Portuguese

Portuguese  English

English  Spanish

Spanish

New Credit Line for Housing Renovations Injects R$ 30 Billion Until 2026 with Hidden Subsidy from the Treasury and Greater Public Debt Risk

The new credit line for housing renovations announced by the federal government promises to release up to R$ 30 billion in financing between 2025 and 2026, according to information from Brasil247. The program is designed to primarily assist low-income families, with interest rates of up to 1.5% per month, but has been controversial because the discount offered to beneficiaries represents a hidden subsidy borne by the National Treasury, without formally appearing in the budget.

This form of funding raises concerns among economists and congressional staff, who see a risk of increasing the Brazilian public debt, already above 74% of GDP.

The model also reopens the debate over fiscal transparency, as the real costs do not appear in the official expenditure statements, but rather in the difference between the government’s financing cost and the interest charged to borrowers.

-

The Federal Revenue Service now automatically cross-references everything you declare with data from banks, credit cards, brokerage firms, and insurance companies, and any discrepancy between your income and your expenses triggers an alert in seconds.

-

Amid global tensions, Brazil blocks the United States’ proposal at the WTO and paves the way for a trade crisis and possible retaliations.

-

Shopee opens the largest logistics warehouse in Brazil in Guarulhos: 220,000 m² on Dutra, contract signed before construction, pays R$ 45/m² and accelerates deliveries at scale, putting pressure on Mercado Livre and Amazon.

-

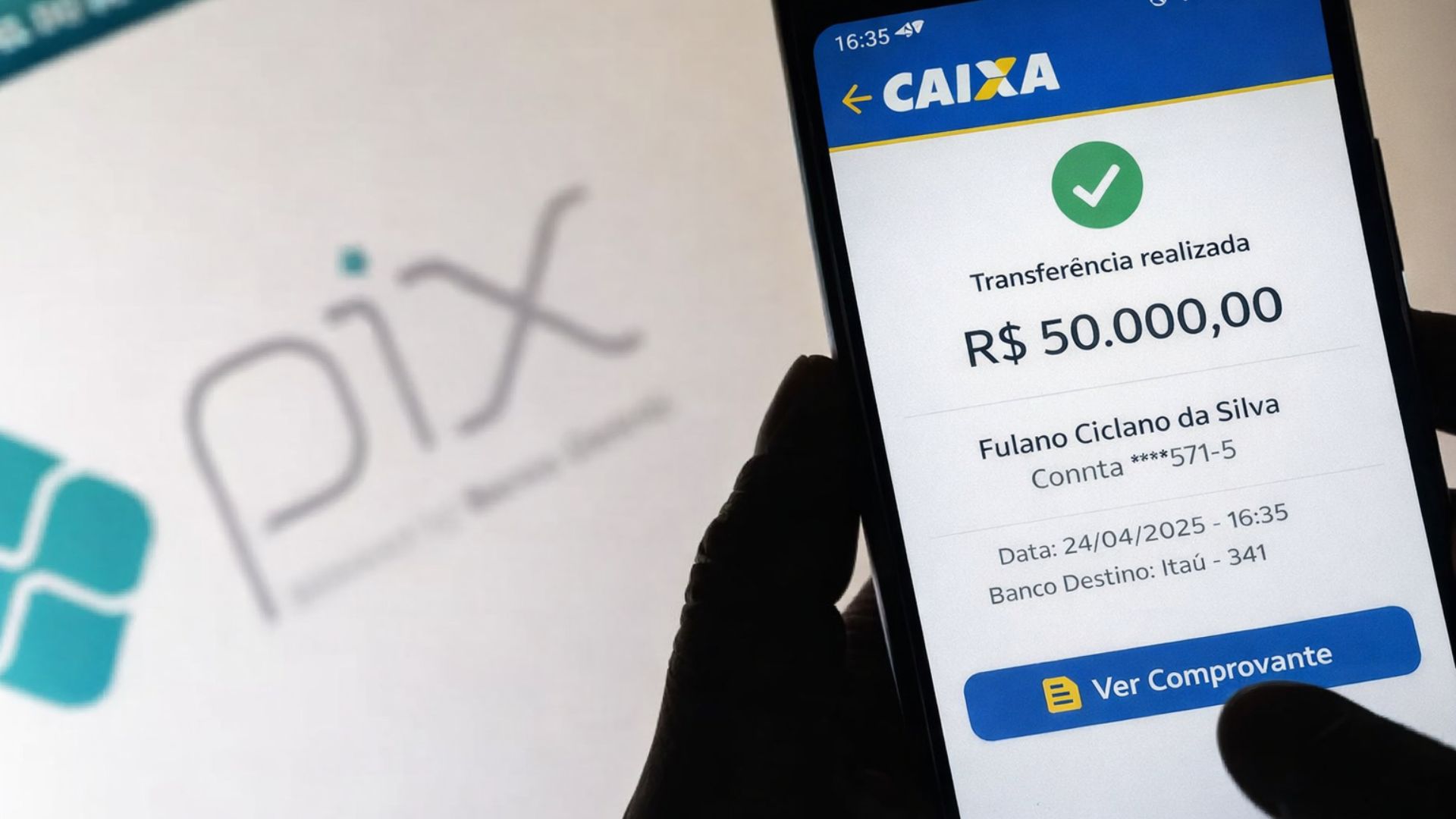

After mistakenly transferring R$ 50,000 via Pix, a man will receive the amount back along with R$ 10,000 for moral damages from the recipient.

How the New Credit Line Works

The program is divided into three income brackets. The Bracket 1, which serves families with a gross monthly income of up to R$ 2,850, will have lower interest rates and will be backed by the Popular Housing Guarantee Fund (FGHab), which currently has around R$ 1 billion to cover defaults.

If a borrower cannot pay, the fund covers part of the installments.

In Bracket 2, the conditions will still be favorable, but without the FGHab guarantee. Bracket 3 will be limited to financing at market rates, without subsidy.

This division shows that the initial focus is on reaching the most vulnerable groups, although the reach depends directly on the Treasury’s ability to absorb financial risks.

The government stated that the resources will partially come from the Pre-Salt Social Fund, with R$ 7.5 billion reserved in 2025 and another R$ 7.5 billion in 2026, in addition to remaining balances from previous fiscal years.

However, since there will also be complementary credit lines with market resources, the total amount of financing may exceed the announced R$ 30 billion.

The Hidden Subsidy and Its Impact on the Treasury

The most criticized point by analysts is the financing method. The subsidy does not appear in the budget, but materializes in the difference between the basic interest rate of the economy, the Selic (15% per year), and the interest charged to beneficiary families, well below that level.

This difference is funded by the National Treasury, silently increasing the Union’s liabilities.

While it does not infringe the spending ceiling or the fiscal target, the real cost shows up in the evolution of public debt, which is already considered high for emerging countries.

Fiscal Risk and Limited Reach

Another challenge is the sustainability of the FGHab, whose coverage capacity may not be sufficient in the face of a possible wave of defaults.

The government still needs to define the level of leverage allowed for the fund, which may limit the number of families served.

Experts warn that the program, while socially relevant, may have a smaller reach than promised.

Without expanding guarantees or allocating new resources to the FGHab, the risk of default will fall on the Treasury, increasing the long-term cost.

And you, do you believe that this type of policy compensates for future risks to the economy, or do you think the government should adopt more transparency regarding the involved costs?

Leave your opinion in the comments; we want to hear from those who experience this reality in practice.

Seja o primeiro a reagir!