Portuguese

Portuguese  English

English  Spanish

Spanish

Central Banks Bought 863 Tons Of Gold In 2025. Poland Led, Brazil Returned To The Market And China Maintained Purchases. Understand The Numbers.

In 2025, the global gold market recorded a movement that, despite being little visible outside specialized circles, carries profound implications for the international financial system. Even with the metal traded at record levels throughout the year, central banks continued to accumulate gold on a large scale, ending the period with 863.3 tons of net purchases. The number, consolidated by the World Gold Council (WGC), confirms that the search for physical assets remains a central strategy for diversification and protection in an environment marked by geopolitical tensions, persistent inflation, and monetary uncertainties.

Although lower than the exceptional volumes above 1,000 tons observed in 2022, 2023, and 2024, the 2025 result remains well above the historical average of the previous decade, when annual purchases hovered around 400 to 500 tons. Practically speaking, this represents the consolidation of a new structural level for official demand for gold, rather than a one-off peak.

The Global Numbers That Explain The Turnaround

The data from Gold Demand Trends shows that the fourth quarter of 2025 concentrated around 230 tons of official purchases, indicating that central banks’ appetite did not wane even with the high price of the metal.

-

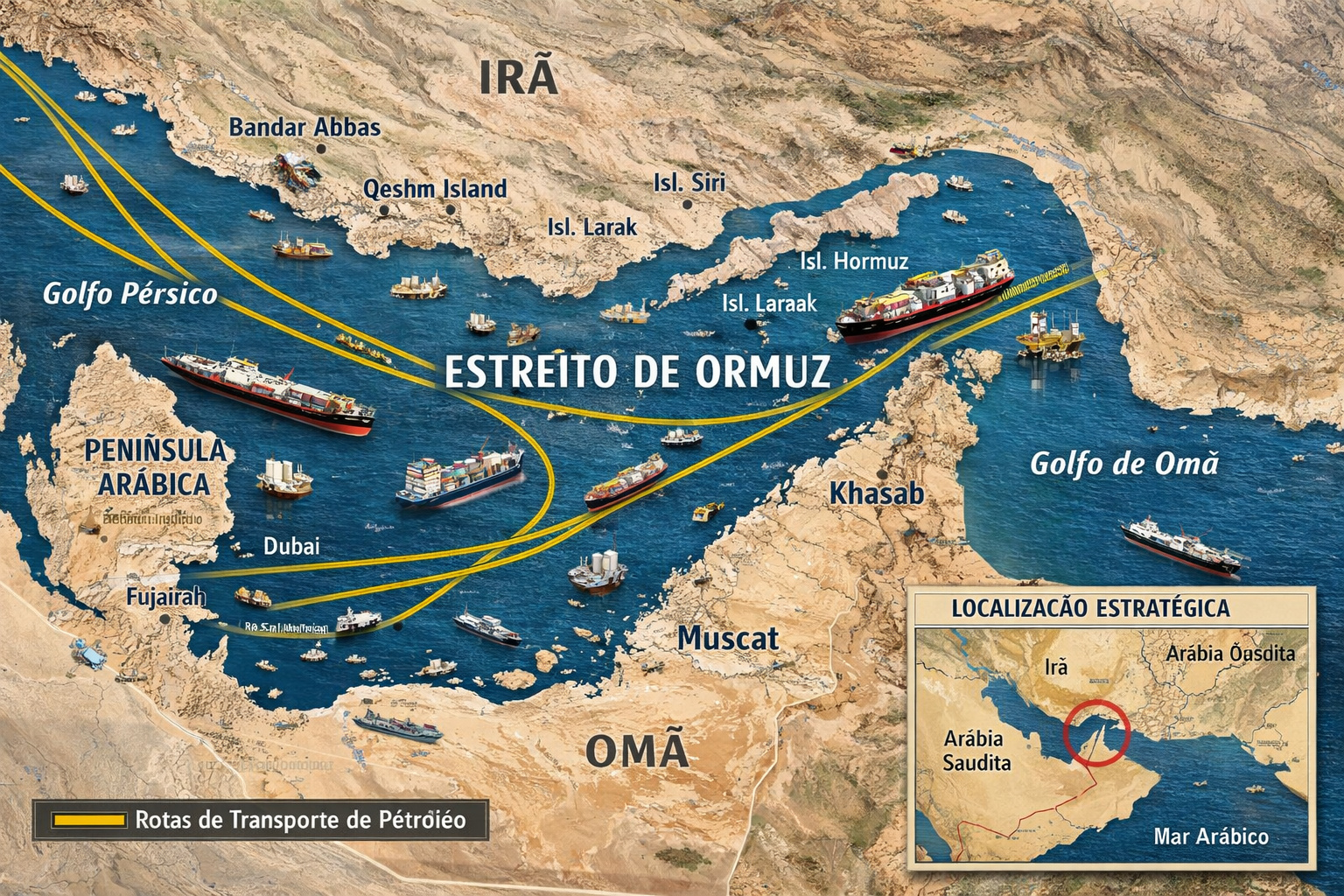

Global summit with over 40 countries pressures Iran for a blockade in the Strait of Hormuz and warns of direct impact on oil, food, and the global economy.

-

Russia has broken the U.S. maritime blockade to send oil to Cuba and is now loading a second ship while Trump says that “Cuba is next” in a possible military action against the island.

-

Spain challenges the USA and closes its airspace for operations against Iran, raising global tension and provoking the threat of a trade rupture.

-

While no other country manufactures tanks in Latin America, Argentina activates the TAM 2C-A2 and raises a curiosity about the technological lag in the region.

Throughout the year, dozens of monetary institutions participated in the movement, but a small group of countries accounted for most of the volume acquired.

This behavior confirms a shift that has been unfolding since 2022: gold has returned to play a central role in the composition of international reserves, not as a speculative alternative, but as a tool for reducing systemic risk.

The entity itself highlights that the level of purchases observed since 2022 represents the highest since the end of the gold standard and the Cold War.

Poland Leads And Transforms Gold Into National Security Policy

The most emblematic case of 2025 was Poland. The country’s central bank added 102 tons to its reserves throughout the year, becoming the largest official buyer in the world during this period.

As a result, the total amount of gold held by the country approached 550 tons, raising the metal’s share to about 28% of international reserves.

More relevant than the absolute number was the institutional discourse that accompanied the movement. Authorities from the Polish central bank publicly declared their intention to further increase the gold stock, with long-term goals that could bring the country to levels nearing 700 tons, explicitly associating the metal with national economic and financial security.

This type of positioning indicates that, for some European countries, gold has been re-envisioned as a strategic pillar in the face of a regional and global instability scenario.

Brazil Returns To The Market And Reinforces Reserve Diversification

Another highlight of 2025 was Brazil’s return to official gold purchases. After a period without significant acquisitions since 2021, the Brazilian Central Bank returned to the market between September and November, accumulating around 43 tons in just three months. Consequently, national reserves rose to approximately 172 tons.

Despite the significant volume in a short period, gold still represents a relatively modest share of Brazil’s reserves, estimated at about 7%.

This indicates that the movement does not signal a radical change in monetary policy, but rather a strategic adjustment aimed at diversifying assets and reducing exclusive dependence on fiat currencies and foreign sovereign bonds.

China, Turkey And The Continuity Of The Asian Movement

China maintained its gradual purchasing strategy in 2025. According to official data compiled by the WGC, the country added around 27 tons throughout the year, bringing its total reserves to just over 2,300 tons.

Although the pace has been more moderate than in previous years, the continuity of acquisitions reinforces the long-term view: gold remains a structural component of Chinese reserve policy.

Turkey also figured among the relevant buyers, even amid internal macroeconomic challenges. The Turkish central bank continued to use gold as a stabilization tool and protection against currency volatility, maintaining the country among the major official accumulators of the metal.

Expensive Gold, But Still Strategic

One of the key points to understand 2025 is the relationship between price and institutional behavior. Gold spent much of the year hitting historical highs, which naturally imposed caution on central banks.

The World Gold Council itself observes that the pace of purchases was partially tempered by the metal’s appreciation, as rising prices automatically increase the value of existing reserves.

Nevertheless, the fact that acquisitions remained elevated indicates that central banks do not view gold merely as a price opportunity, but as strategic insurance.

Unlike private investors, these institutions do not seek short-term returns, but stability, liquidity in extreme crises, and protection against systemic risks, including financial sanctions and monetary shocks.

Relationship With The Dollar And The International Monetary System

The increase in gold’s share in global reserves does not necessarily mean the abandonment of the dollar or other strong currencies. What the data show is a gradual rebalancing, in which physical assets regain lost ground over the past decades.

According to analyses from the WGC itself and agencies like Reuters, the share of gold in international reserves is moving towards levels observed in the early 1990s, a period marked by relevant geopolitical and monetary transitions.

In this context, gold functions as a neutral asset, without a sovereign issuer, globally accepted and with a history of value preservation in crisis scenarios. For emerging countries and economies exposed to external risks, this characteristic has become particularly appealing after 2022.

Comparison With Previous Accumulation Cycles

Historically, large cycles of gold purchases by central banks tend to coincide with moments of rupture or reconfiguration of the international system. The pattern observed since 2022, and confirmed in 2025, presents parallels with periods such as the post-oil crisis in the 1970s and the transition from the end of the Cold War.

The current difference lies in the global simultaneity of the movement. Instead of isolated decisions, there is a broad set of countries from different regions reinforcing stocks in a coordinated manner, even if not formally articulated. This pattern suggests that exclusive reliance on fiat currencies has come to be seen as a concentrated risk.

What To Observe From 2026 Onward

Data from 2025 consolidates a trend, but does not close the debate. For the coming years, analysts will be monitoring three main factors: the continuity of official purchases at elevated levels, the public discourse of central banks regarding the role of gold, and the relationship between new geopolitical crises and the acceleration of acquisitions.

If the behavior observed since 2022 continues, gold is likely to remain one of the main strategic assets in the international financial system, alongside strong currencies and increasingly, critical physical resources.

Gold As A Link Between Financial Reserves And Real Power

Observing the movement of central banks in 2025, it becomes clear that gold has returned to occupy a space that goes beyond financial accounting. It is directly connected to the broader debate on economic sovereignty, national security, and control of real assets.

Just as critical minerals have begun to be treated as instruments of industrial and geopolitical power, gold reassumes its historical role as the silent anchor of trust among states.

The year 2025 did not mark the beginning of this change, but confirmed that it is already underway.

-

-

2 pessoas reagiram a isso.