Portuguese

Portuguese  English

English  Spanish

Spanish

Real-Life Simulations Show That A Whole Life Insurance Can Cost Less Than A Streaming Subscription And Still Provide Million-Dollar Coverage In Case Of Serious Unexpected Events.

The topic of whole life insurance is often treated with some taboo or mystery in the financial market. Many brokers avoid detailing the numbers and prefer to highlight only the emotional benefits of protection. However, a technical and comparative analysis between insurers shows that, with just over R$ 100 per month, it is possible to guarantee up to R$ 1 million in total coverage, including death, disability, critical illnesses, and funeral assistance. The cost, however, varies according to age, health, and the policyholder’s objectives.

This price difference has mathematical logic. The younger and healthier the insured, the lower the risk and the cheaper the policy. At 30 years old, a standard profile can obtain million-dollar coverage for R$ 102.90 per month. However, above 50, the cost increases exponentially and may no longer be advantageous. The ideal time to purchase insurance is when one is in an active earning phase, especially for self-employed individuals or those supporting dependents.

Comparison Between Insurers And Coverages

Among the analyzed insurers, Asus had the lowest monthly cost, R$ 102.90, with coverage of R$ 1 million and funeral assistance of up to R$ 15,000.

-

The Federal Revenue Service now automatically cross-references everything you declare with data from banks, credit cards, brokerage firms, and insurance companies, and any discrepancy between your income and your expenses triggers an alert in seconds.

-

Amid global tensions, Brazil blocks the United States’ proposal at the WTO and paves the way for a trade crisis and possible retaliations.

-

Shopee opens the largest logistics warehouse in Brazil in Guarulhos: 220,000 m² on Dutra, contract signed before construction, pays R$ 45/m² and accelerates deliveries at scale, putting pressure on Mercado Livre and Amazon.

-

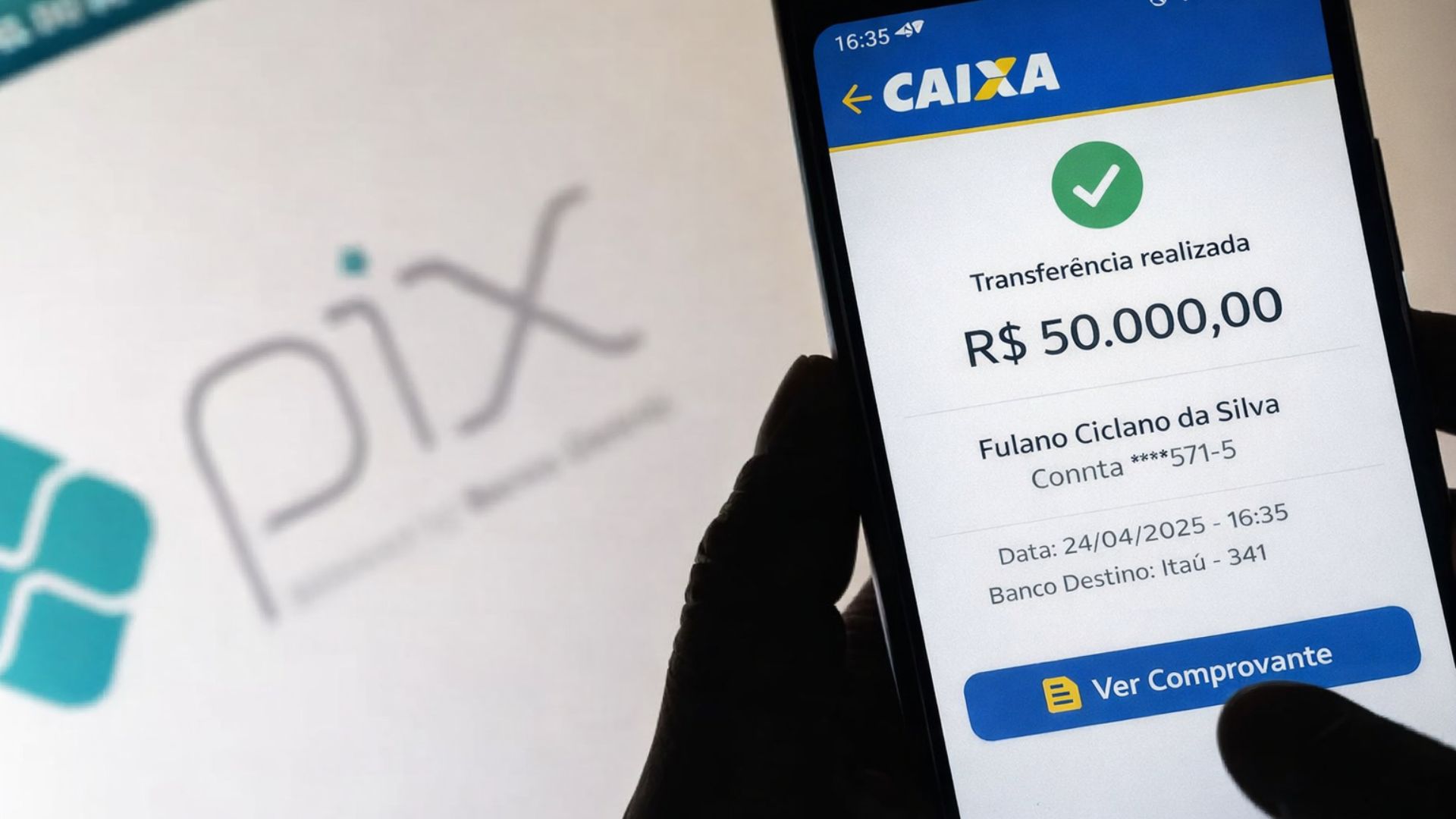

After mistakenly transferring R$ 50,000 via Pix, a man will receive the amount back along with R$ 10,000 for moral damages from the recipient.

On the other hand, Icatu, with a premium of R$ 353, offers relevant additional coverages such as advancement for terminal illness and permanent disability, raising the total coverage to over R$ 3 million.

At the top of the table, options like MAG and MetLife offer monthly premiums close to R$ 700, with complete packages that include accident compensation, critical illnesses, and daily hospitalization.

This variation reinforces that the “best” insurance depends on personal strategy.

For those investing up to R$ 2,000 per month, basic coverage is sufficient to protect family assets in case of unforeseen events.

Meanwhile, those investing over R$ 3,000 may consider more robust plans, with multiple layers of compensation and succession protection.

When Whole Life Insurance Stops Being Worth It

Life insurance is not lifelong and should not be. It is a temporary protection tool for moments of vulnerability.

From the age of 55, the cost increases to the point that it may be more efficient to switch to a private pension plan.

In this model, the invested amount is fully returned to the family, while traditional insurance is merely a risk contract: if nothing happens, there is no payout.

Therefore, the primary function of insurance is to ensure immediate liquidity in extreme situations such as accidents, disability, and severe diagnoses, and to prevent family financial collapse.

After the wealth accumulation phase, it makes more sense to reduce exposure and direct contributions to succession instruments or pension plans.

The Importance Of Proportional Planning

Experts recommend that the amount spent on life insurance should not exceed 25% of monthly contributions.

Spending more than that jeopardizes financial growth and distorts the balance between protection and investment.

With proper planning, it is possible to protect the family without interrupting wealth accumulation, and still choose personalized coverage for one’s professional profile, such as daily disability benefits for those who rely on manual or intellectual labor.

The central point is that life insurance should not be seen as a fixed expense, but as a safety bridge between the construction phase and financial consolidation.

It exists to cover the gap between the start of the journey and asset stability.

Understanding the real function of whole life insurance is the first step to making informed choices and avoiding costly and unnecessary contracts.

What few brokers explain is that insurance is a transition tool, not a subscription for a lifetime.

Have you calculated how much a million-dollar coverage would cost for your profile? Comment below what would be the ideal monthly protection amount that makes sense in your financial reality.

-

-

-

-

4 pessoas reagiram a isso.