Portuguese

Portuguese  English

English  Spanish

Spanish

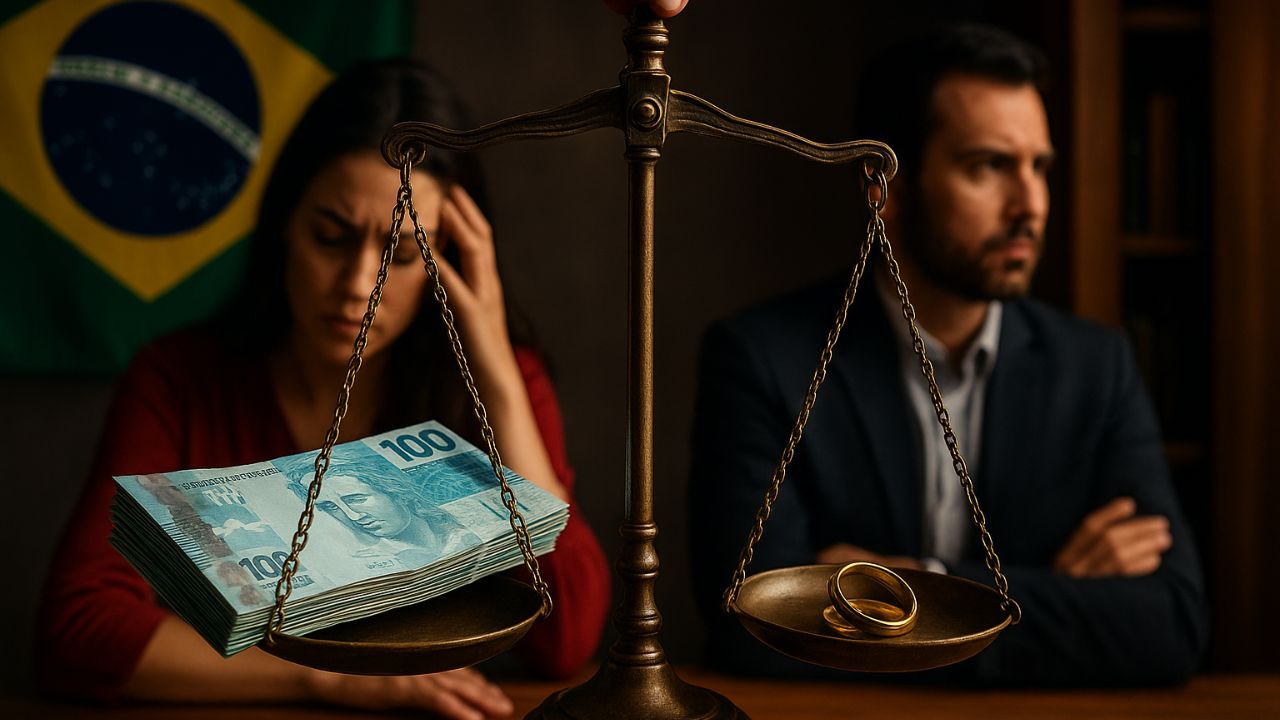

Decision Protects Partners Who Use Share Bonus to Increase Capital, Provided the Original Shares Are Private Assets; The Understanding of STJ Sparks Intense Debate on the Balance in Asset Division.

A decision from the Superior Court of Justice (STJ) established an important precedent at the intersection of Family Law and Corporate Law, shielding partners in divorce proceedings. According to an in-depth analysis by the Consultor Jurídico portal, increasing a company’s capital through the reinvestment of profits or reserves, an operation known as a bonus, should not be shared if the original shares are considered private assets of one spouse.

This understanding directly impacts asset division in partial community property regimes, the most common in Brazil. The measure aims to protect business assets, treating capital increases as an extension of the original asset, and not as a “fruit” acquired during marriage. However, the decision raises an alarm about potential imbalances in the division, prompting questions about the protection of the spouse who is not involved in the partnership.

What Is a Share Bonus and Why Is It So Important?

A share bonus, or capitalization of reserves, is an accounting and corporate operation where profits that have not been distributed to partners (dividends) are incorporated into the company’s capital. Instead of receiving cash, the partner sees their share in the company increase, either through the issuance of new shares or by increasing the nominal value of existing ones. It is, in practice, an automatic reinvestment of earnings into the business structure itself.

-

With the arrival of Law 11.788, internships are now recognized as professional experience.

-

The Brazilian Civil Code states that a property owner has the right to cut the roots of a neighbor’s tree that invade their land, as long as it does not harm the tree itself. The owner must notify the neighbor before taking such action.

-

Engineer is sentenced to repay R$ 148 thousand after holding public positions in three municipalities in Rondônia with incompatible schedules, and the decision is upheld by the Court of Justice.

-

Chamber approves project that creates mandatory Life Insurance for police officers, firefighters, guards, and traffic agents.

According to experts consulted by the Consultor Jurídico, this is a common strategy to strengthen a company’s cash flow, finance expansions, or simply increase its financial robustness without the need for external contributions. The central point of legal discussion is that while the profit is generated during the marriage, it does not actually pass through the personal assets of the partner; it is directly converted into more capital for the legal entity, which completely changes its nature for sharing purposes.

Fruit or Extension of the Asset? The Key to the STJ Decision

The Civil Code, in its article 1,660, establishes that “the fruits of common assets, or of the particular assets of each spouse” must be shared in the partial community property regime. If one spouse has a rented private property, for example, the rental value (the fruit) received during the marriage belongs to the couple. The big question that the STJ needed to answer was: is a share bonus a fruit, like a dividend, or merely an extension of the original private asset?

The Court’s conclusion, in line with corporate doctrine and the Corporation Law (LSA), was that the bonus does not represent a real increase in the shareholder’s assets but rather an reallocation of values within the company’s own balance sheet. As highlighted in the analysis by the Consultor Jurídico, there is no transfer of wealth from the company to the partner. The LSA itself, in article 169, reinforces this thesis by determining that the non-communicability that applies to the original shares extends to the shares resulting from the bonus.

The Precedent Established and Legal Certainty

The position of the STJ was consolidated in the judgment of Special Appeal (REsp) No. 1,595,775. In it, the ministers stated that the bonus shares do not qualify as fruits and therefore are not communicated when the shares that originated them are private assets. This decision creates a clear precedent, offering greater legal certainty for partners and entrepreneurs by defining the rules of the game in a potential divorce.

For the corporate world, clarity is essential. The decision allows companies to deliberate on capital increases via retained earnings without the uncertainty that this strategic operation could, in the future, be undone or contested in a family dispute. This protects the integrity of the capital stock and the governance of the company, preventing marital issues from directly interfering in the management and financial health of the business.

The Alert for Fraud and Imbalance in Division

Despite the corporate logic behind the decision, the topic continues to cause controversy in Family Courts. The main concern is that this interpretation could be used in bad faith. A controlling partner, for example, could deliberately choose not to distribute dividends (which would be shareable) and accumulate profits in the company, capitalizing them to shield this asset from the spouse in the divorce. The Consultor Jurídico points out that this concern is legitimate and should be analyzed on a case-by-case basis.

It is crucial to understand that the STJ decision does not legalize fraud. If it is proven that there is an abuse of rights or the use of the legal entity with the clear intention of harming the other spouse, the situation changes. The courts have tools to curb such practices, such as the disregard of legal personality. What the decision establishes is that the bonus operation, in itself, is legitimate. The analysis of the intent behind it remains a task for the judge in each specific case.

The decision of the STJ sheds light on a complex subject, bringing a technical definition that privileges the corporate nature of the operation. At the same time, it exposes the tension between protecting business assets and the pursuit of justice in the division of assets built during a shared life.

Do you agree with the decision of the STJ? Do you think this measure fairly protects the business environment or could it create loopholes for injustices in divorce? Share your opinion in the comments; we want to hear what you think on the subject.

-

Uma pessoa reagiu a isso.