Portuguese

Portuguese  English

English  Spanish

Spanish

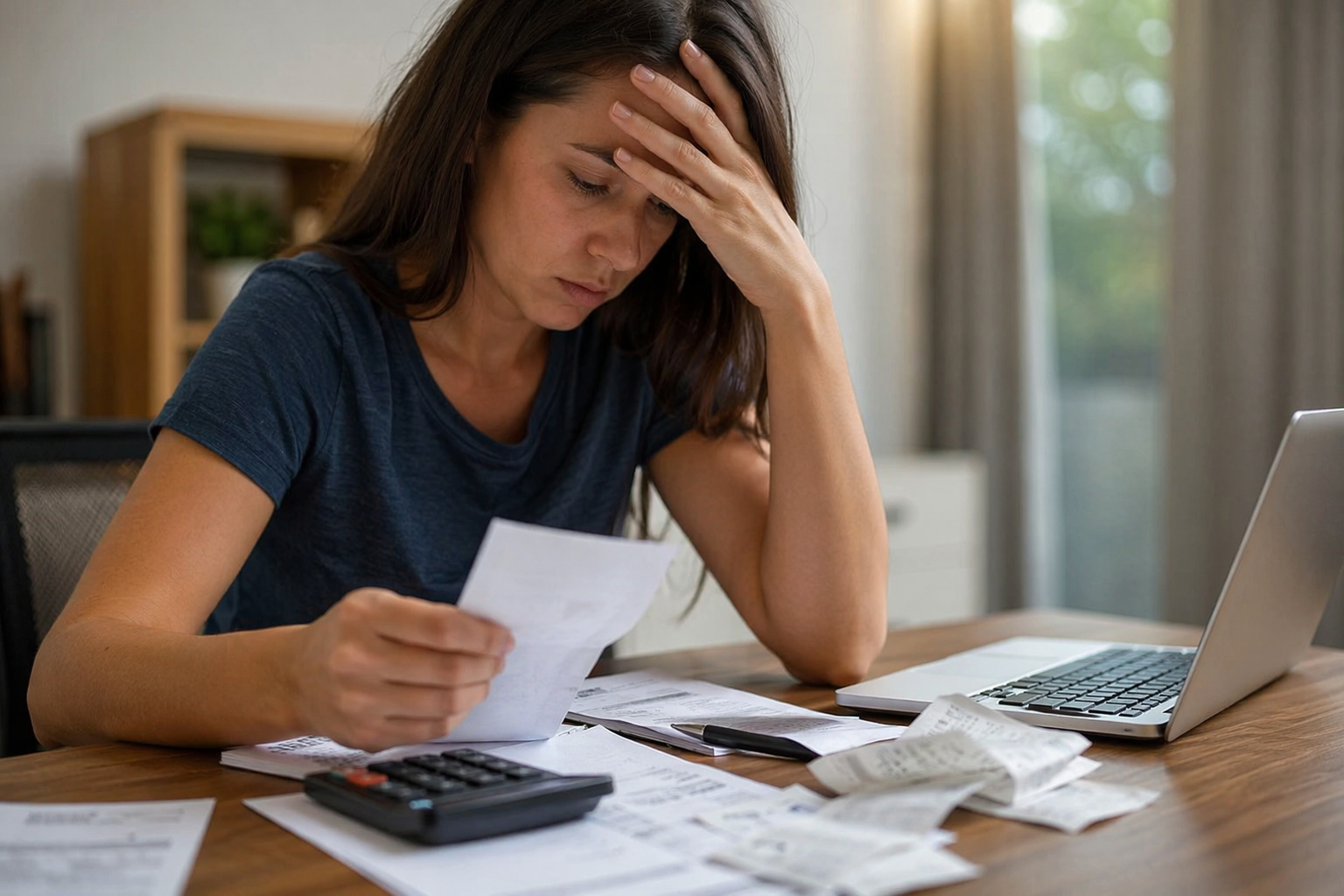

The Desenrola 2.0 program from the federal government offers discounts of up to 90% on the debts of indebted families, aims to block access to new lines of credit with abusive interest rates like the credit card revolving debt that reaches 435.9% per year and is expected to be implemented by provisional measure in 2026.

Millions of Brazilians struggling with uncontrollable debts may have a real chance to start over. The federal government announced the return of the Desenrola program in a 2.0 version that goes beyond renegotiation: in addition to offering discounts of up to 90% on debts, the project proposes to block beneficiaries’ access to new lines of credit with abusive rates, creating a mechanism that seeks to prevent families from falling back into debt after clearing their names. The program is in the final stages of preparation and is expected to be implemented by provisional measure in 2026.

The government’s strategy tackles the debt problem on two simultaneous fronts. The first is the renegotiation with discounts that can reach 90% of the total debt amount, with financial institutions receiving government support that uses public funds as collateral. The second is the limitation of access to credit card revolving debt, which reaches the astronomical rate of 435.9% per year and is one of the main traps that push families back into debt. Desenrola 2.0 aims to address not only existing debts but also to prevent new ones from accumulating.

How the discount of up to 90% on debts from the Desenrola 2.0 program works

Renegotiation is the central pillar of the program. Participating financial institutions will be able to count on public funds as collateral in negotiations, which reduces the risk for banks and creditors and allows them to offer much more favorable conditions than those available in the normal renegotiation market.

-

In addition to the war with Iran, a strong El Niño could tighten inflation in Brazil in 2026: higher energy costs, risks to food, and warnings about red flags put the government on high alert already.

-

Those with debt in their name will be on alert in 2026: Central Bank reveals indebtedness of 49.7% of income and increasing pressure from high inflation and interest rates.

-

Emirates pays R$ 34,850.71 per landing of the A380 in Guarulhos, a fee calculated by maximum weight; a video shows ANAC’s rates, compares Campinas, and reveals: Recife would be even more expensive for international flights today, which is alarming.

-

Neither the USA nor China: two countries in Latin America could enter the top 10 largest economies in the world by 2030 and concern traditional powers.

In practice, this means that a person with debts of R$ 10,000 could settle them by paying only R$ 1,000, depending on the debt profile and the specific conditions of each institution.

The generous discounts on debts combined with reduced interest rates are expected to transform the financial reality of families who today cannot even pay the minimum on their credit cards. The program is aimed at indebted families who have lost the ability to meet their commitments and who, without intervention, would remain with a negative credit record for years.

The goal is to return these people to the consumer market and the banking system in a healthy way, without renegotiation becoming just a postponement of the problem.

The block against new debts that differentiates Desenrola 2.0 from the original program

The major novelty of Desenrola 2.0 compared to the previous version is the preventive approach. The program does not limit itself to renegotiating existing debts: it proposes to restrict beneficiaries’ access to new loans under onerous conditions, especially to credit card revolving debt, whose rate of 435.9% per year is one of the highest in the world.

The logic is simple: it is of no use to clear a family’s debts if, months later, they fall back into debt under the same conditions that led them to the problem.

This block against new debts is accompanied by commitments that include financial education responsibilities. Program beneficiaries take on the responsibility to participate in activities that help them understand how credit works, how to plan the family budget, and how to avoid the traps that fuel the cycle of indebtedness.

It is a significant change in approach: instead of just putting out the fire of debts, Desenrola 2.0 tries to prevent it from recurring.

Why the credit card revolving debt is the villain of Brazilian debts

The credit card revolving debt is by far the most expensive credit option available to Brazilian consumers. With an interest rate of 435.9% per year, it turns a R$ 500 purchase into a snowball that can exceed R$ 2,000 in a few months if the consumer pays only the minimum amount on the bill.

It is a mechanism that attracts families in temporary difficulty and traps them in a cycle of self-feeding interest.

Desenrola 2.0 directly targets this problem by proposing limitations on access to revolving credit for those who join the program. The idea is that families who have just renegotiated their debts with discounts of up to 90% do not have immediate access to a line of credit that charges almost 5 times the amount borrowed in annual interest.

For banks, the restriction may mean less revenue from interest in the short term. For families, it means a real chance to keep their finances organized after getting out of the red.

The expected impact of Desenrola 2.0 on the economy of families and the country

The government’s expectation is that the program will have a positive effect not only on family finances but on the national economy as a whole. Families that clear their debts return to consuming, stimulate local commerce, and reactivate productive chains that depend on domestic consumption.

Chronic indebtedness removes millions of people from the consumer market and reduces tax revenue, creating a negative cycle that affects everyone from small merchants to public coffers.

With the Desenrola 2.0 proposal about to become reality through provisional measure, attention now turns to the details of implementation. How many financial institutions will join, what types of debts will be eligible, how the block against new loans will work in practice, and what criteria will define who can participate are questions that still depend on the official publication of the text.

What is already clear is that the program targets a problem affecting tens of millions of Brazilians and that this time the approach includes prevention, not just remedy.

What to expect from Desenrola 2.0 and who can benefit

The program is in the final stages of preparation and is expected to be published as a provisional measure, allowing for immediate implementation. The target audience is indebted families who cannot renegotiate their debts under accessible conditions in the conventional market, especially those trapped in credit options with high interest rates.

The discount of up to 90% on debts, combined with the restriction on new indebtedness and commitments to financial education, forms a package that attempts to address the problem structurally.

If Desenrola 2.0 works as planned, millions of Brazilians will be able to restart their financial lives with a clean slate and with tools to avoid repeating the same mistakes. But renegotiation programs depend on adherence, oversight, and political continuity to generate lasting results.

The first Desenrola already demonstrated that the demand exists and that millions of people are willing to resolve their issues when conditions are favorable. Version 2.0 promises to go further. Now it remains to turn the promise into a decree.

Do you have debts that could be renegotiated with a discount of up to 90%? Do you think the block against new loans will work or that people will find another way to get into debt? Share in the comments. This program can affect the lives of millions of families, and the debate needs to include those who need it the most.

Seja o primeiro a reagir!