Portuguese

Portuguese  English

English  Spanish

Spanish

Simulation Based on Central Bank Data Shows How Much R$ 15 Thousand Yields in Savings in 30 Days and Warns of More Advantageous Alternatives Available in the Market.

The Caixa Savings Account is one of the most popular investments in Brazil. But is it still worth keeping the money there?

A recent simulation, based on the most recent data from the Central Bank, helps answer this question simply and directly.

Yield Is the Same at All Banks

Anyone who puts money in savings, regardless of the bank, receives exactly the same yield.

-

The institute that trained the greatest aerospace engineers in Brazil has just opened its first campus outside São Paulo after 75 years: ITA Ceará will have R$ 445 million, new courses in energy and systems, and classes are expected to start in 2027.

-

Luciano Hang, owner of Havan, goes to Juiz de Fora after the tragedy in February, brings R$ 1 million, hands out R$ 2,000 cards, and donates up to R$ 15,000 to victims in the region.

-

The Brazilian passport allows legal residence in dozens of countries without the need for a prior visa, and most Brazilians are unaware that they can apply for residency directly upon arriving in nations in South America, Africa, and even Europe.

-

Petrobras sends a message to Brazilian truck drivers after fuel collapse and reveals plan to have 100% domestic diesel.

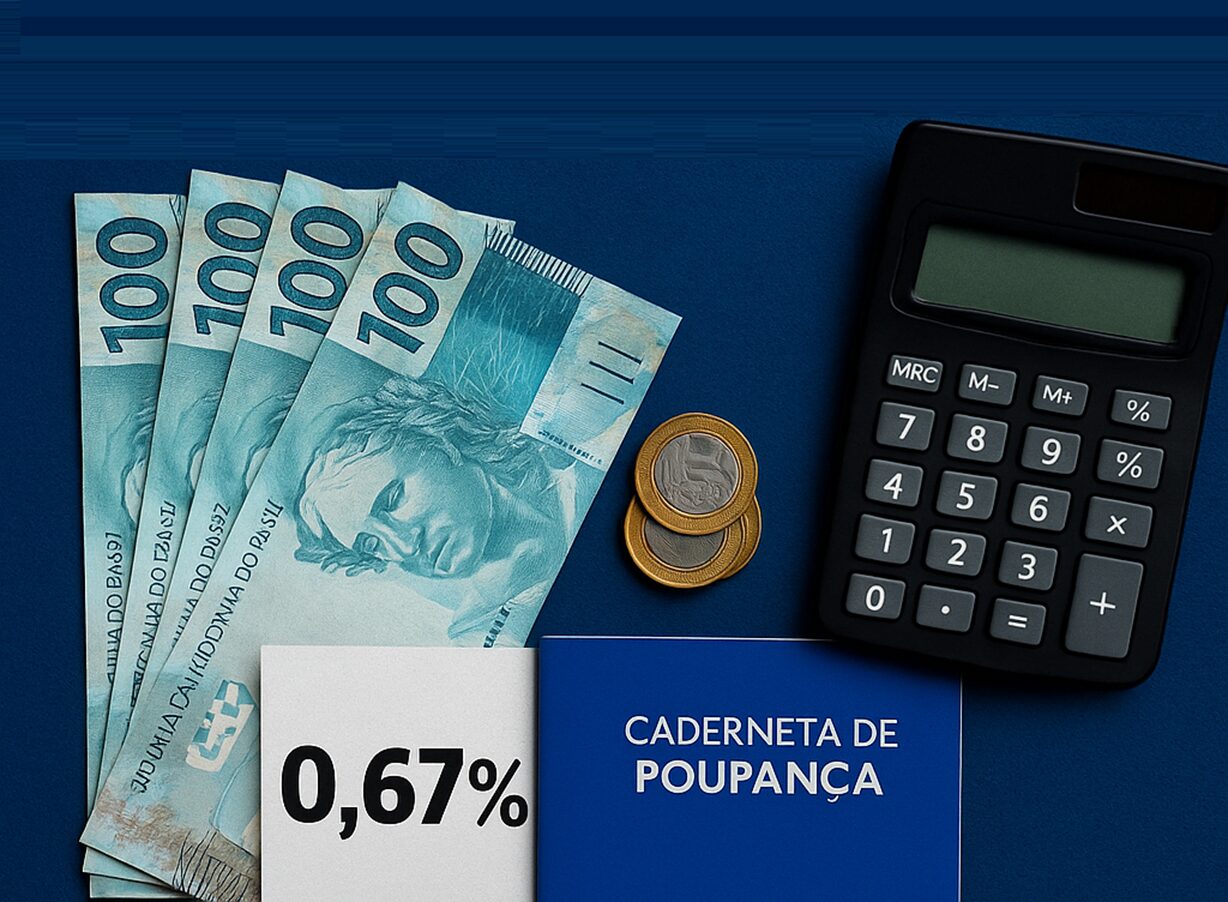

The percentage is set by the Central Bank and does not change between institutions. According to the most recent data released on the Central Bank website, the monthly yield of savings was 0.67%.

With this rate, it is possible to calculate how much R$ 15 thousand invested for 30 days yields.

The answer is straightforward: R$ 100.50. This is the net amount the investor receives at the end of the month, without any tax deductions.

This is because savings are tax-exempt, simplifying the calculation and attracting many more conservative investors.

It Is Necessary to Leave the Money for 30 Days

An important point: to receive this full yield, the amount must remain in the account for at least 30 consecutive days.

If the money is withdrawn before the deadline, the proportional yield is not paid. In other words, any transaction before the investment’s anniversary date nullifies the earnings for that month.

This limits the flexibility of the investment and can be a problem for those in need of immediate liquidity.

Therefore, it is crucial to consider whether the money can truly be left static for this period before investing in savings.

Are There More Advantageous Options?

Although the yield from the Caixa Savings Account is secure and tax-free, it is far from being the most attractive in the market. Many banks offer investments like CDBs that yield 100% of the CDI.

In these cases, the yield is usually higher, even with income tax charged on profits.

Thus, those who keep money stagnant in savings should assess whether it is worth maintaining this habit. The difference in yields over the long term can be significant.

The final reflection is simple: do you continue to keep your money in savings for convenience, or have you started looking for alternatives with better returns?

Seja o primeiro a reagir!