Portuguese

Portuguese  English

English  Spanish

Spanish

With the Decision Promised by the Ministry of Cities, Minha Casa, Minha Vida Should Expand Tier 1 to R$ 3,200 and Tier 2 to About R$ 5,000, in Addition to Reinforcing Goals of 3 Million Housing Units and Adjusting Property Ceilings with Support from FGTS Already in This Current Mandate.

Minha Casa, Minha Vida has returned to the government’s radar with the proposal to increase income tier limits and thus open the program to more Brazilians. The indication is that Tier 1, currently limited to R$ 2,850, will be expanded for families with income of up to R$ 3,200, while Tier 2 is expected to rise from R$ 4,700 to around R$ 5,000.

The decision is expected to be made by the Ministry of Cities by the end of the week and, the following month, will go to the Curator Council of FGTS, which evaluates the approval of the new rules. In the background, the government seeks to boost the program’s reach and bring the target of 3 million contracted housing units closer by the end of the mandate in December.

What Changes in the Tiers and Why This Unlocks More People

The mechanism is simple to understand: the program is organized by tiers of gross monthly family income, and each tier grants access to different financing conditions. When the ceiling of the tier rises, families that were previously “on the edge” become eligible for the program, which tends to increase the potential beneficiary base without disrupting the entire housing credit machinery.

-

The Federal Revenue Service now automatically cross-references everything you declare with data from banks, credit cards, brokerage firms, and insurance companies, and any discrepancy between your income and your expenses triggers an alert in seconds.

-

Amid global tensions, Brazil blocks the United States’ proposal at the WTO and paves the way for a trade crisis and possible retaliations.

-

Shopee opens the largest logistics warehouse in Brazil in Guarulhos: 220,000 m² on Dutra, contract signed before construction, pays R$ 45/m² and accelerates deliveries at scale, putting pressure on Mercado Livre and Amazon.

-

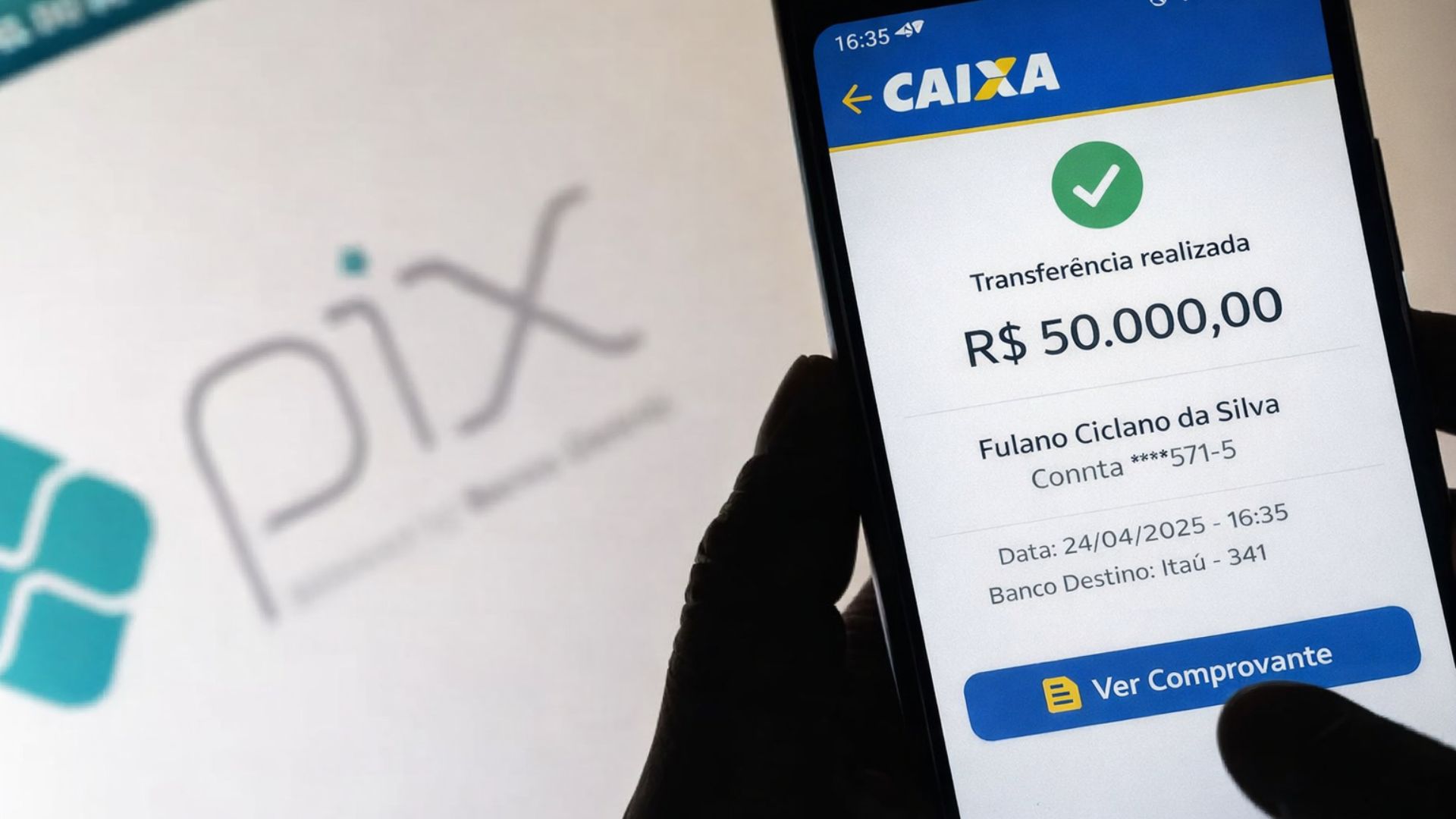

After mistakenly transferring R$ 50,000 via Pix, a man will receive the amount back along with R$ 10,000 for moral damages from the recipient.

In practice, the proposal specifically targets the most common transitions: those who barely exceed the current limits and end up pushed into less advantageous lines.

According to the portal oglobo, by raising Tier 1 to up to R$ 3,200 and Tier 2 to about R$ 5,000, Minha Casa, Minha Vida expands the entry door for families that have income but still face difficulty in assuming high installments or gathering a larger down payment.

How Each Tier Works Today and What Benefits It Delivers

Today, Minha Casa, Minha Vida has three main income tiers. In Tier 1, the ceiling for gross monthly family income is R$ 2,850, and it’s in this layer that the largest public support weighs in: the subsidy can reach 95% of the property’s value, making the family pay a significantly smaller portion of the final price.

In Tier 2, income ranges between R$ 2,850.01 and R$ 4,700. Here, the program maintains the incentive logic but with a different design: there is a subsidy of up to R$ 55,000 and lower interest rates, attempting to balance cost and access.

Meanwhile, Tier 3 ranges from R$ 4,700.01 to R$ 8,600: there is no subsidy, but there is still the advantage of interest rates below the market standard, which can reduce the total amount paid over the financing period.

Why the Program Affected the Middle Class and the “Tier 4 Effect”

The government had already made a recent move to include an audience that usually gets stuck between two worlds: it does not fit into the stronger social design but also does not find cheap credit easily.

A new income tier was created, raising the program’s reach, which previously served income up to R$ 8,600, to accommodate those with income of up to R$ 12,000, focusing on housing financing for the middle class.

This change addresses a specific problem: the scarcity of savings resources, traditionally used as a source for financing properties by this audience.

When this source becomes more restricted, credit tends to get more expensive, more selective, or simply harder to access.

By including the middle class in Minha Casa, Minha Vida’s design, the government aims to offer a financing path with more predictable rules, albeit with different conditions from the tiers that receive subsidies.

Subsidy, Low Interest Rates, and What Truly Matters in the Budget

In real life, what decides the game is the monthly budget. Minha Casa, Minha Vida combines two instruments to make the installment “fit”: direct subsidies (when available) and interest rates below the standard. The lower the income and the greater the vulnerability, the more likely the subsidy will be substantial, especially in Tier 1.

Additionally, the program offers regional and operational advantages: low-income families residing in the North and Northeast regions have access to lower interest rates and a discount granted by FGTS to help the installment fit the family budget.

The mentioned interest rates range from 4% per year to 10.5% per year, and the discount can reach up to R$ 55,000 per family, according to the rules described for the program.

The Ceiling on Property Value and Why It Became a Central Piece

It is pointless to expand the income tiers if the property ceiling is left behind. That is why recent adjustments also targeted the maximum allowable property value in certain tiers and regions.

In December, the Curator Council of FGTS approved new adjustments to the property value ceiling of Minha Casa, Minha Vida in tiers 1 and 2 in municipalities of the Central-West, Northeast, and North regions.

The limit of R$ 255,000 is expected to be corrected by an average of 4%, according to technicians from the Ministry of Cities, in a scenario where the table had been frozen for about three years. In the interior municipalities of São Paulo and Rio de Janeiro, the property value ceiling was also adjusted by the same percentage.

In the capitals, the value was maintained at R$ 350,000, and this ceiling of R$ 350,000 also serves as a reference for Tier 3 and for the income tier up to R$ 12,000.

FGTS, Curator Council, and the Timeline Until the Change Becomes Law

The institutional pathway helps explain why these updates tend to be announced in stages. First, the Ministry of Cities defines the proposal and consolidates the parameters.

Then, the change is brought to the Curator Council of FGTS, which has the final say on the approval of the new rules within the financing and linked discount arrangement.

This detail is important because Minha Casa, Minha Vida does not depend only on a political decree, but on technical and financial alignment to sustain subsidies, discounts, and interest rate conditions.

That is why the mentioned timeline involves a decision by the end of the week at the ministry and the formalization of the proposal to the Curator Council of FGTS in the following month, before it becomes applicable law.

What to Observe Now If You Want to Join Minha Casa, Minha Vida

For those seriously looking at home ownership, the main point is to keep track of which income tier your family fits into and what conditions are associated with it: subsidy, interest rates, and property ceiling. A small income variation can completely change the type of available benefit, especially in the transition between Tier 1 and Tier 2.

It is also worth observing the ceiling on property value in your region and the impact of adjustments by state and type of municipality because the feasibility of financing depends on the intersection of income, rate, possible down payment, and property price.

And, with the government’s goal of expanding contracts and reaching 3 million housing units by December, the expectation is that the search and competition for units and credit will increase as the new tiers are approved.

The move to raise the income tiers of Minha Casa, Minha Vida signals an attempt to broaden the program’s reach with two fronts at the same time: bringing more families under the rules of subsidies and low interest rates and, at the same time, providing a pathway for the middle class to finance amid the difficulty of credit tied to savings.

If the change advances in the Ministry of Cities and is approved by the Curator Council of FGTS, the entryway to the program is likely to become larger in the short term.

Now I want to understand your situation: do you think that increasing the income tiers of Minha Casa, Minha Vida helps more those trying to buy their first home or pushes prices higher? And, in your city, does the ceiling on property value seem compatible with what exists in the market today?

Senhor (a)

O aumento da faixa de renda ajuda, porém nós que pagamos aluguel não temos condições de pagar uma entrada com o valor alto, os valores dos apartamentos em Goiânia são muito altos. Eu estou precisando comprar, não tenho entrada, os juros são muito altos, e nós que pagamos aluguel não temos condições de pagar a entrada.