Portuguese

Portuguese  English

English  Spanish

Spanish

IMF Shows Dollar at 58% of Global Reserves in 2025, Lowest Level in 25 Years; Yuan and Rupee Advances Pressure American Hegemony.

The report released by the IMF in 2025 brought a number that resonated from Wall Street to Beijing: the dollar has fallen to 58% of global foreign exchange reserves, the lowest level in 25 years. It may seem technical, but the effect is political: it is proof that the American currency, the pillar of the international financial order since the end of World War II, is gradually and quietly losing ground.

The data confirms what has been sensed in the corridors of power: the dollar no longer reigns alone. Meanwhile, the Chinese yuan and the Indian rupee are gaining ground, supported by billion-dollar agreements in the BRICS, new currency swap mechanisms, and alternative payment systems to Swift.

For Washington, it is a red alert: each percentage point lost means hundreds of billions of dollars in influence lost over global trade and finance.

-

USA and China compete for Brazil over resources that could be worth trillions — rare earths put the country at the center of a global dispute

-

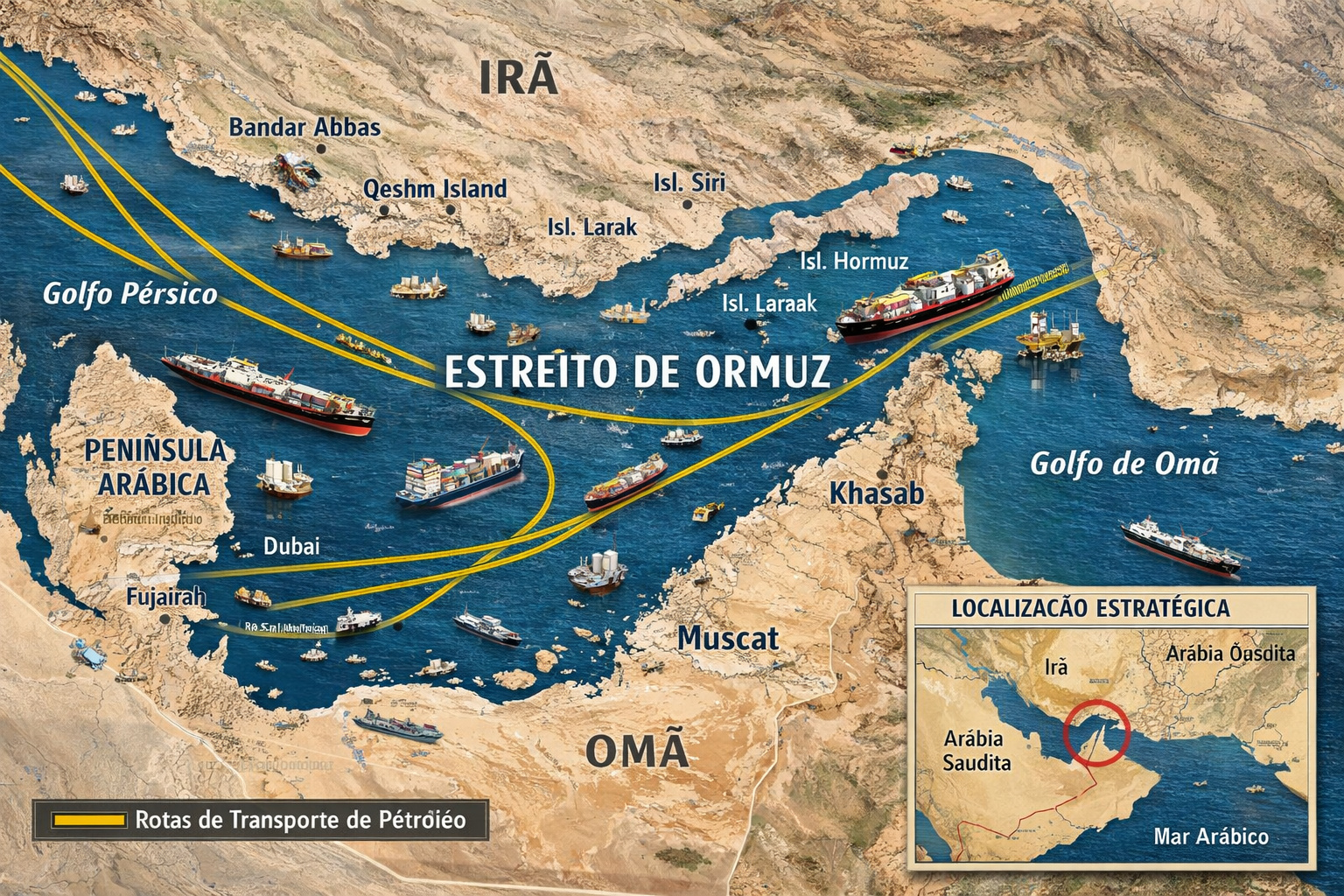

Global summit with over 40 countries pressures Iran for a blockade in the Strait of Hormuz and warns of direct impact on oil, food, and the global economy.

-

Russia has broken the U.S. maritime blockade to send oil to Cuba and is now loading a second ship while Trump says that “Cuba is next” in a possible military action against the island.

-

Spain challenges the USA and closes its airspace for operations against Iran, raising global tension and provoking the threat of a trade rupture.

The Rise and Fall of the Dollar Empire?

Since the end of the Cold War, the dollar has always been the safest asset on the planet. In 2001, it represented over 72% of international reserves of central banks. This supremacy allowed the United States to finance deficits, impose sanctions, and maintain unparalleled firepower.

But the curve began to shift after the 2008 crisis. Confidence in the American currency was shaken, and many countries began seeking alternatives to not rely solely on Washington. From 2014 onward, with increasing geopolitical tensions, the process of diversifying reserves gained momentum.

We reached 2025 with the IMF confirming the fall to 58% — a level not seen since the 1990s. The movement may seem slow, but for market analysts, it is a seismic change: in just two decades, the dollar has lost over 14 percentage points of market share in global reserves.

The Advance of the Yuan: From Periphery to Center

The biggest beneficiary of this decline is undoubtedly China. The yuan, which in 2001 was practically irrelevant in the international system, now accounts for about 5% of global reserves and, more importantly, over 40% of trade between Brazil and China.

The leap is not due only to the strength of the Chinese economy but to a deliberate strategy by Beijing. The creation of billion-dollar currency swaps, such as the one signed with Brazil in 2025, provides liquidity to the currency.

Systems like CIPS (the Chinese alternative to Swift) offer transaction routes outside the American orbit. Energy agreements with Russia, Iran, and Saudi Arabia pave the way for the so-called petroyuan.

The Rupee Enters the Game

If the yuan is already a reality, the Indian rupee emerges as a novelty in 2025. New Delhi has resorted to bilateral agreements to settle imports of oil and exports of pharmaceuticals in rupees and pressures the BRICS to have the currency considered in multilateral transactions.

It is still early to say if the rupee will have the same reach as the yuan, but the message is clear: the dollar is no longer the only viable option.

For many emerging markets, using local currencies means lowering costs, avoiding sanctions, and gaining more geopolitical leverage.

Brazil at the Epicenter of the Dispute

Brazil appears as a laboratory for this transition.

- The R$ 157 billion swap with China opened the doors for the yuan.

- Trade with Russia is already beginning to be partially settled in yuan.

- And India pressures for more agreements in rupees within the BRICS.

For Brasília, the challenge is balancing interests. On one hand, currency diversification strengthens agriculture and the export industry, reducing costs and risks. On the other, there is a risk of swapping dependence on Washington for a new dependence on Beijing or New Delhi.

The Alert from Washington

In the U.S., the dollar’s fall to 58% of reserves is treated as a sign of the erosion of American hegemony.

The fear is not of losing absolute leadership overnight, but rather facing a slow and continuous decline, in which more and more contracts for energy, food, and technology begin to be denominated in alternative currencies.

This weakens the U.S.’s ability to impose sanctions — such as those applied to Russia after the war in Ukraine — and reduces Wall Street’s allure as the sole destination for investments.

Europe in a Delicate Position

The European Union, caught between Washington and Beijing, watches cautiously. The euro maintains a stable share but cannot expand as a real alternative to the dollar.

Meanwhile, it must deal with the implementation of the EUDR (Anti-Deforestation Regulation), which pressures Brazilian exporters and threatens to further strain relations with emerging countries.

The ‘New Currency War’

Experts describe the 2025 scenario as the beginning of a “currency war”. It is not about immediately replacing the dollar but about gradually reducing its centrality. This is what economists call monetary multipolarization: a world in which different currencies — yuan, rupee, digital real (Drex), euro — compete in spaces previously dominated exclusively by the dollar.

The decline of the dollar in global reserves opens new opportunities for Brazil: diversifying partners, reducing currency costs, and gaining voice in forums like the BRICS. But it also brings risks: exposure to the yuan and rupee may mean greater dependence on countries that play hardball in geopolitics.

The fact is that, in 2025, the hegemony of the dollar is officially shaken. The lingering question is whether Brazil will use this transition to gain more autonomy or end up hostage to a new center of power.

Seja o primeiro a reagir!