Portuguese

Portuguese  English

English  Spanish

Spanish

Brazilians withdrew R$ 23.5 billion from savings in January, the largest volume of withdrawals in an entire year, followed by R$ 6.6 billion in February and R$ 11.1 billion in March, in a scenario where the Selic at 14.75% per year makes other investments much more profitable than the savings account.

Brazilians are withdrawing money from savings at a pace not seen in a long time. In three consecutive months of net withdrawals, the savings account lost more than R$ 41 billion, especially in January when Brazilians withdrew R$ 23.512 billion, the largest volume of withdrawals in an entire year. February recorded withdrawals of R$ 6.616 billion, and March closed with a negative balance of R$ 11.118 billion, according to data released by the Central Bank this Thursday (9). It is the third consecutive month of withdrawals, and the first quarter of 2026 has already accumulated a deficit that signals a change in the financial behavior of Brazilians.

The scenario is not difficult to explain. With the Selic rate at 14.75% per year, savings yield significantly lower returns than alternatives such as CDBs, Treasury Direct, and fixed income funds, and Brazilians are doing the math. The profitability of the savings account is given by the reference rate plus 0.5% per month, a formula that applies while the Selic is above 8.5%. Even so, the real return falls below investments with similar liquidity and no additional risk. The result is queues for withdrawals that do not stop.

Why are Brazilians withdrawing money from savings in 2026

The answer combines two factors. The first is profitability. With the Selic at 14.75%, fixed income investments such as CDBs from medium banks, LCIs, LCAs, and Treasury Selic offer returns far superior to savings with equivalent or even lower risk.

-

São Paulo has connected its two airports by rail for the first time in history, and now you can travel by train from Congonhas to Guarulhos for just R$ 5.40. However, the journey requires four transfers, takes about two hours, and only operates during a narrow time window that almost no one can use.

-

Curitiba will have a direct flight to Europe starting in July, and for the first time in history, Paraná will have a continuous air connection with Europe, saving three hours of travel for passengers who previously needed to connect in São Paulo.

-

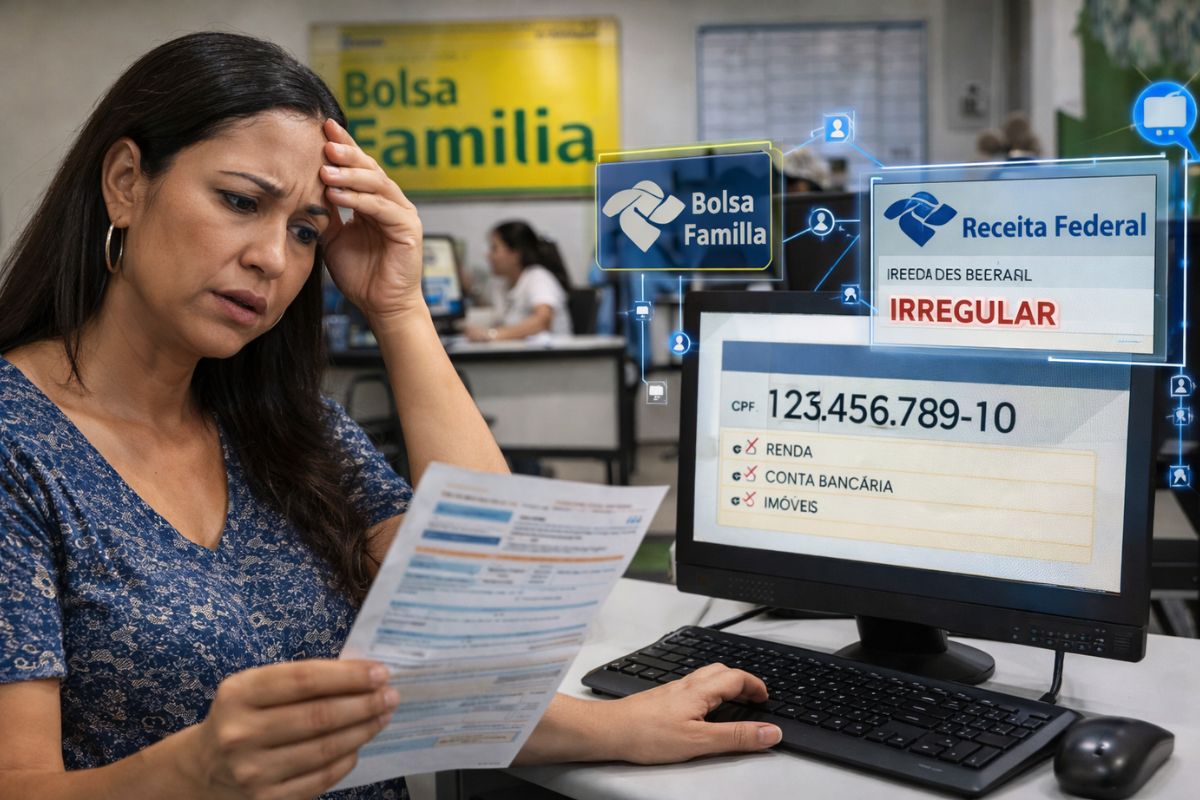

The federal government will cancel Bolsa Família and other benefits for millions of Brazilians who do not update their CadÚnico in 2026, and the new system already cross-references data with the Federal Revenue Service in real time to identify those who are irregular.

-

Famous sertanejo singer and the automaker BYD appear together on the federal government’s dirty list after instances of work analogous to slavery in Goiás and Bahia.

According to information from the CNN Brasil, for Brazilians who leave money in the savings account out of habit or convenience, the difference in yield has become too large to ignore especially in a scenario where inflation pressures purchasing power and every percentage point of yield makes a difference in the budget.

The second factor is financial pressure. Brazilians are facing high costs for housing, food, and services, and savings often serve as an emergency reserve that is tapped when expenses exceed income.

The withdrawal of R$ 23.5 billion in January, a month of property tax (IPTU), vehicle tax (IPVA), school supplies, and other concentrated expenses suggests that a significant portion of the withdrawals is not a migration to better investments, but forced consumption. For many Brazilians, the piggy bank is not being exchanged for another investment; it is being spent.

What the numbers from March reveal about the pace of withdrawals by Brazilians

The negative balance of March, at R$ 11.118 billion, was greater than that of February (R$ 6.616 billion), indicating that the pace of withdrawals is not slowing down after the peak in January.

The SBPE (Brazilian Savings and Loan System) recorded a negative balance of R$ 9.089 billion, while rural savings had net withdrawals of R$ 2.029 billion both modalities losing resources simultaneously.

The persistence of withdrawals for three consecutive months indicates that this is not an isolated event. Brazilians are consistently reducing their balances in the savings account, either due to cash needs or investment decisions.

The accumulated R$ 41 billion in the quarter is a significant volume that, if maintained at this pace throughout the year, would represent the largest outflow of resources from savings in recent history.

What does the Selic at 14.75% have to do with the withdrawals of Brazilians from savings

The relationship is direct and mathematical. With the Selic at 14.75% per year, savings yield approximately 7.7% per year while investments linked to the Selic or CDI deliver returns close to 14% net.

For Brazilians who have R$ 50,000 in savings, the difference amounts to more than R$ 3,000 per year in lost earnings money that simply evaporates due to inertia.

The math is simple, but changing habits is difficult. Savings accounts have income tax exemption, immediate liquidity, and are available at any bank without the need to open an account with a brokerage.

Even so, the tax advantage does not compensate for the difference in profitability in the current scenario, and Brazilians are realizing this. Investments such as LCI and LCA are also exempt from income tax and offer much higher returns for those who accept waiting periods that range from 90 days to a year.

What the withdrawals mean for the economy and the future of savings

The money that leaves savings does not disappear; it goes somewhere. If it migrates to other investments, the economy gains efficiency in capital allocation.

If it goes to consumption, it may boost retail in the short term, but it means that Brazilians are depleting their reserves, which increases the financial vulnerability of families in the face of unforeseen events.

For the real estate market, the continuous withdrawals from the SBPE are concerning. Savings is one of the main sources of housing finance in Brazil, and the persistent reduction of deposits may increase the cost of mortgage credit or force changes in the funding composition of banks.

The scenario is paradoxical: the high Selic that attracts Brazilians away from savings is the same that makes real estate financing more expensive, which depends precisely on these resources. As long as interest rates do not fall, the outflow from the savings account should continue, and Brazilians’ piggy banks will keep emptying.

Do you still have money in savings or have you already migrated to other investments? Do you think it is worth keeping the savings account with the Selic at this level?

Seja o primeiro a reagir!