Portuguese

Portuguese  English

English  Spanish

Spanish

Federal Revenue Creates System That Centralizes Property Information With Unique Code And Expands Data Cross-Referencing On Retroactive Rents, Increasing Risk Of Audits And Fines For Taxpayers Who Did Not Declare Rental Income.

The Federal Revenue regulated the Brazilian Property Registry (CIB) and began requiring notaries and municipalities to share, in (almost) real-time, data on property transactions in the Sinter, a national system managed by the Federal Revenue itself.

Published in the Official Gazette on August 18, 2025, IN RFB No. 2,275/2025 provides for implementation by November 25, 2025, when the CIB will begin to be incorporated into registrational acts and municipal registrations.

From then on, registered lease contracts will directly feed the tax authority’s databases, allowing cross-referencing with IRPF and IRPJ declarations.

-

Brazil blocked a proposal from the United States at the WTO that would make the exemption from tariffs on digital products like streaming and ebooks permanent, favoring American tech giants at the expense of developing countries.

-

IPTU exemption for seniors in 2026: see how to secure the benefit.

-

The institute that trained the greatest aerospace engineers in Brazil has just opened its first campus outside São Paulo after 75 years: ITA Ceará will have R$ 445 million, new courses in energy and systems, and classes are expected to start in 2027.

-

Luciano Hang, owner of Havan, goes to Juiz de Fora after the tragedy in February, brings R$ 1 million, hands out R$ 2,000 cards, and donates up to R$ 15,000 to victims in the region.

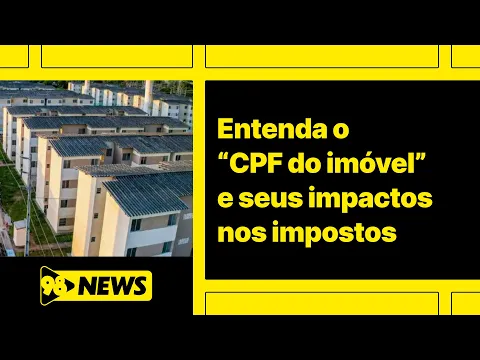

What Changes With IN 2.275/2025 And The CPF Of Properties

The regulation details the obligations of notarial and registration services: to integrate into the Sinter and adopt the CIB as a unique identifier in documents and systems, with a schedule agreed upon between the Federal Revenue, CNJ, and registry operators.

The annex of the act lists steps for diagnosis, prototyping, approval, and go-live by 11/25/2025.

In practice, the CIB acts as a “CPF of the property,” standardizing registrations and facilitating the sharing of contracts and deeds with tax administrations.

The Federal Revenue itself describes the CIB as a tool for legal certainty and data integration in the context of tax reform.

Furthermore, Supplementary Law No. 214/2025 and Decree No. 11,208/2022 include the CIB within the Sinter and list property transactions subject to sharing, including leasing, onerous assignment, and leasing, making the cross-referencing of declared (or not) income in the Income Tax natural.

Retroactivity: Why The Tax Authority Can Look Back

The timeline available to the Treasury to establish tax credit by official assessment is, as a rule, five years, counted from the first day of the subsequent fiscal year after the triggering event, pursuant to Article 173, I, of the CTN.

This means that, with the databases fed from the end of 2025, the Federal Revenue can reach events that occurred since 2021, within the decadential period.

The Superior Court of Justice has already consolidated the logic of counting the deadline from the following fiscal year, regardless of when the administration became aware of the triggering event.

How The Cross-Referencing Is Likely To Occur

With the CIB present in the documents and systems of the notaries, information on lease contracts, amendments, and terminations will be sent to the Sinter immediately after the execution or registration.

The municipalities will contribute cadastral data (such as IPTU and addresses), facilitating the link between property, ownership, and CIB.

Subsequently, the Federal Revenue cross-references this information with declarations already submitted, identifying inconsistencies or omissions.

The flow is continuous and automated, without relying on individualized notice campaigns. There is also a financial layer.

Since January 2025, the update of the e-Financeira has expanded the universe of institutions required to report transactions, including payment institutions.

The submissions are consolidated by account (credits and debits), without identification of the type of transfer — including PIX — and serve the risk management of the tax authority.

This expansion reinforces the cross-referencing with the CIB and reduces the scope for “off-the-books” rents.

Fines And Penalties: From 75% To 150%

When the omission of income is detected and the assessment is made officially, a 75% fine is applied on the tax due, in addition to interest at the Selic rate.

In cases where intentional wrongdoing is proven — conduct of fraud, evasion, or collusion as defined by law — the fine can be upgraded to 150%.

Administrative jurisprudence requires demonstration of intent to maintain the qualification. For those who take action proactively, there are relevant differences.

In the case of voluntary payment before any official procedures, no official fine is applied; late payment fines (0.33% per day, limited to 20%) and interest apply.

After notification or assessment, the legislation provides for a 50% reduction of the official fine if the taxpayer pays (or parcels legally) the debt within the deadline.

In summary: before the fiscal action, the taxpayer avoids the official fine; after it, they can reduce it by half.

Who Is More Exposed With The Property CPF

Individuals as landlords with informal contracts tend to be captured as old instruments are formalized or when new amendments are notarized with the CIB.

Corporate investors who do not correctly segregate rental income from other income will have their numbers compared by the link between CIB, deeds, and accounting records, potentially impacting IRPJ and CSLL.

Situations of beneficiary different from the declarant — such as informal power of attorney among family members — tend to trigger alerts.

And rents deposited in third-party accounts become more visible in light of the consolidated reporting of financial movements, even without individualization by type.

How To Act To Regularize Without Aggravating The Liability

The first step is to amend the declarations (IRPF or IRPJ) from the last five years whenever there are discrepancies, providing correct values and, if applicable, deductions supported by law.

Next, pay the due tax with late payment fines and Selic.

Before any inspection procedures, this approach constitutes voluntary disclosure — a situation where the official fine does not apply.

If there is already an infraction notice or notification, payment within the legal deadline can reduce the official fine by half.

It is recommended to formalize the contract at the notary’s office, ensuring the correct issuance of the CIB, and to organize receipts of payments made (electronic receipts, DARFs, and required documents), as handwritten notes are insufficient in case of questioning.

Important Dates

The regulatory calendar provides for implementation of the CIB by 11/25/2025, followed by a validation and consolidation phase until December.

On 12/31/2025, the calendar year closes; the IRPF 2026 submission will require that rental income from 2025 is already correctly declared.

Throughout 2026, the trend is an intensification of the use of CIB/Sinter in fiscal cross-referencing, given the agreed timeline between the Federal Revenue, CNJ, and registrars.

What Do Agencies And Experts Say

Entities in the property registry sector have stated that the integration increases legal security and reduces fraud in the transaction chain.

The Federal Revenue, on the other hand, has highlighted the standardization of registries and the integration of data as central objectives — especially in the context of tax reform and the creation of the unique identifier.

Tax experts recognize that the five-year decadental period limits the temporal scope of collections, but warn that the combination of fines and interest can multiply the amount owed when there are repeated omissions over several years.

Those who received rents between 2021 and 2025 and have not yet regularized have a short window to correct the past before the new infrastructure makes omission easily detectable.

E para onde vai esse dinheiro de impostos? Educação não tem, Sus não funciona, falta hospitais, medicamentos faltando, corrupção no Brasil virou modinha,vai se pagar mais impostos para sustentar vida luxuosa de políticos ****,governo ****.

Medida acertada. Afinal, aluguel de imóveis é rendimento tributável e deve pagar imposto de renda sim. Também, deveria acabar com essa farra de inquilino ter que pagar IPTU, porque não é dono do imóvel. Quem deve pagar esse tributo é o proprietário.

Vc deve ser um desses que mama nas tetas do governo.

Nelson, o aluguel irá aumentar e quem pagará esses impostos serão os inquilinos e não os proprietários ou seja a taxação e o pente fino na arrecadação irá fazer com que os proprietários passem esse valor extra para os inquilinos e então dentro de 5 anos você verá uma alta exponencial em todo o mercado de aluguéis. Todos os países que fizeram algo parecido tiveram um efeito adverso.

Aí fica fácil né camarada. O locatário usa o imóvel integralmente e tem que pagar o IPTU?? Vou vender todas as minhas casas e ir morar de aluguel com IPTU por conta do proprietário. Aí fica fácil!!!!!

Acertada é o ****. Chega de imposto. Esta configurado que o erário que tirar tudo q é nosso. Daqui a pouco vamos pagar imposto até para se enterrar, pelo fogão e geladeira todo ano. País de **** e de administradores **** que pensam igual vc seu ****.

Esse governo de **** e ditadores precisa ser parado

Você é inquilino ou proprietário, Ronaldo?