Portuguese

Portuguese  English

English  Spanish

Spanish

With the Arrival of the New IVA Tax Model, from the Tax Reform, Small and Medium-Sized Enterprises Registered under Presumed Profit Will Need to Review Their Accounting and Operational Structure to Avoid an Increase in Tax Burden and Loss of Competitiveness in the Market.

The new IVA tax model, which will unify federal, state, and municipal taxes, will bring a profound transformation in how companies calculate and collect consumption taxes. The simplification promised by the tax reform comes with new technical requirements, which are particularly alarming for entrepreneurs under the Presumed Profit regime, which currently serves a substantial portion of small and medium-sized Brazilian enterprises.

The reformulation of the tax system will demand greater transparency, traceability, and digital control of operations, meaning that many companies will have to adapt quickly or face increased costs and tax risks.

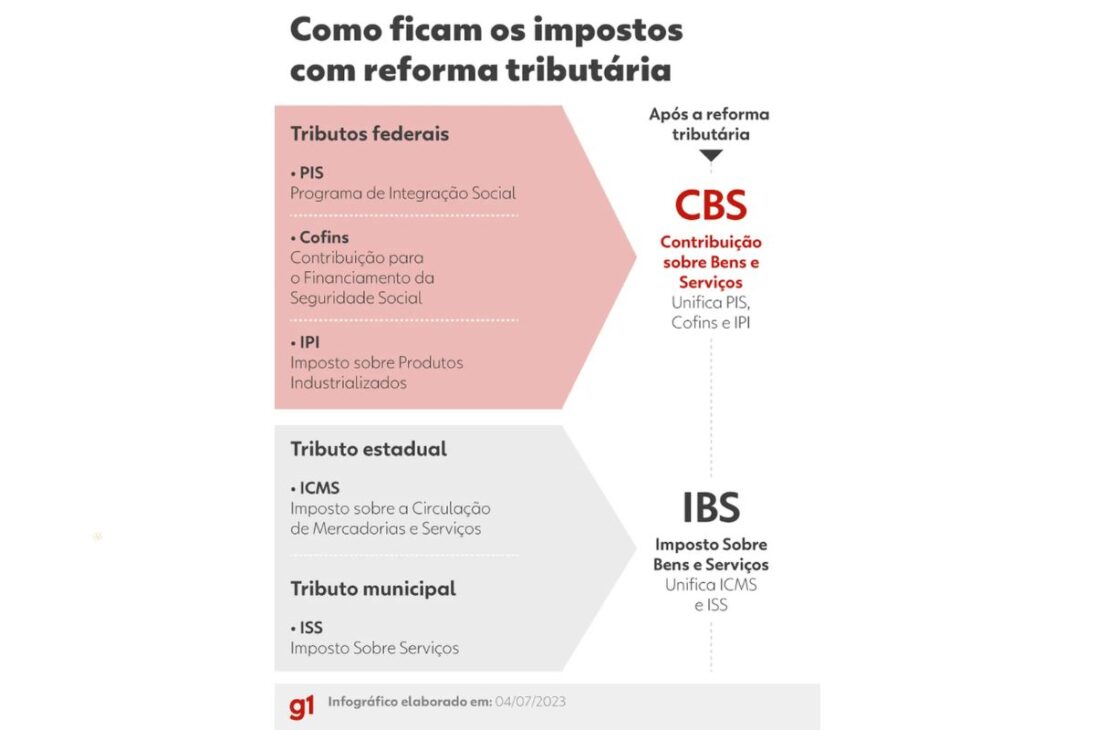

What Changes with the New IVA Tax Model

The Value Added Tax (IVA) will consist of two fronts: the CBS (Contribution on Goods and Services), under federal jurisdiction, and the IBS (Tax on Goods and Services), managed by states and municipalities.

-

A new Brazilian shopping center worth R$ 400 million will be built in an area equivalent to more than 4 football fields, featuring 90 stores, 5 cinemas, a supermarket, a college, and parking for 1,700 cars, potentially generating 3,000 jobs.

-

Larger than entire cities in Brazil: BYD is building a 4.6 km² complex in Bahia with a capacity for 600,000 vehicles per year, but the discovery of 163 workers in conditions analogous to slavery has shaken the entire project.

-

With an investment of R$ 612 million, a capacity to process 1.2 million liters of milk per day, Piracanjuba inaugurates a mega cheese factory that increases national production, reduces dependence on imports, and repositions Brazil on the global dairy map.

-

Brazilian city gains industrial hub for 85 companies that is equivalent to 55 football fields.

Together, they will replace taxes such as PIS, Cofins, ICMS, and ISS, creating a non-cumulative model where the tax is paid only on the value added at each stage of the production chain.

For companies operating under the Presumed Profit system, this change represents a paradigm shift.

The current system allows for simplified assessment based on a presumed profit margin defined by law.

With the IVA, it will be necessary to register and prove all operations, detailing tax credits and debits transparently and traceably.

In practice, the new model will require integrated systems, more technical accounting, and automated fiscal management.

The informality, which is still common in small operations, is likely to disappear with digitalization and the automatic cross-referencing of data by the Federal Revenue Service.

Why the Presumed Profit May Lose Relevance

The Presumed Profit regime has always been a simplified and advantageous alternative for smaller companies.

However, the logic of the IVA does not fit well into this format, as it is based on the compensation of tax credits.

Service sectors, such as law, consulting, health, education, and technology, are likely to be the most affected.

This is because these activities generate few tax credits, since their main costs are concentrated in labor, and wages do not generate IVA credits.

The result is heavier taxation, with no possibility of compensation.

In contrast, companies that deal with inputs or goods may have a lesser impact, as they will be able to recover part of the amounts paid along the production chain.

Still, a more sophisticated control of invoices and accounting documents will be necessary to ensure the correct utilization of credits.

Impacts on Accounting Routine and Financial Management

The new IVA tax model will require Presumed Profit companies to adopt a control standard similar to that of large corporations.

This includes the use of ERP software, issuance of integrated electronic invoices, and maintaining accurate records of entries, exits, and tax credits.

This scenario changes the operational logic of the financial and tax departments. While simplicity was once the biggest attraction of the Presumed Profit, now the challenge is the technical complexity and rigidity of tax compliance.

The IVA will require constant data reconciliation and regular internal audits, as inconsistencies can result in automatic penalties from the Federal Revenue’s cross-referencing systems.

This means increased costs for accounting, consulting, and technology, which can weigh on the budgets of small and medium-sized companies.

Companies that take too long to adapt risk paying more taxes than necessary or losing important tax credits.

Real Risk of Increased Tax Burden

One of the most sensitive points of the reform is the potential increase in tax burden for sectors with little credit generation.

Under the current regime, the Presumed Profit offers effective rates between 11% and 16%, depending on the sector.

With the IVA, this burden could rise to 18% or more, depending on cost structure and tax compensation capacity.

Another issue is the reduction of fiscal planning flexibility.

The new system tends to standardize rules and eliminate sector-specific exceptions, limiting tax optimization strategies that many companies currently use.

The result is a narrower profit margin and less room for strategic accounting adjustments.

For highly competitive segments, where prices are sensitive and profitability is tight, any increase in tax burden can compromise financial sustainability.

How Companies Should Prepare for the IVA

The transition to the new IVA tax model will be gradual, but preparation needs to start now.

The adaptation period should include:

Reviewing the tax compliance, simulating scenarios between Presumed Profit and Real Profit;

Investing in fiscal automation, with software capable of calculating and recording IVA credits and debits;

Training accounting and financial teams, focusing on indirect taxation and digital compliance;

Reviewing contracts and pricing, as the IVA will impact pass-throughs, margins, and agreements with suppliers and clients;

Sector impact analysis, considering the nature of costs and potential credit generation.

Companies that anticipate the change will be able to reduce risks, adjust prices, and avoid surprises in cash flow. On the other hand, a lack of planning can lead to silent losses, especially in the first years of the transition.

-

-

-

-

-

30 pessoas reagiram a isso.