Portuguese

Portuguese  English

English  Spanish

Spanish

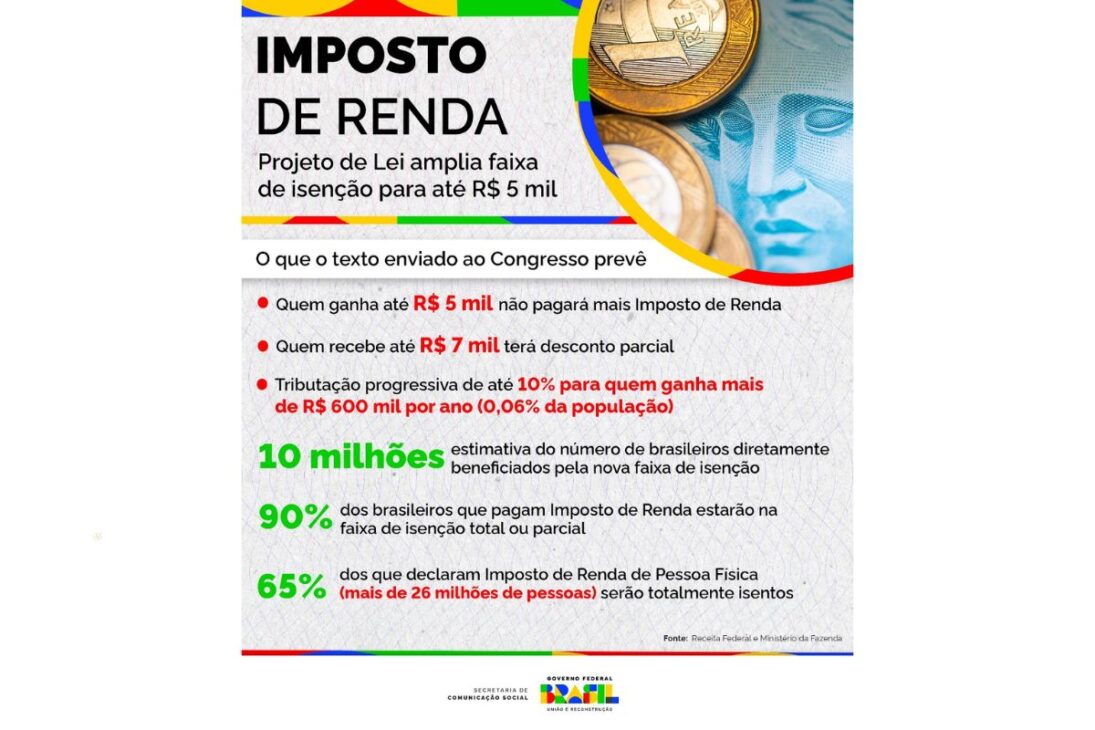

Treasury Direct Achieves Historic Real Interest Rate of 8% Above Inflation, Reflecting Increased Fiscal Distrust, the Impact of New Income Tax Exemptions, and Investor Alerts About the Cost of Financing the Brazilian Government

Treasury Direct has reached a record of 8% per year above inflation, an unprecedented level that sparks both excitement and concern. For long-term investors, this is a rare opportunity to secure a real yield well above the historical average, which hovers around 4.5% per year. For the government, however, it is a warning sign: the more expensive it becomes to raise resources, the greater the market’s distrust regarding public accounts.

According to William Ribeiro, the main reason for this surge is the growing fiscal risk. With the approval of the income tax exemption for those earning up to R$ 5,000 monthly, the government has relinquished a portion of its revenue. Without equivalent cuts in spending and with uncertainties about compensations, the market has reacted by demanding higher interest rates. In simple terms, the greater the perceived risk, the higher the premium required to finance the State.

Why the Government Is Paying So Much

The measure that expanded the income tax exemption brought relief to the middle class, but it also created a significant fiscal cost.

-

Oil surged to $115 a barrel due to the war in the Middle East, and diesel in Brazil has already risen to R$ 7.45 per liter, while the United States…

-

Brazilian city bets on the business environment to generate jobs and attract investments in the energy sector — secretary reveals strategy at Macaé Energy 2026.

-

50 viaducts, 4 tunnels, 28 bridges, and 40 kilometers of bike paths: BR-262 in Espírito Santo will receive 8.6 billion reais for the largest engineering project in the state’s history, inspired by the Immigrant Highway in São Paulo.

-

Brazil produces too much clean energy and doesn’t know what to do with it: over 20% of solar and wind capacity was wasted in 2025 while investors flee and 509 renewable generation projects were abandoned in the last year.

Estimates point to renunciations between R$ 25 billion and R$ 45 billion per year. Without a credible compensation plan, this revenue loss creates uncertainty about the balance of public accounts.

States and municipalities also lose revenue, increasing the pressure on the consolidated result.

In light of this, investors have begun to demand higher interest rates to buy government bonds, which has pushed Treasury IPCA+ rates to historic levels.

This movement mirrors the pattern of previous periods of fiscal tension, such as 2016 and 2022, when increased public spending and political instability caused long-term rates to soar.

What the Investor Needs to Understand Before Buying

Despite the appeal of the rate, Treasury Direct is not an investment for impulsive decisions. The 8% rate above inflation applies only to those who hold the bond until maturity.

If the investor decides to sell early, the price may fluctuate due to what is called market marking. When rates rise, bonds lose value; when they fall, they appreciate.

This means that the same bond can generate early profit or loss, depending on the timing of the sale.

For those seeking safety and real profitability in the long term, Treasury IPCA+ remains one of the best options available.

However, it is essential to respect the maturity period and have an emergency reserve outside of it, as liquidity and stability do not go hand in hand in this type of investment.

The Fiscal Risk and Confidence in the Government

The record real interest rate is not a symptom of prosperity, but rather of distrust.

The government collects over R$ 3 trillion per year, but remains unable to balance revenues and expenses.

The perception that public spending will continue to rise makes investors demand more return to take on Brazil risk. This makes credit more expensive, reduces private investment, and puts pressure on public debt.

The National Treasury, therefore, pays dearly to raise funds because the market sees the country as overspending and under-planning.

Without fiscal credibility, even well-intentioned policies end up costing more. The high interest rate is, ultimately, the price of budgetary disorganization.

Historic Opportunity or Disguised Trap

Locking in IPCA + 8% per year is a rare opportunity, but the high premium comes with a warning sign.

For those with a long horizon and a disciplined profile, this rate can ensure solid real income for decades.

However, for those who need liquidity or tend to react to volatility, the risk of loss is high. The key is to understand that profitability and stability never walk hand in hand.

The moment is strategic for those looking to consolidate retirement reserves, educational funds, or long-term assets.

But the success of this choice depends on the country’s fiscal behavior in the coming years. If the government can control spending and generate confidence, the bonds will appreciate.

If it fails, market marking could penalize those who do not know how to wait.

The Treasury Direct is experiencing one of the most paradoxical moments in its history. It pays the highest real interest rate ever, but it does so because the market doubts the country’s fiscal health.

For the informed investor, it is a time for calm and strategy: to take advantage of the premium without ignoring the context.

What may currently seem an opportunity may become a trap if Brazil does not adjust its accounts and regain credibility.

And you, will you take advantage of this IPCA + 8% from Treasury Direct or prefer to wait for more fiscal clarity? Do you think the risk compensates the return? Leave your opinion in the comments and share how you are handling this decision in practice.

Seja o primeiro a reagir!