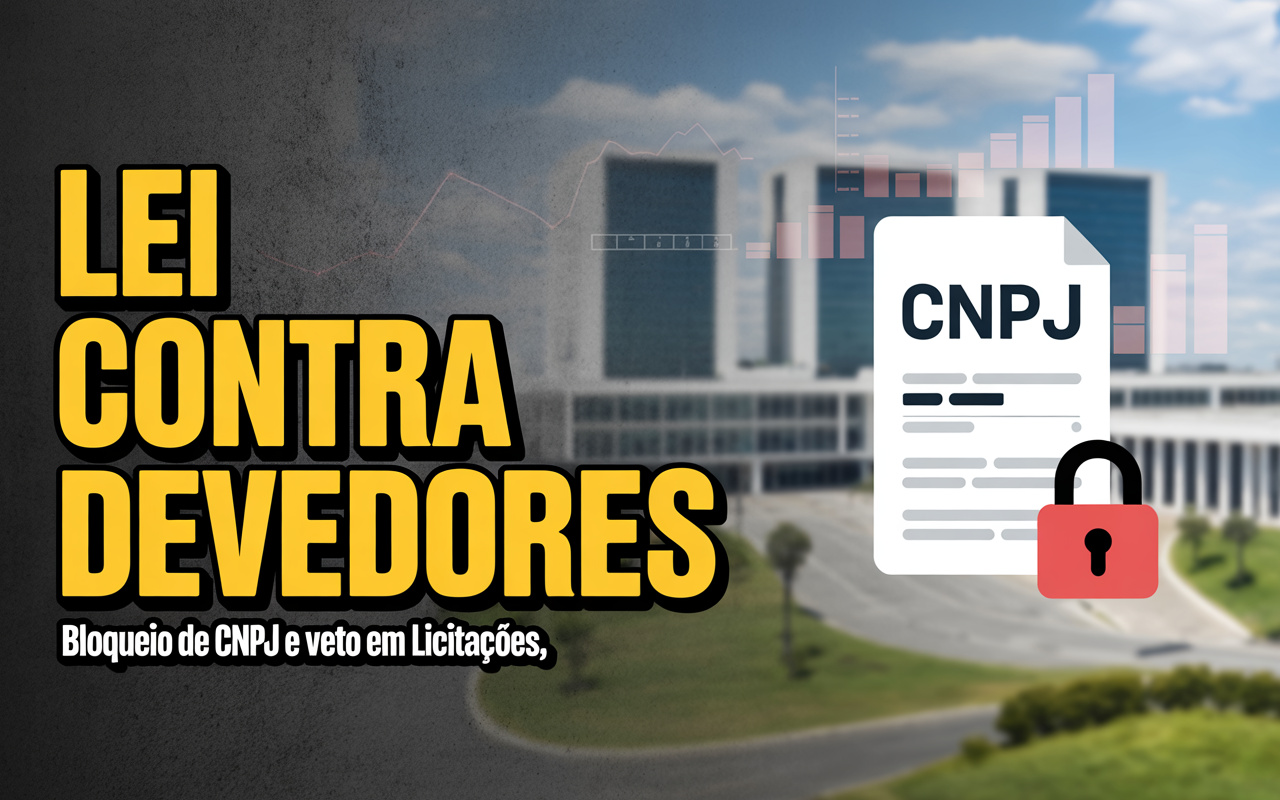

Enacted on January 9, 2026, Complementary Law No. 225 establishes strict rules against “habitual debtors,” including CNPJ blocking, prohibition in bidding processes, and fiscal restrictions for those who use default as a business strategy.

On January 9, 2026, following its publication in the Official Federal Gazette, Brazil began operating under the Complementary Law No. 225/2026, signed by President Luiz Inácio Lula da Silva the previous day, which focuses on a specific type of taxpayer: the “habitual debtor”, one who does not fail to pay due to temporary incapacity, but instead uses default as a business model, gaining a competitive advantage over companies that regularly pay taxes.

According to a report by R7 published on January 9, 2026, Complementary Law 225 is part of a larger package called the Taxpayer Defense Code, and creates a fundamental distinction: it is not any company in debt that will be punished, but only those that show recidivism, accounting manipulation, and use of default as a commercial advantage.

Objective Criteria Define Who May Be Classified

To avoid criminalizing the ordinary taxpayer, who may occasionally delay a tax payment or face a cash crisis, the law requires strict financial criteria. According to the official publication, “habitual debtor” will be considered those who:

-

The noise law will no longer be in effect at 10 PM starting in June with a new rule valid during the 2026 World Cup.

-

The Chamber opens a debate on driver’s licenses at 16 years old as part of a reform that includes around 270 proposals to change the Brazilian Traffic Code and may redesign rules for licensing, enforcement, and circulation in the country.

-

The new Civil Code could revolutionize marriages in Brazil with “express divorce” and changes that could exclude spouses from inheritance.

-

Banco do Brasil sues famous influencer for million-dollar debt and intensifies debate on delinquency, risks of seizure, and direct impact on Gkay’s credibility.

– Maintain unjustified tax liabilities of R$ 15 million or more, and

– These liabilities represent more than 100% of the taxpayer’s known assets.

This provision prevents small business owners or struggling merchants from being classified as such and targets companies structured to evade taxes, which operate in a predatory manner against competitors and public revenue.

What Changes in Practice for Those Classified as Habitual Debtors

The law creates a set of unprecedented administrative and economic sanctions in the Brazilian tax system, including:

Blocking or Inaptitude of CNPJ

The company may be declared inapt, which in practice halts its operations, prevents the issuance of invoices, and destroys its capacity for immediate competition.

Prohibition from Participating in Public Bidding

Habitual debtors become prohibited from competing for contracts with the Union, States, and Municipalities, directly affecting sectors that depend on public purchases.

Loss of Tax Benefits and Government Incentives

Programs for exemptions, tax relief, and incentives granted by Development Companies and Finance Secretariats may be canceled, reducing profit margins.

Restriction on the Use of Judicial Recovery

The law creates specific barriers to prevent habitual debtors from using judicial recovery to shield tax debts, separating real crises from strategies of artificial shielding.

These provisions bring Brazil closer to the model already adopted in OECD countries, where systematic non-compliance with taxes is treated as market distortion, not merely as default.

Why the Government and Tax Authorities Pushed for the Law

According to the Federal Senate, the text — originated from PLP 125/2022 — was defended as a protection for regular taxpayers, and not as a tax burden increase.

The motivation is economic: companies that fail to pay taxes finance artificially low prices, pressuring the margins of competitors that collect taxes and also reduce municipal, state, and federal revenue.

In Congress, centrist and leftist lawmakers argued that the measure prevents a growing phenomenon: companies with billion-dollar debts that open and close CNPJs in a cascade, maintaining assets and competitiveness while the tax authorities and competitors are left at a loss.

Market Reaction and the Debate on Legal Uncertainty

Unlike other tax issues, the law did not generate widespread panic in the productive sector, because the text excludes:

– companies with debts disputed in court,

– involuntary debtors,

– and taxpayers in very short-term recovery.

However, business associations are calling for State and Municipal Regulations to be standardized, to avoid different interpretations among tax authorities, something that could lead to legal disputes in the future.

The legal market predicts that the issue will be heavily litigated, especially in cases where the Federal Revenue Service or Finance Secretariats attempt to classify companies at the boundary of asset and debt criteria.

The Symbolic Impact: Default as a Strategy Becomes Visible

Economists and prosecutors from the National Treasury highlight that the law is important not for the number of affected companies, but for its regulatory effect: for the first time, the State defines a concrete benchmark that separates cyclical default from strategic evasion.

For the productive sector, the message is clear: the fiscal game is no longer just accounting, and becomes competitive and reputational.

The enactment of Complementary Law No. 225/2026 does not create a police state, but establishes clear boundaries between:

- the entrepreneur who owes because they broke,

- the entrepreneur who owes because they resort, and

the entrepreneur who owes because they don’t want to pay and use this to gain market.

This is why the issue has gained traction: it is not about taxes, it is about competition, fiscal justice, and improving the business environment.

-

-

2 pessoas reagiram a isso.