Portuguese

Portuguese  English

English  Spanish

Spanish

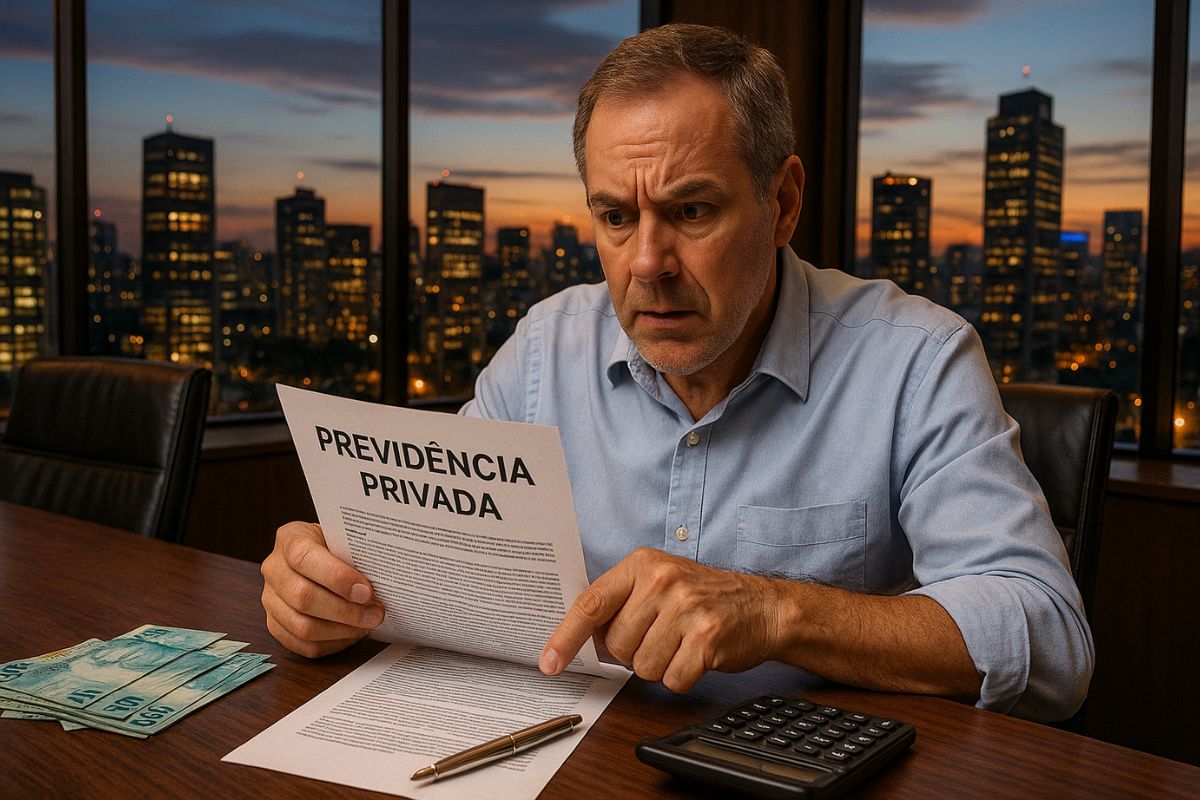

Is Private Pension Worth It? What You Haven’t Been Told Before Signing the Contract. Corporate Plans, PGBL, VGBL and Traps That Can Be Costly: Discover When Private Pension Makes Sense and When It’s Certain Loss

The private pension is often presented as a solution to secure your financial future, but the reality is that it is not always advantageous. Depending on the type of plan, length of stay, and contractual conditions, it can be a strategic tool or a poor investment. What few people know is that there are hidden traps, from abusive fees to restrictive withdrawal rules that can compromise returns.

Let’s analyze the scenarios in which private pension is truly interesting and when it’s better to seek alternatives. We will also explain the types of plans, tax regimes, and the points that most catch unwary investors.

Corporate Plans: The Role of Match and Vesting

If your company offers a corporate private pension plan, the first point is to understand if there is a match — when the company complements your contribution. For example, if you invest R$ 500 per month and it adds the same amount, you are doubling the contribution at no extra cost to you.

-

Brazil Ignores Trump’s threats to BRICS, Buys 42 tons of gold and reduces the Dollar’s share by 6.45% in international reserves.

-

Havan buys historic football land in Blumenau for a million-dollar amount protected by a confidentiality clause and is already planning to change even the layout of streets to build a megastore in half-timbered style costing 80 million reais.

-

Mercado Livre “opens the vault” and announces a record investment of R$ 57 billion in Brazil in 2026, a value 50% higher than the previous year, with an expansion plan that includes 14 new logistics centers, totaling 42 units in the country and hiring an additional 10,000 employees.

-

How investment in technology can revolutionize the national economy and enhance industrial gains, according to a study that highlights the direct impact on productivity, innovation, and wealth retention within Brazil.

However, this benefit usually comes with vesting, a rule that conditions the right to the amount invested by the company to a minimum length of stay. If you leave early, you may lose part or even all the money it deposited. Staying less time than required can turn the benefit into a loss.

Individual Pension: PGBL vs VGBL

Those seeking a pension on their own find two main formats: PGBL and VGBL. The PGBL allows you to deduct up to 12% of your annual gross income from Income Tax, but the taxation upon withdrawal is on the total accumulated (contribution + earnings). It is suitable for those who file a complete tax return and contribute to INSS.

The VGBL, on the other hand, does not offer a deduction on Income Tax, but upon withdrawal, the taxation applies only to the earnings. It is more commonly used in estate planning, as it facilitates asset transfer without probate and avoids ITCMD in some states. Those who file under the simplified model or have already reached the deduction limit tend to benefit more from it.

Tax Regimes: Progressive or Regressive

In the progressive regime, the Income Tax varies from 0% to 27.5% based on the amount withdrawn in the month, with adjustments in the tax return. It is recommended for those who will make smaller withdrawals or in the short term.

The regressive regime starts at 35% and decreases to 10% after 10 years, without adjustments in the tax return. It is more advantageous for those who can maintain the investment long-term. Starting in 2024, the choice can only be made at the time of the first withdrawal, a change that provides more flexibility for the investor.

Fees and Traps That Erode Returns

Even with tax benefits, a poor plan can undermine the strategy. Pay attention to the fees: entry/exit fees, above-average management fees, and unwarranted performance fees. Another risk lies in “fund of funds,” which embed hidden extra costs.

Furthermore, pension plans from traditional banks usually have management fees exceeding 2% per year, which, in the long run, can significantly reduce net profitability. Before signing, compare costs, funds, and historical real returns (already discounting all fees and taxes).

When It’s Worth It and When It’s Not

It’s worth it when:

- The company offers a match and you intend to stay long enough to receive 100% of the benefit.

- The plan has low fees and quality funds.

- You are in the maximum Income Tax bracket and can use PGBL to lower your tax.

- You want estate planning with simplicity, using VGBL.

It’s not worth it when:

- You will need to withdraw in a few years (high tax and possible loss of vesting).

- The plan has high fees and low performance.

- You are exempt or file under the simplified model and do not take advantage of the tax benefits of PGBL.

What to Consider Before Deciding

Before contracting, ask:

- What is the total fee (entry, management, and performance)?

- Is there a match and what is the vesting period?

- What assets compose the portfolio?

- Is there a possibility of portability to another more advantageous plan?

Private pension can be a great instrument, but only when chosen with care. Ignoring costs and rules can turn a benefit into a financial trap.

And you? Have you already done or considered doing a private pension? What was your experience, and what weighed most in your decision? Share your opinion in the comments so we can exchange ideas about what really works in practice.

-

-

-

-

-

-

31 pessoas reagiram a isso.