English

English  Francês

Francês  Alemão

Alemão  Italiano

Italiano  Japonês

Japonês  Norueguês

Norueguês  Portuguese

Portuguese  Spanish

Spanish

The Lower Supply of Raw Materials and High Global Demand Will Drive Prices of Oil, Uranium, Copper, and Aluminum Up

The green economy is already a reality, and countries around the world have been trying to reduce environmental risks and ecological scarcity, aiming for sustainable development without degrading the environment. However, as paradoxical as it may seem, this “green economy” is expected to drive up the prices of various commodities, such as oil, uranium, copper, and aluminum, says Ruy Alves, manager at Kinea Asset.

Read Also

- Titanic Comes Back to Life in China; the Luxury Ship Labeled as ‘Unsinkable’ Is Under Construction and Will Be the Size of the Original

- The Largest Oil Company in Brazil Has Accounts Frozen in Bolivia Due to a Dispute Over a Gas Field Area

- Macaé Will ‘Get on Track’! One of the World’s Largest Engineering, Services, and Infrastructure Companies Wants to Build a Locomotive Factory in the City

- Epson Calls Students from All Areas for Positions in São Paulo in Industrial, Operations, Marketing, Human Resources, and Much More

The green economy is closely related to the ecological economy but has a more politically applied focus. This was the theme of the Coffee & Stocks held yesterday (05/28) with Ruy Alves, global macro manager at Kinea (check out the full discussion in the video below).

The issue is far from trivial; Kinea published a 9-page letter this week explaining how raw materials such as oil, uranium, aluminum, and copper may see their prices rise.

-

Rio Grande do Sul accelerates energy transition: State invests in renewable technologies and consolidates decarbonization strategies and pathways to attract billions in new industrial investments.

-

With 160,000 m² of collectors, an area larger than 20 football fields, Silkeborg, in Denmark, hosts a solar thermal plant that heats 19,500 homes and could become the largest solar heating plant in the world.

-

A study reveals the expansion of renewable energy procurement in Brazil and shows how companies are taking advantage of opportunities to reduce expenses, ensure energy efficiency, and strengthen strategic environmental commitments.

-

Mato Grosso do Sul excels in the sugar-energy sector: the state reaches a milestone of 22 operating mills and accelerates the production of clean energy in MS with a focus on sustainability.

The reasons are not the same for all raw materials, but if we had to summarize it in one sentence, we could say: supply is unlikely to grow (either because no one wants to invest in new projects or due to environmental issues) and demand will remain strong or even increase, even for those commodities that are not environmentally friendly.

See Below the Effects of a Green Economy on the Prices of Oil, Copper, Aluminum, and Uranium, According to Ruy Alves, Manager at Kinea Asset

Looking back to 2005, during George W. Bush’s administration, the United States started its version of the dream field: a new renewable energy project using ethanol extracted from corn to be mixed with gasoline, thereby generating a renewable energy source that is neutral in carbon emissions to the atmosphere.

The result of this decision was a subsequent increase in corn prices from ¢200/bushel in 2005 to ¢800/bushel in 2011. This effect impacted not only corn prices: the grain competes for area with various other crops, primarily with soybeans. This process led to a widespread increase in agricultural prices, also affecting beef prices subsequently, as cattle not only compete for pasture space with corn but also feed on it.

We could say that currently, the world is undergoing a process similar to that of the United States in 2005, but now on multiple fronts and on a global scale. “Our desire to reduce carbon emissions, pollution, and move to an ESG economy (the acronym represents the shift in companies’ social impacts) is noble in its intents, but it also comes at a cost that will reflect on various commodities over the next few years.”

These effects range from increased demand for “green” applications, such as copper in electrification, to reduced supply of other commodities due to environmental issues, such as aluminum, and also to potential problems in the supply of other commodities because we are discouraging investments, such as in oil.

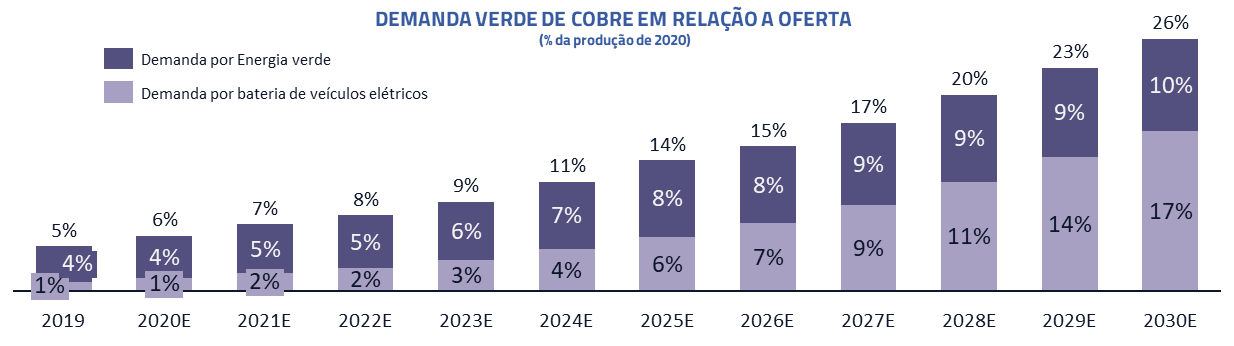

Copper – Strong Green Demand with Limited Supply Capacity

The transition to a renewable energy matrix is not limited solely to energy generation; it also encompasses its transmission and storage. However, for energy transmission, no metal is more efficient than copper.

If we are to transform our energy matrix from fossil fuels to renewables, the entire transmission network will have to be rethought. The planned wind and solar farms require distribution networks, and electric cars demand a large quantity of the metal compared to traditional vehicles.

In addition to the growth in demand, we should also face a challenging environment for supply. Copper is a rare metal, and investments in extraction in recent years have been below what is necessary to meet the growing demand. Important regions such as Chile and Peru are currently discussing taxes that may discourage future investments, and new exploration areas are located in regions with greater political instability, like Africa.

New exploration investments, if initiated today, will take at least five years to generate substantial supply, and it appears there will be no prospect of supply meeting the “green” demand for energy distribution and electric cars. This imbalance will likely have to be resolved through higher prices.

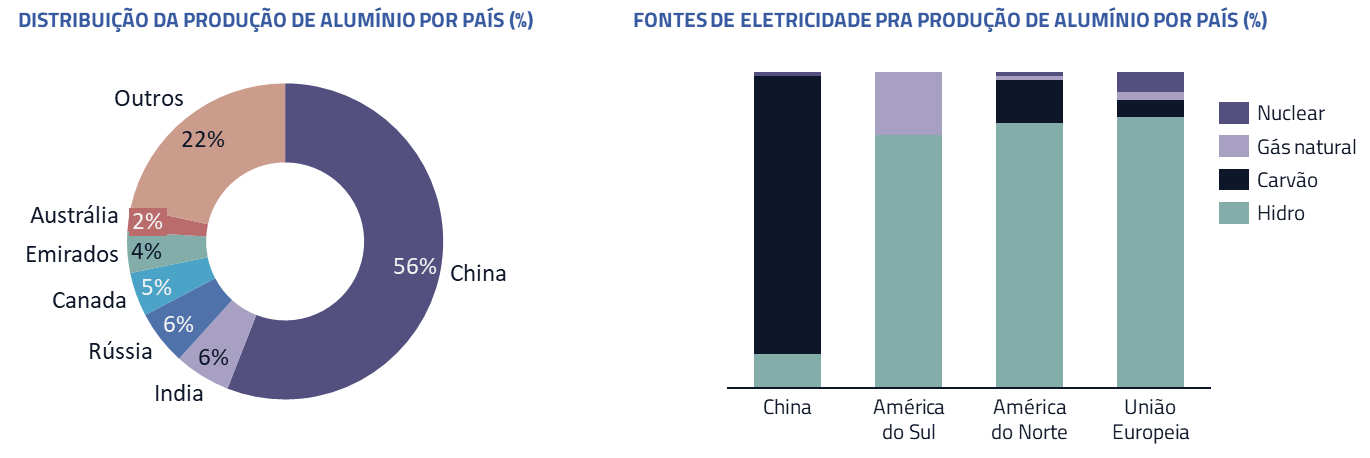

Aluminum – Environmental Issues Restricting Supply

According to Ruy Alves, aluminum reflects a distinct problem from copper: its production demands a huge amount of electrical energy. Aluminum is produced from bauxite as raw material, one of the most abundant metals in the Earth’s crust. However, due to the energy required, the metal can be considered as “condensed electricity.” Its production, in the West, occurs in regions with abundant supplies of cheap energy: for example, in the cases of Brazil and Norway, two of the main producers, this production is located near hydropower plants.

The problem for the metal is that the main producer, China, responsible for more than half of global production, is a country that has its energy matrix based on coal, the source of the highest carbon emissions into the atmosphere.

In recent years, China has reassessed its stance on emissions and pollution, trying to reverse a drastic situation of extremely high pollution levels in various regions of the country. Anyone who has been to China must have noticed the constant “fog” of pollution, combined with coal trucks that drive by to feed energy production.

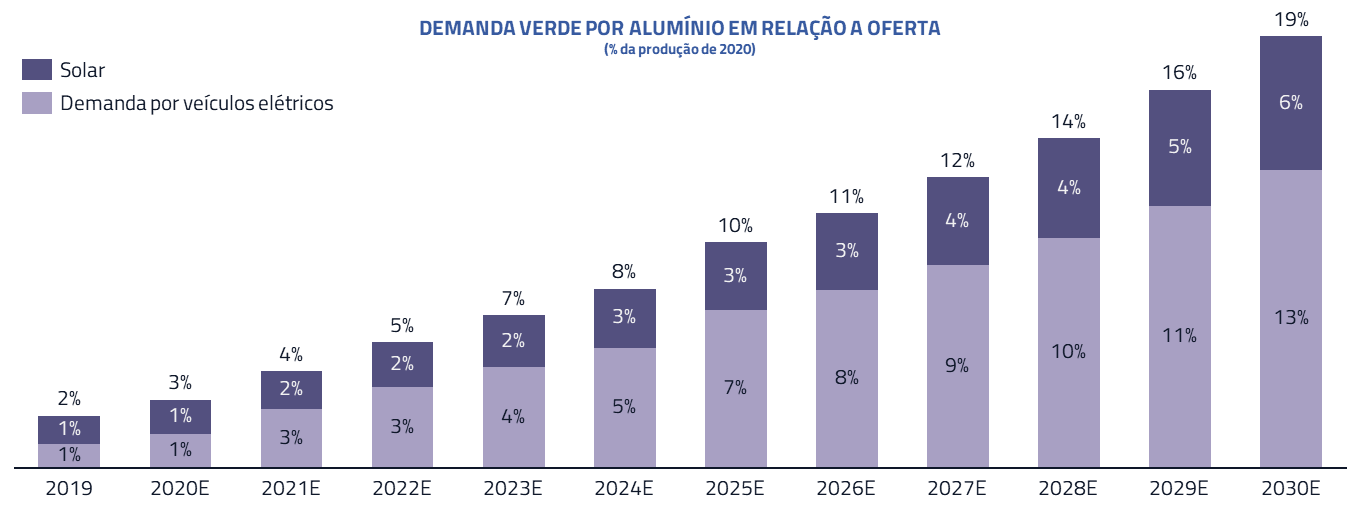

The consequence of this new stance has been a plateau in global production, which had been growing strongly until 2017. Looking ahead, we should face strong demand from economic reopening along with the world’s inability to respond with corresponding supply, creating a deficit and consequent drop in stocks, which are already at levels below the historical average.

The metal is also expected to see its demand heated by the green economy, replacing steel in transport and construction for being lighter, as well as its use in solar panels. The combination of more limited supply and heated demand in the coming years will also likely be resolved through higher prices for the metal.

Oil – The Risk of Disregarding the Energy That Sustains Our Society

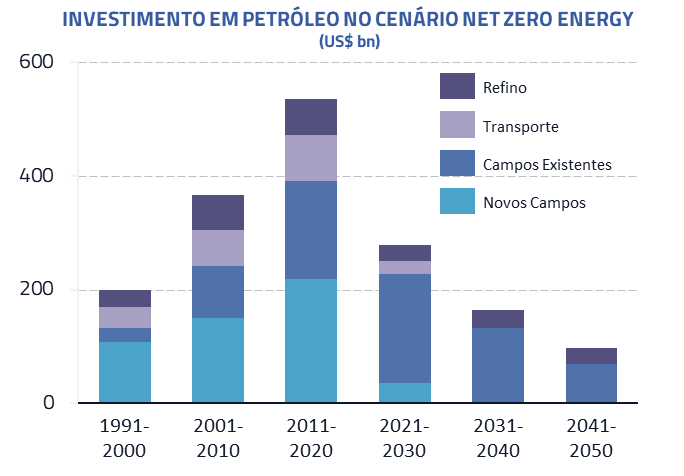

Oil has been the main villain of carbon emissions within the context of global warming over the past decades. There is not a day when global leaders do not appear in the press, presenting a negative outlook on the commodity. Investment funds today activated discourage investments in the sector, and the international oil agency itself has suggested that investments in the sector should cease to meet carbon emission targets.

However, oil is very important for humanity. More than 70% of the energy that drives the United States, the largest economy in the world, comes from fossil sources.

The use of fossil fuels, with their enormous energy density, has allowed us to spend only 3% of global GDP on energy generation, being able to enjoy the benefits of that energy for the remaining 97% of GDP. The amount of energy we produce is equivalent to every person on the planet having 70 people working 365 days a year for them.

In practice, the decision to move away from oil will mean that we must spend more of the global GDP on energy generation, and less on the benefits of that generation. An EROEI of 10x, for example, would mean that the percentage of global GDP attributed to energy generation would rise from 3% to 10%. In other words, we will likely have to pay more for the energy we consume. A similar effect to what happened with the price of corn, mentioned above.

In the last decade, we have experienced a benign environment for oil prices, due to the entry of shale oil production in the United States, which has become, over the past few years, about 10% of the total global production. However, for the coming years, we expect a different scenario: shale companies in the United States have experienced financial problems in recent years, and the current Biden administration is actively discouraging investments in the sector (limiting access to federal lands and canceling important pipelines). The result is that production is already showing a decline, and the number of new rigs is at suboptimal levels to ensure future production growth.

This occurs at a time when stocks are beginning to normalize after the pandemic, and demand is starting to show signs of recovery. With marginal supply now concentrated in the hands of OPEC+, we may see substantially higher prices in the coming years.

Uranium – The Only Scalable Source of Carbon-Free Baseload Electricity

Renewable energies, such as wind and solar, suffer from a serious problem: intermittency. We cannot expect that wind or sunny days are constant. As battery technology does not allow us to store electrical energy for future use, we need clean energy sources that can be used as baseload electricity. There are two potential clean sources for this role: hydropower and nuclear.

However, hydropower also presents serious environmental problems. One of them is how nearly all the most obvious areas on the planet have already been explored for generating this type of energy; new areas, when they exist, imply the creation of enormous reservoirs that have deep environmental implications. In this context, nuclear energy presents itself as the only scalable alternative for generating baseload energy that is carbon-free.

Several countries are already moving toward expanding their nuclear energy generation capacity. China, with its energy matrix heavily concentrated on coal, has embarked on a project to build new plants. In the United States, Joe Biden’s administration is also studying the resumption of nuclear power plant construction projects to meet carbon emission targets. In Europe, several plants that were scheduled for decommissioning are being kept in operation due to the infeasibility of meeting carbon emission reduction goals with other energy sources.

The consequence of this process should be a significant increase in demand for uranium over the next decade. The demand growth will, on the other hand, face a subpar supply function: over the last decade, especially after the tsunami that affected Fukushima in Japan, uranium production has been drastically reduced. We are already observing declines in stocks, and projections for the coming years indicate a substantial deficit that should lead to price increases.

Kinea emphasizes its commitment to forming an environmentally responsible society and advocates for initiatives for a cleaner world, with less carbon and better corporate governance practices.

However, the point that Kinea raises in its article is that there are indeed costs that society and investors must be aware of during this transition period. The green economy will demand resources in areas where we are currently unable to provide supply. This will result in movements in commodity prices that may become significant, and as investors, we must stay alert.

by- Kinea

Seja o primeiro a reagir!