Português

Português  Inglês

Inglês  Espanhol

Espanhol

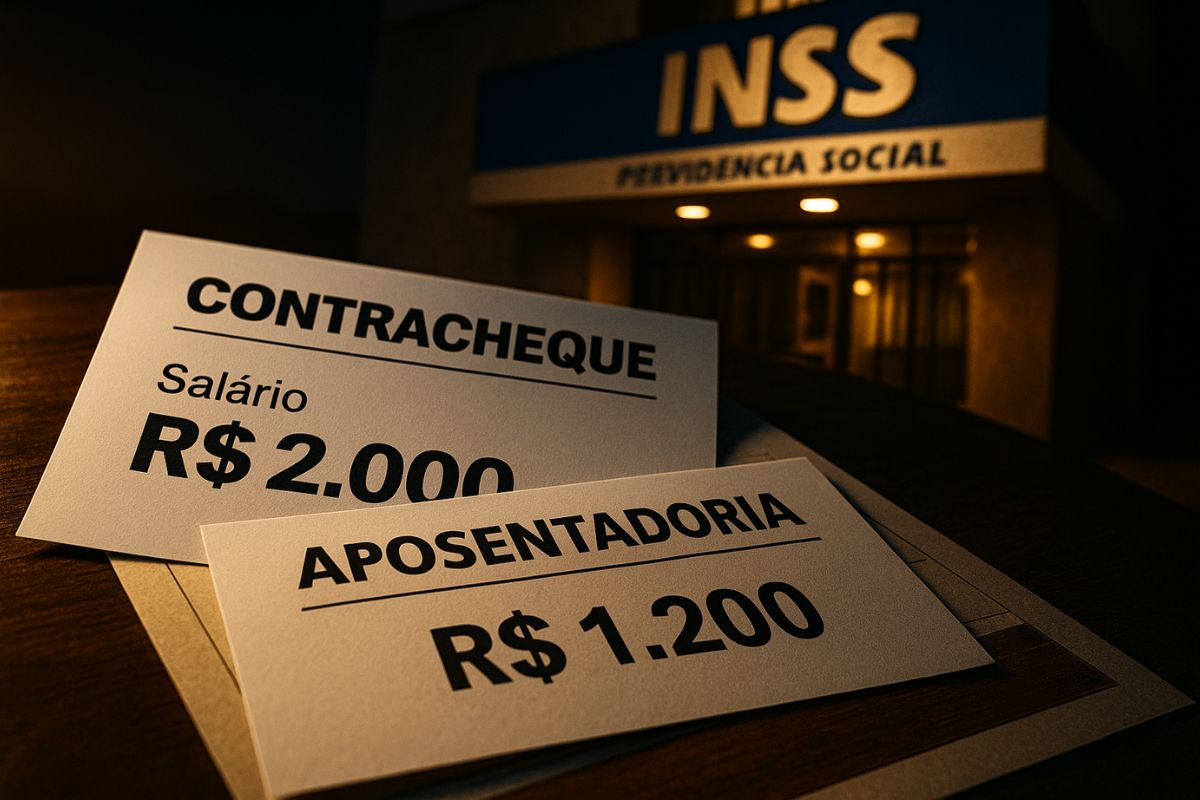

Retirement Calculation Does Not Mirror Current Salary: The INSS Considers the Average of All Salaries Since July 1994, Which Can Lower the Final Benefit.

Many people believe that, when earning R$ 2,000 per month, the amount they will receive upon retirement will be exactly that. However, as lawyer Edmilson Almeida – Social Security Law explains, this expectation is a common misconception. The INSS does not only rely on the most recent salary, but rather on a historical average that begins in July 1994, when the Real Plan was implemented.

This means that past salaries, often lower, are included in the calculation and reduce the final average. Even contributions of R$ 600, R$ 800, or R$ 1,000 made in the past affect the calculation, lowering the amount you will actually receive upon retiring with an expectation of R$ 2,000.

How the Average Is Calculated

According to the current rule, the INSS considers 100% of contributions made since July 1994, updated by official indices.

-

The Senate approves a bill that criminalizes misogyny, hatred, or aversion towards women, and includes the crime in the Racism Law with a penalty of up to 5 years.

-

Chamber Approves Bill That Allows Pepper Spray for Women Over 16 and Imposes Strict Rules for Purchase, Possession, and Use as Self-Defense

-

Chamber Approves Law to Combat Leucaena, Fast-Growing Plant That Dominates Land and Threatens Native Species in Various Regions of the Country

-

Asset Division: Know What Cannot Be Divided in Case of Divorce

Unlike what many imagine, there is no automatic discard of lower salaries: all are included in the calculation.

In practice, this makes retirement lower than the salary a person receives today.

According to Edmilson Almeida, this is the most critical point:

”It doesn’t matter if you earn R$ 2,000 today. If in the past you contributed with lower amounts, this difference will pull the average down.”

The Coefficient That Further Reduces It

In addition to the average, there is another decisive factor: the coefficient applied to the benefit salary.

In retirement by age, for example, the initial amount is 60% of the average, plus 2% for each year that exceeds 15 years of contributions (women) or 20 years (men).

That is, a male worker with 20 years of contributions and an average of R$ 2,000 would only receive 60% of that amount: R$ 1,200.

Since this amount is below the minimum wage, he would end up receiving the minimum pension amount. Only with more contribution time does the amount increase.

Difference Between Types of Retirement

Not all rules are the same.

In cases of disability retirement due to a work accident, for example, the calculation is more advantageous:

The insured is entitled to 100% of the average. In the transition rules, such as tolls or points, the criteria vary greatly.

Therefore, two workers with the same average of R$ 2,000 may retire with very different amounts, depending on the chosen modality and the total contribution time.

Pension Planning Is Essential

What these examples show is that pension planning is not optional.

Anyone expecting to retire with R$ 2,000 needs to review their contribution history, simulate scenarios, and assess whether it is worthwhile to wait a few more years to increase the final income.

According to Edmilson Almeida, “haste can be expensive.”

Often, delaying the retirement request ensures a significantly higher amount, which will make a difference for the rest of one’s life.

Retirement is not an immediate reflection of the current salary, but rather a historical average combined with specific calculation rules.

Those who believe they will retire with R$ 2,000 simply because that is the value on their paycheck may be negatively surprised.

And you, have you calculated how much you will really receive upon retirement? Do you believe the rules are fair or do you think they should be revised? Share your opinion in the comments — your experience can help others understand this topic better.

Seja o primeiro a reagir!