Portuguese

Portuguese  English

English  Spanish

Spanish

Country Faces Unprecedented Twin Deficits in Magnitude, with Rising Debt and Selic at 15% Per Year, According to Jornal de Brasília.

The Brazil entered 2025 in an uncomfortable position among the largest economies in the world. The country combines a gross public debt of 77.5% of GDP with the highest basic interest rate in the world, currently at 15% per year. This equation puts pressure on public finances, expands the so-called twin deficits, and reinforces the perception of structural fragility of the national economy.

Experts consulted by Jornal de Brasília explain that the twin deficits, fiscal and external, occur when the government spends more than it collects while the country has a negative balance in its accounts with the outside world.

This combination places Brazil on a worrying path of persistent imbalances, as the high cost of debt limits investment capacity and reduces competitiveness compared to other emerging economies.

-

The Federal Revenue Service now automatically cross-references everything you declare with data from banks, credit cards, brokerage firms, and insurance companies, and any discrepancy between your income and your expenses triggers an alert in seconds.

-

Amid global tensions, Brazil blocks the United States’ proposal at the WTO and paves the way for a trade crisis and possible retaliations.

-

Shopee opens the largest logistics warehouse in Brazil in Guarulhos: 220,000 m² on Dutra, contract signed before construction, pays R$ 45/m² and accelerates deliveries at scale, putting pressure on Mercado Livre and Amazon.

-

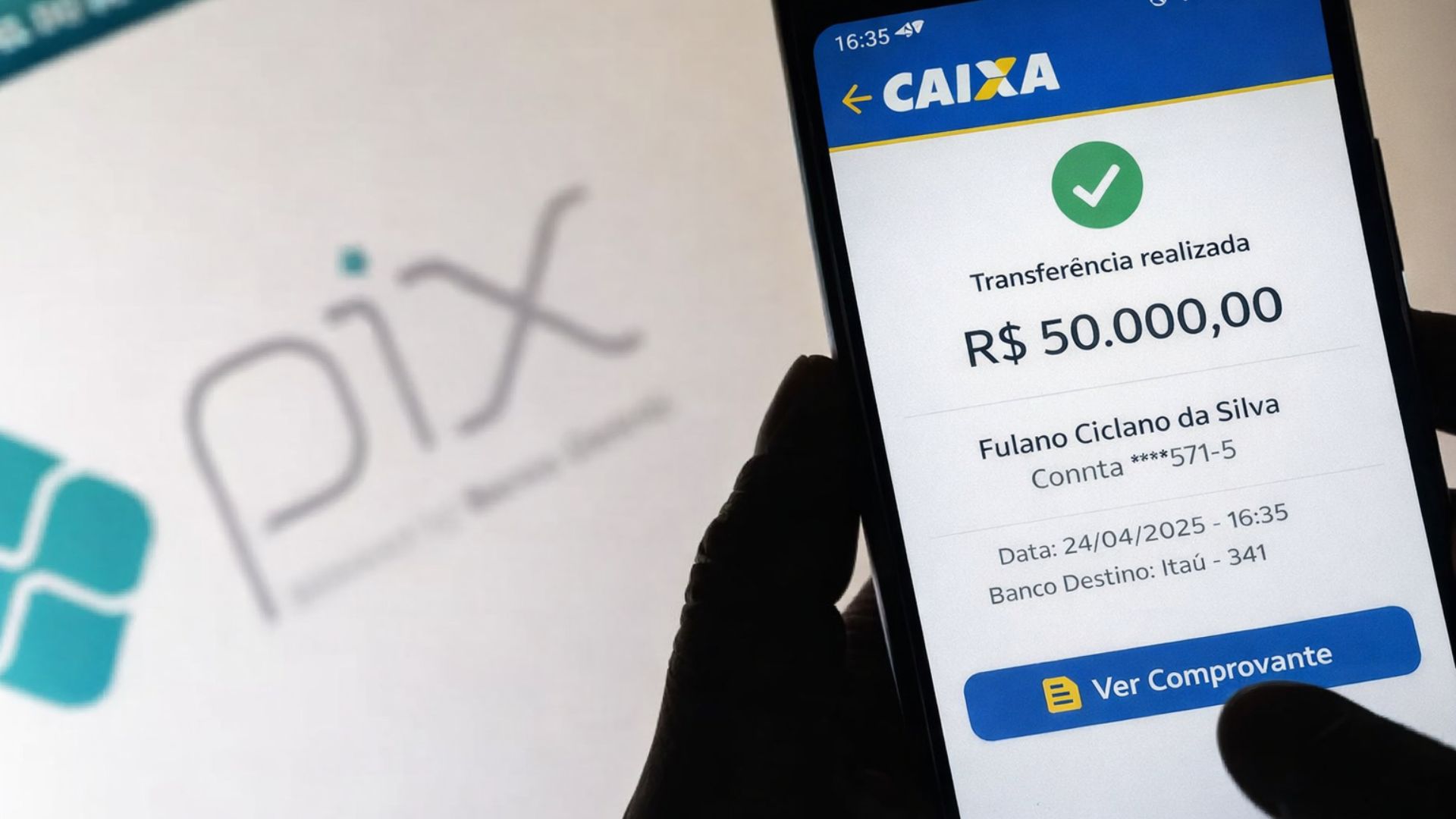

After mistakenly transferring R$ 50,000 via Pix, a man will receive the amount back along with R$ 10,000 for moral damages from the recipient.

The Weight of Interest on Public Debt

Interest expenses have been the main driver of the rise in gross debt. In the 12 months ending in July 2025, the government disbursed nearly R$ 1 trillion just in interest payments, which drove the nominal deficit to 7.12% of GDP.

When adding the Union, states, and municipalities, the projection reaches 8.5% of GDP, with 8 percentage points derived exclusively from the cost of debt rollover.

This scenario fosters a vicious cycle: the government pays more to finance itself, which increases the debt, which in turn requires even higher interest rates to attract buyers of public bonds.

The result is a growing indebtedness, which jumped six percentage points in just over two and a half years.

The Deterioration of the External Sector

In addition to fiscal fragility, the current account deficit rose from 1.4% to 3.5% of GDP in just 12 months.

The worsening is explained by the slowdown in exports, which grew less than imports, and the increase in remittances of profits, dividends, and services sent abroad.

Although the external deficit is still covered by incoming foreign direct investment, analysts warn that the trend is unsustainable without internal adjustment.

The loss of competitiveness in the trade balance exposes the economy to exchange rate shocks and increases dependence on external capital.

Strangulation of Investment and Crowding-Out Effect

The weight of debt and high interest rates also reduces space for public and private investment. Public investment, which once represented 5% of GDP, is now less than 2%, despite the high tax burden, around 34% of GDP.

According to former Central Bank President Arminio Fraga, this phenomenon generates the so-called “crowding out”, when the private sector reduces investments because it competes with the government for credit.

This helps explain why Brazil’s total investment rate remains at only 17% of GDP, while Asian countries invest over 30%.

The Structural Challenge Until 2027

According to analyses by economists such as Samuel Pessôa (Ibre-FGV) and Marcus Pestana (Independent Fiscal Institution), the main Brazilian problem lies not only in the external deficit but in the inability to generate consistent primary surpluses.

Without this, the path of debt will continue to rise, even with gradual cuts in Selic expected in the coming quarters.

Projections indicate that the imbalance is likely to persist until at least 2027, when a more robust solution will be needed to contain the rise in debt and reduce dependence on high interest rates.

Until then, Brazil will continue to be observed as a warning case among major economies, especially because, despite being a leader in oil production in Latin America, it cannot convert this wealth into fiscal and external balance.

The Brazil now faces a scenario of high indebtedness, record interest rates, and twin deficits that places it in a negative spotlight in the global landscape. Although the country still manages to attract foreign investments, the sustainability of this strategy is uncertain.

And you, do you believe that Brazil will be able to reverse this cycle of indebtedness and high interest rates in the coming years, or is the trend towards worsening economic vulnerability?

Leave your opinion in the comments; your perspective is essential for this debate.

Com este governo de esquerda altamente **** e gastador vai ao colapso com certeza e se entrar um presidente serio ifependente do partido precisara de no minimo 2 mandatos para amenizar os estragos deste governo igual na Argentina.

Click pelegos & gás… Se reaprarem, a página está cheia de propaganda da Star link, do Elon Munsk… Click pateiotario & gas

Caracas e não é da Venezuela, tenho 2 grau e consigo enxergar que estes especialistas só mentem, o Brasil é um dos países mais procurados para investimentos por outros países , Ibovespa bate recorde em cima de recorde e ainda vem com essa de fragilidade, o que acontece no nosso país é briga ideológica, aqueles que estão no poder brigam entre si para ferrar o povo , eu prefiro esse governo **** como qualquer outro , mas pauta temas que favorece a maior parte da população!!