Portuguese

Portuguese  English

English  Spanish

Spanish

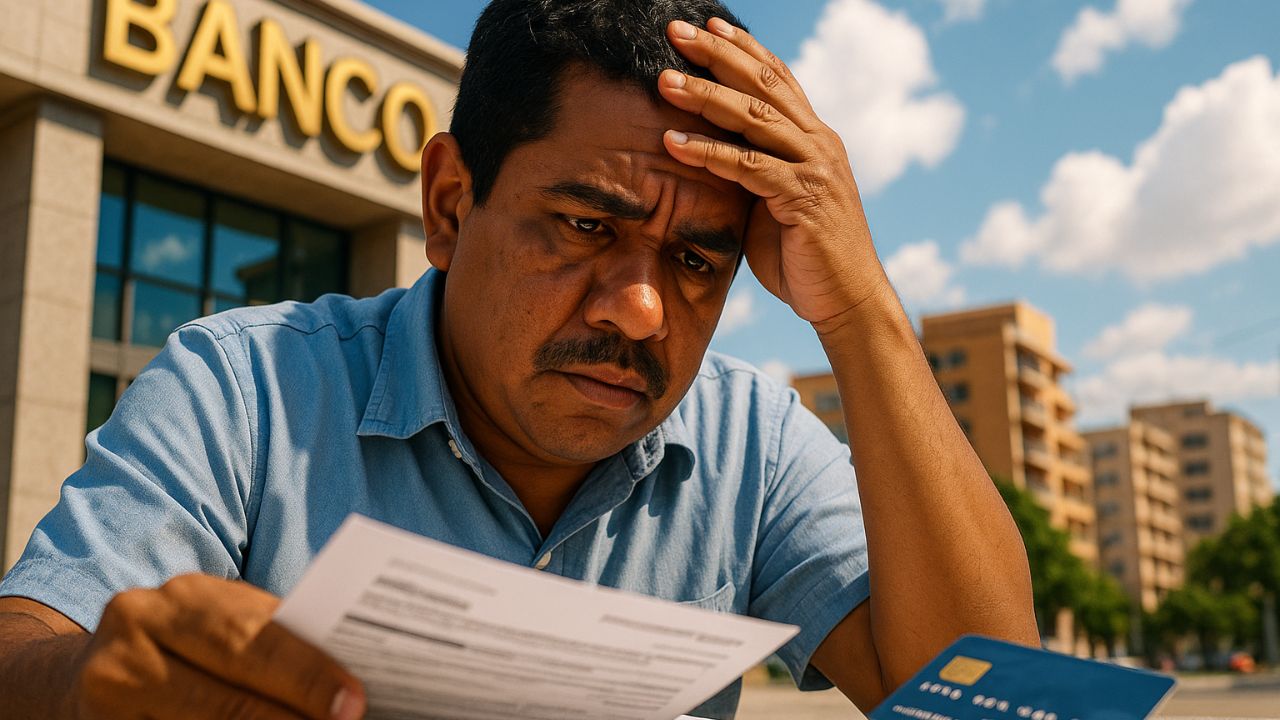

Lawyer Explains What Happens If You Stop Paying Bank Debts, The Risk of Lawsuits, Account Freezing, Statute of Limitations, and Discounts When Negotiating.

If you are thinking about stopping paying bank debts, you probably have already reached that point where the numbers no longer add up. Overdrawn credit card, overdraft, payroll loan, personal loan, and suddenly it seems that the only way out is simply to stop paying and see what happens next.

As a lawyer, I can tell you one thing clearly: stopping paying bank debts is not the end of the world, but it is also not a step you can take blindly. There are legal, financial, and practical consequences that need to be understood carefully. At the same time, it is precisely this scenario of default that makes many banks accept renegotiations with discounts of up to 95 percent to settle everything at once.

Next, I will directly explain what really happens when you decide to stop paying, what the real risks are, how lawsuits work, account freezes, the statute of limitations on debts, and why there is so much flexibility when it comes to agreements.

-

The institute that trained the greatest aerospace engineers in Brazil has just opened its first campus outside São Paulo after 75 years: ITA Ceará will have R$ 445 million, new courses in energy and systems, and classes are expected to start in 2027.

-

Luciano Hang, owner of Havan, goes to Juiz de Fora after the tragedy in February, brings R$ 1 million, hands out R$ 2,000 cards, and donates up to R$ 15,000 to victims in the region.

-

The Brazilian passport allows legal residence in dozens of countries without the need for a prior visa, and most Brazilians are unaware that they can apply for residency directly upon arriving in nations in South America, Africa, and even Europe.

-

Petrobras sends a message to Brazilian truck drivers after fuel collapse and reveals plan to have 100% domestic diesel.

What It Means, Practically, to Stop Paying Bank Debts

When someone talks about stopping paying bank debts, they are not pressing a reset button. What happens is a predictable sequence of steps, roughly in this order:

Delinquency of payments and the incidence of interest and penalties, administrative collection by the bank itself, transfer of the debt to the collection department or third-party companies, inclusion of the name in default registries, and possible filing of a collection lawsuit or execution.

In other words, stopping paying bank debts does not make the debt disappear; it only changes how the bank will try to collect. Instead of collecting the total amount in installments, it starts seeking the money through other means, including judicial ones.

First Consequences: Interest, Penalties, and Bad Credit

Right from the first days of delinquency, contractual charges come into play:

Late payment interest

Penalty for delay

Default charges provided for in the contract

The amount starts to grow, sometimes at an alarming rate. Following that, comes the negative listing:

Inclusion of your Social Security Number in Serasa, SPC, and other registries

Difficulty in obtaining new credit, financing, and credit cards

Restrictions for renting, real estate financing, and even some job hires

The first impact of stopping paying bank debts is to kill your credit power for a good time, which can be strategic in some cases, but must be understood as a real cost of that decision.

From Friendly Collection to Judicial Process

After some time of delinquency, the bank changes its approach. First comes persistent collection:

Phone calls, messages, emails, collection letters

Renegotiation proposals with long installments and high interest

Transfer to specialized collection companies

In a second moment, there is the possibility of the bank filing a lawsuit. Depending on the type of debt and the documentation it possesses, this may happen through:

Collection action

Monitory action

Execution of the title when there is strong and liquid documentation

Here’s an important point: stopping paying bank debts opens up space for negotiation, but it also opens up space for judicial processes, and the bank chooses the path it deems most efficient for itself.

Account Freezing and Seizure of Assets: How Far Can the Bank Go?

If the bank wins a judicial action or already enters with a well-documented executive title, it can request harsher measures, such as:

Freezing amounts in bank accounts via electronic systems

Searching for vehicles in your name

Attempting to seize assets, such as cars or real estate, respecting legal protections

In some specific cases, freezing part of earnings when permitted by law and the judge

There is a general rule in the legal system that protects:

Salary

Pension

Social security benefits

These amounts are usually exempt from seizure, except for specific exceptions analyzed on a case-by-case basis. Therefore, it is not true that by stopping paying bank debts the bank automatically “takes everything”, but it is also not true that nothing can be reached. Free and available assets can indeed be affected by judicial decision.

Statute of Limitations: When the Debt Becomes Uncollectable

One of the topics that generates the most confusion is the statute of limitations. In simple terms, the statute of limitations is the period the creditor has to legally collect a debt. Once this period has passed, they lose the right to demand payment through legal means.

In many bank debts, the statute of limitations is a few years from the due date, varying according to the type of contract. After that:

- The debt does not disappear, but becomes a natural obligation

- The creditor loses the ability to take you to court for collection

- They can still offer agreements and internally register the debt, but with limitations

Another important point is the negative listing. The default registries usually maintain the recording for a maximum period counted from the due date. After that, the name is removed from the registry, even if the debt has not been paid.

In other words, stopping paying bank debts can lead to the statute of limitations and the removal of the name from credit agencies, but this takes time and does not prevent collection attempts along the way.

Why Banks Offer Discounts of Up to 95 Percent

If you have ever received an offer to settle a debt with a huge discount, you are not alone. It is common to see banks offering discounts of 80 to 95 percent in settlement campaigns, especially for very old contracts or those already fully provisioned as losses.

Why does this happen:

- Over time, the chance of recovering the full amount falls significantly

- The institution has already accounted for that debt as a loss

- Any amount received in the settlement represents an “extra” for the bank

- It is better to receive a little in cash than to maintain an old debt that is unlikely to be paid

In practice, stopping paying bank debts and remaining in default for a long time is precisely what creates the scenario for large discounts. The creditor realizes that:

- You are no longer in a position to pay the full amount

- The judicial route can be costly and time-consuming

- An agreement with a large discount is the most efficient way to recover something

Of course, this does not mean you should simply stop paying everything. It means that, in some cases, default ends up being the trigger for negotiations that are much more advantageous than those offered when the debt is still “up to date”.

When It Makes Sense to Negotiate and When to Seek Legal Help

Given this scenario, the question is not just whether you should stop paying bank debts, but:

- At what point did the debt become unmanageable

- Whether the interest has made the contract abusive

- Whether there is already legal action against you

- Whether there is real risk to important assets of your family

In many cases, it is worth:

- Analyzing each contract

- Checking for abusive clauses

- Calculating what the original debt is and how much has turned into just charges and interest

- Using default as a negotiation tool, but strategically

Having legal guidance makes a big difference, especially when there is already a lawsuit, risk of freezing, or doubt about the statute of limitations. A good diagnosis prevents impulsive decisions, whether to stop everything or accept the first offer made.

In the end, stopping paying bank debts is a serious decision that can open space for both problems and negotiation opportunities, depending on how you conduct the next steps.

And you, have you thought about stopping paying bank debts or have you received a very high discount proposal from the bank to settle everything? Share in the comments what was the biggest doubt or fear that came up in that situation.

Estou a um pouco mas dé um ano sem pagar o Cartão de crédito dá Caixa não aceitei o acordo dele pois não tinha como conprilo além que dobrou a dívida isso está me tirando o Sono com muitas ameaças com nome no Serasa,tenho 73 anos tou quaze tendo um infarto pelas ameaças!

Eu estou desempregada, doente com transtorno de retardo mental mistos e estava passando fome e fiz uma portabilidade do meu banco para outro banco, e agora eles estão me bloqueando o CPF eu não tenho dinheiro para comprar meus medicamento e não estou conseguindo receber no programa do governo federal, sendo que minha aposentadoria é de um salário mínimo e o Bradesco ficava com todo meu dinheiro, eu não recebia nenhum centavo e ainda tenho um filho especial.

Esse mês tomei uma decisão, não pago mais nada, só o básico…E vou descansar e viver…Ou morro de fome e da falta do básico como Luz, água, e outros. Um dia acerto tudo à vista. Parcelar é bobagem . Só piora a situação.