Portuguese

Portuguese  English

English  Spanish

Spanish

Petrodollar, BRICS and Alternative Payment Systems: How the Decline of Dollar Participation Below in Global Reserves, the Freezing of Russian Assets, the Expansion of Gold in Central Banks and Projects Like BRICS Pay, The Unit, CIPS and mBridge Expose a Structural Limit Between Military Hegemony and International Financial Control

The petrodollar system, the foundation of United States financial hegemony since the post-war era, faces a structural shock with the decline of dollar participation in global reserves, the advance of gold, and the BRICS’ efforts for alternative payment and settlement mechanisms outside of SWIFT.

The petrodollar is presented as one of the central pillars of contemporary financial hegemony, functioning as a permanent mechanism for capital recycling.

In this arrangement, global oil trade revenues return to the United States in the form of continuous purchases of Treasury bonds, financing high military spending and prolonged conflicts.

-

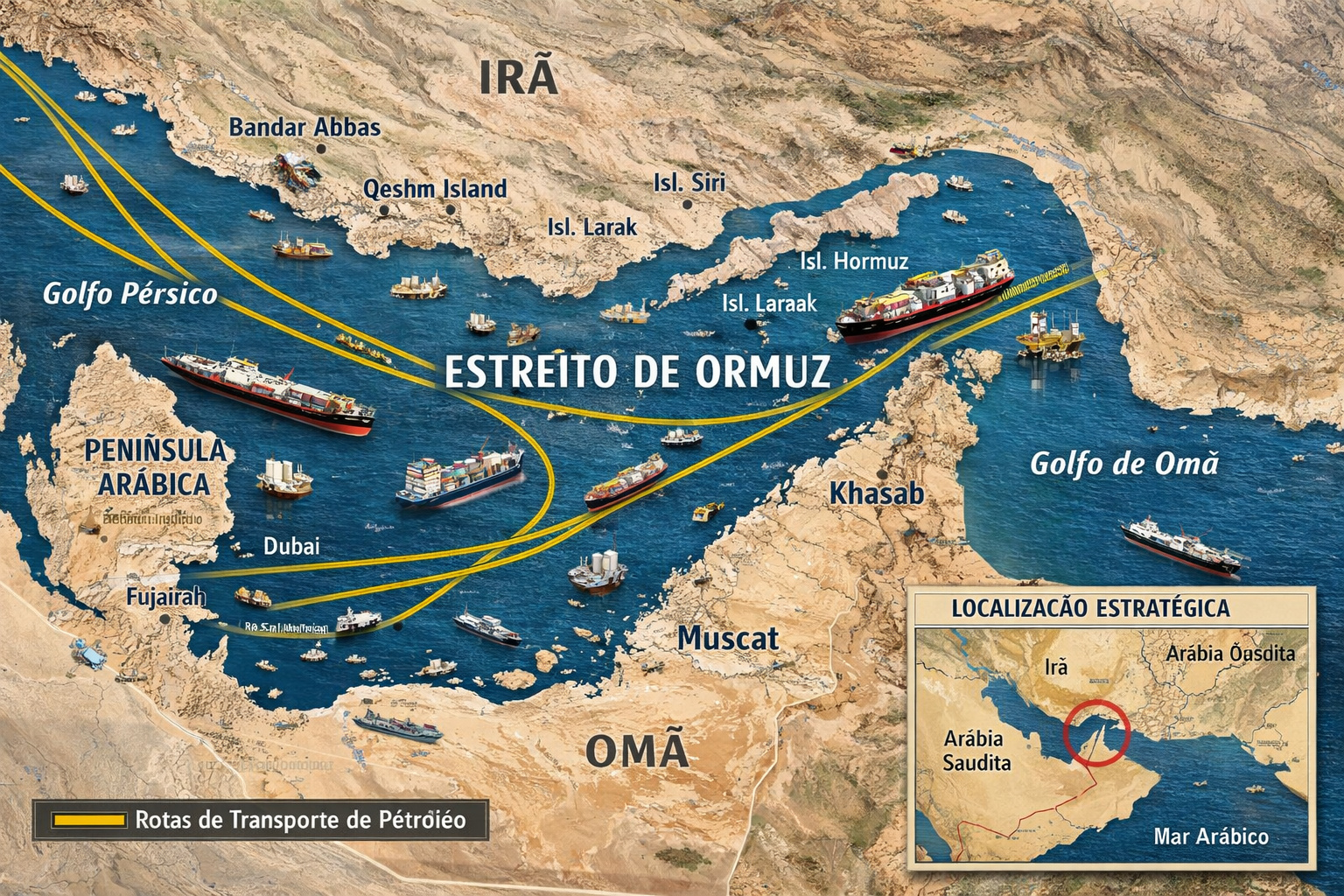

Global summit with over 40 countries pressures Iran for a blockade in the Strait of Hormuz and warns of direct impact on oil, food, and the global economy.

-

Russia has broken the U.S. maritime blockade to send oil to Cuba and is now loading a second ship while Trump says that “Cuba is next” in a possible military action against the island.

-

Spain challenges the USA and closes its airspace for operations against Iran, raising global tension and provoking the threat of a trade rupture.

-

While no other country manufactures tanks in Latin America, Argentina activates the TAM 2C-A2 and raises a curiosity about the technological lag in the region.

Any country that considers reducing its dependence on this system faces asset freezes, economic sanctions, or even more severe measures.

This model, however, coexists with a structural contradiction. Maintaining dominance requires increasing resources, obtained both through the expansion of spheres of influence and through the constant issuance of dollars as the global reserve currency.

At the same time, the external debt of the United States functions as a financial containment mechanism for rivals, forcing other countries to sustain the system by acquiring dollar-denominated assets.

The United States must choose between sustaining ever-increasing military spending, exemplified by the proposed budget of US$ 1.5 trillion for the Department of Defense, or preserving control of the international financial system.

The thesis is that it is not possible to maintain both fronts simultaneously in the long term.

Ukraine, Financial Sanctions and the Structural Shock of the System

In this context, the war in Ukraine appears as a turning point. Faced with the impossibility of demonstrating absolute power without compromising its own financial bases, the system reportedly considered the country “disposable”, at least in theoretical terms.

More relevant than the conflict itself was the intensification of the use of the financial system as a geopolitical weapon.

The exclusion of Russia from the SWIFT system and the freezing of its assets abroad are described by experts as the event that broke the tacit balance of the post-World War II era.

For the first time, a nuclear-capable country has been effectively expelled from the main global payments infrastructure. For various central banks, this episode made it clear that dollar reserves or Western financial assets can, in practice, be confiscated.

In direct response, central banks from different regions began to increase their gold reserves, intensify bilateral agreements, and study alternative payment systems. This movement is described as the first major structural fissure in the international financial system since the end of World War II.

The BRICS emerge in this context, not as a bloc seeking to overthrow the existing system, but as an arrangement aimed at building a functional alternative.

The goal is to facilitate international payments, large-scale infrastructure financing, and commercial settlements without dependence on the dollar or SWIFT.

Venezuela, Iran and the Limits of Dollar Exclusion

Venezuela is a critical case study. The central question is whether a major oil producer can survive outside the dollar system without experiencing economic collapse or institutional destruction. The hegemonic system’s implicit answer has been negative.

However, experts relativize Venezuela’s weight on the geopolitical chessboard, highlighting that the country represents only 4% of China’s oil imports.

The truly decisive case would be that of Iran, which sells about 95% of its oil to China, with settlements made in yuan, not in dollars.

Iran, unlike Venezuela, has reportedly resisted coordinated attempts at destabilization, including intelligence operations, attacks, and regime change initiatives.

Despite this, the threat of war remains a constant element, reinforcing the coercive nature of the current international system.

Dollar, Gold and the Erosion of Traditional Reserves

In the first quarter of 2025, its dominant share in exchange reserves was 57.79%. In the second quarter of 2025, this share fell to 56.92%, reflecting a gradual diversification of global reserves as international financial markets continue to expand and evolve. Source: IMF.

This movement is described as a race among central banks for assets deemed politically neutral or less susceptible to sanctions.

The acceleration of alternative system testing by the BRICS occurs in this environment, characterized as a “laboratory” for parallel financial solutions.

The central challenge is not only to create new instruments but to ensure that they can process high volumes of transactions.

The SWIFT system processes at least US$ 1 trillion in transactions per day, establishing a significant technical and operational barrier for any alternative.

The Unit, mBridge and BRICS Bridge

Among the proposals under discussion, The Unit stands out, described as a blockchain-based trade token that is non-sovereign and apolitical.

It would not function as currency but as a unit of account for settling commercial and financial transactions among participating countries.

The proposal envisions that The Unit will be backed by a basket of commodities or a neutral index, avoiding the dominance of a single country. Its operation is compared to the IMF’s Special Drawing Rights, but restricted to the BRICS ecosystem.

Another initiative is mBridge, a shared central bank digital currency system among monetary authorities and commercial banks.

Although not formally part of the so-called “BRICS laboratory”, mBridge involves five members, including the Digital Currency Institute of the People’s Bank of China and the Hong Kong Monetary Authority, along with the declared interest of 30 other countries.

Inspired by mBridge, BRICS Bridge aims to accelerate international transfers, payment processing, and account management, eliminating the need for prior conversions to dollars.

In this model, countries in the bloc exchange currencies directly, reducing costs and dependence on the Western financial system.

The Role of the New Development Bank

The New Development Bank, established in 2015 in Shanghai, is identified as the potential central node of the BRICS Bridge. The institution could take on currency conversion, compensation, and settlement functions within the alternative system.

However, the bank’s statutes are still tied to the dollar, which hinders its full integration into the new arrangement. This limitation necessitates a profound structural review before the bank can operate as a financial axis of an independent system.

The delay in this adaptation is described as one of the main bottlenecks of the project, highlighting the gap between conceptual formulation and practical implementation.

BRICS Pay and the Operational Challenges

BRICS Pay is presented as a distinct strategic infrastructure aimed at building a financial system described as decentralized, sustainable, and inclusive. Currently in pilot phase, the project is expected to remain in testing until 2027.

After this deadline, member countries must discuss the creation of a settlement unit for intra-BRICS trade by 2030 at the latest.

This is not a global reserve currency, but a parallel and compatible option to SWIFT within the bloc’s ecosystem.

In its initial practice, BRICS Pay allows tourists and business travelers to make payments via QR code, linking Visa or Mastercard cards to the application.

This dependence, however, is identified as a central problem, as it keeps the system under financial oversight from the United States.

The strategic challenge is to incorporate the own brands of the countries in the bloc, such as UnionPay and Mir, and reduce exposure to sanction mechanisms. For larger and more complex transactions, the obstacle of completely bypassing SWIFT still persists.

Interoperability, Settlement and Sanctions

All ongoing tests face two central problems. The first is the interoperability of financial messages, which requires secure and standardized data formats.

The second is the effective processing of settlement, that is, how funds move between central bank accounts without passing through systems subject to sanctions.

These obstacles explain why, despite conceptual advances, solutions have yet to reach a global scale comparable to that of the existing system. The technical and institutional path is long, but the search for alternatives is considered irreversible.

Yuan, CIPS and the Hypothesis of a New International Currency

The internationalization of the yuan emerges as one of the most concrete possibilities. The CIPS system, based on the Chinese currency, already operates in 124 countries and is described as extremely popular among participants in the so-called Global South.

Creating an entirely new system is difficult and costly, making the utilization of existing structures a lower resistance option. Still, there are reservations about the yuan’s ability to broadly and quickly replace the dollar.

As an alternative, the proposal for a new international currency issued by a specific institution, inspired by John Maynard Keynes’ Bancor, conceived in 1944 and vetoed by the United States in the context of Bretton Woods, arises.

This currency would have exclusive use in international transactions, circulating in parallel to national currencies, without domestic function.

Its value would be based on a weighted basket of currencies from participating countries, with weights defined by each economy’s share in terms of purchasing power parity.

Oil, Sanctions and the Core of Hegemony

The control of global oil trade is seen as a central privilege of American hegemony. Pricing and payment in dollars ensure capital recycling to US financial assets.

In this arrangement, alternative energy sources are discouraged, while countries exporting oil outside this control are treated as threats to the established order.

The existence of independent energy flows is described as a factor that weakens the capacity for economic coercion.

The BRICS’ efforts around alternative payment systems thus appear as a direct response to this strategy of creating bottlenecks and dependencies.

A Moment of Structural Transition

The costs of maintaining hegemony have become prohibitive. The approach of a structural change is described as inevitable, marked by the loss of the ability to impose unilateral wills through financial means, leaving only the threat of open warfare.

In this scenario, the BRICS are presented as actors seeking to capitalize on this historical moment, bringing together economic, political, and intellectual efforts to escape a system considered inefficient, unstable, and dangerous.

Even acknowledging the risks of retaliation and sanctions, inaction has become riskier than the attempt to build alternatives.

The impasse between military hegemony and global financial control has entered its decisive phase, with consequences still in full formation.

Ótima matéria ,bem explicado. Esperamos que no futuro os países criem este sistema que não depende de moeda de nenhum país, para a conversão de moedas em todos os países . Com os direitos iguais a cada

O ser humano em toda a sua existência sempre desagradando Deus.

Contexto de Gênesis 6:6-7

O Motivo: A maldade e corrupção humana haviam se espalhado de tal forma que o coração de Deus foi ferido