Portuguese

Portuguese  English

English  Spanish

Spanish

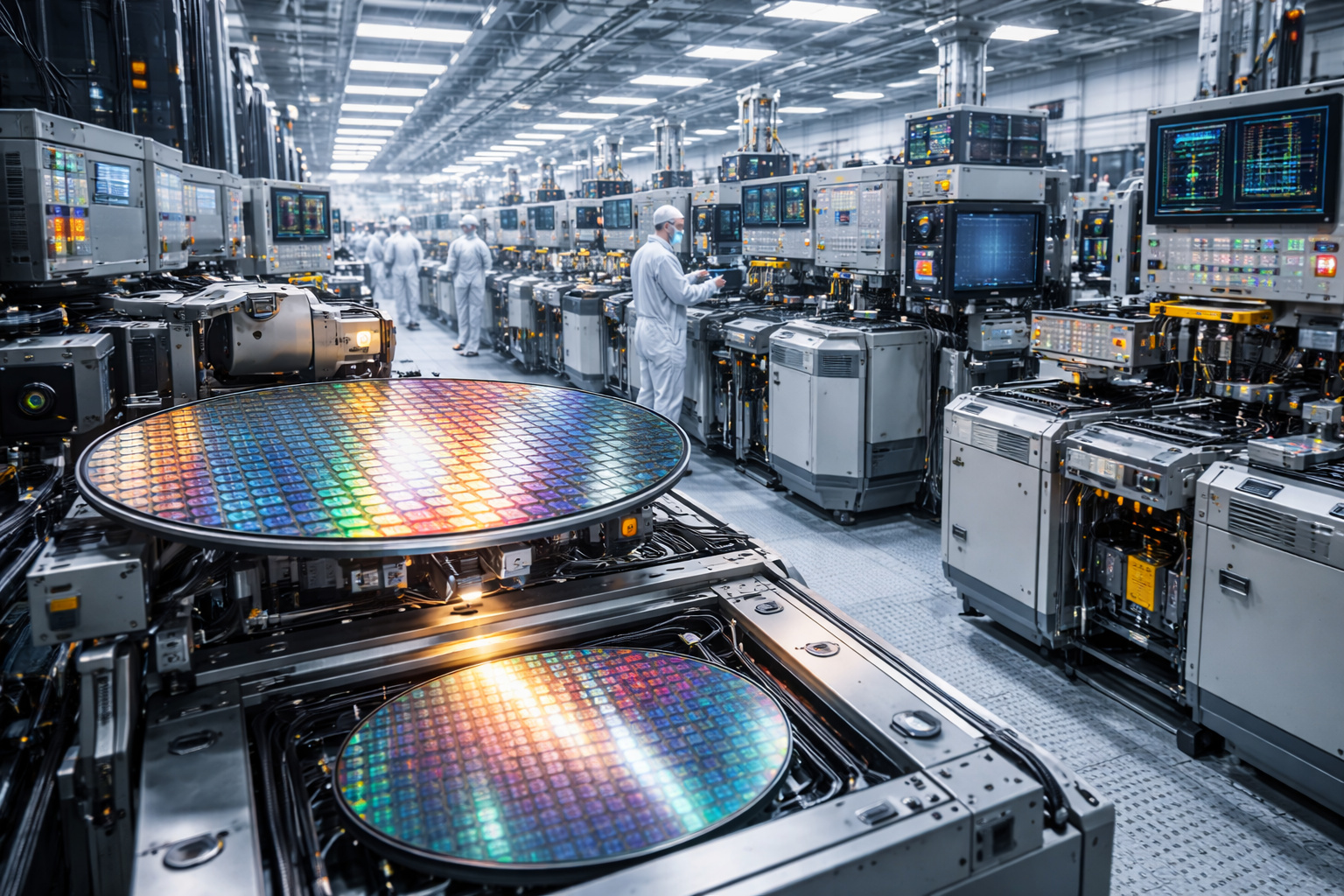

Global trade surpasses US$ 35 trillion in 2025, but a third of the growth came from AI and benefited Taiwan, South Korea, and Southeast Asia.

In 2025, global goods trade grew by 7% and exceeded US$ 35 trillion for the first time in history, according to UNCTAD. This should be good news for everyone. But when the McKinsey Global Institute opened the numbers to identify the source of this growth, the result was surprising: approximately one-third of the entire increase in global trade was driven by a single segment — semiconductors, servers, and networking equipment aimed at artificial intelligence data centers.

According to the McKinsey report from March 2026 and analyses from Euronews, AI infrastructure-related trade grew nearly 40% in just one year. This data reveals a structural shift: global trade is no longer primarily driven by traditional goods and has come to rely on a highly concentrated and technology-intensive supply chain.

Chip sector and AI infrastructure explode after 2022 and create new dynamics in global trade

In 2020, global trade in artificial intelligence data center equipment was a fraction of what it represents today. The launch of ChatGPT in November 2022 marked a turning point in the demand for advanced computational processing.

-

Retirees receive double after error that left employees without salary.

-

It may seem like an exaggeration, but it’s not: your financial life can remain weak even with a high income if you don’t cut expensive debts, invest half of the increase for 12 months, and turn R$ 2,000 or R$ 3,000 monthly into assets.

-

Toyota confirms the end of an era with the closure of a historic factory after nearly 30 years, transfers Corolla production, maintains 1,500 jobs, opens 500 positions, and announces an investment of R$ 11 billion by 2030 in a new phase in Brazil.

-

India wants to connect BRICS digital currencies for trade and tourism without relying on the dollar; this unprecedented proposal places the bloc back at the center of the global payments dispute.

In just three years, the need for AI chips, high-performance servers, and network infrastructure has grown at a speed that no traditional economic model predicted.

The global semiconductor market reached US$ 772 billion in 2025, recording a growth of 22.5% compared to the previous year. The projection for 2026 indicates a jump to US$ 975 billion, rapidly approaching the symbolic mark of US$ 1 trillion.

According to Deloitte, chips aimed at generative AI are expected to generate about US$ 500 billion in revenue in 2026, which represents approximately half of all global semiconductor sales.

Despite this, these chips account for less than 0.2% of the total volume of units sold, revealing an unprecedented concentration of value in the history of the industry.

United States lead global demand for AI data centers, but rely on Asia for hardware

The United States accounted for approximately half of the new data center capacity added worldwide in 2025, according to McKinsey.

The number of hyperscale data centers reached 1,136 units globally, with consistent growth in the average size of these facilities.

Companies such as Amazon, Microsoft, Google, and Meta planned capital investments of US$ 310 billion in 2025, a significant increase from the US$ 210 billion recorded in 2024.

This expansion drove a 66% increase in U.S. imports of artificial intelligence equipment in just one year.

However, the United States produces a reduced share of this hardware. Advanced chips are manufactured in Taiwan, memory components come from South Korea, and assembly occurs mainly in Southeast Asia.

Taiwan dominates global semiconductor production and concentrates the most advanced technology on the planet

Taiwan has established itself as the world’s leading semiconductor production hub. TSMC holds more than 60% of the global chip foundry market.

In 2025, the company’s quarterly revenue reached NT$ 839 billion, equivalent to US$ 25.5 billion, representing a growth of 41.6% compared to the previous year.

The most advanced technology nodes, such as 3nm and 5nm, accounted for 58% of the company’s revenue. According to SEMI, investments in semiconductor equipment in Taiwan grew by 134% in the first seven months of 2025, the largest global increase.

The island maintains a technological advantage estimated at two to three years over other countries in the development of chips aimed at artificial intelligence.

South Korea controls global memory market and becomes a critical piece in AI expansion

While Taiwan dominates chip logic, South Korea leads memory production, considered the main bottleneck for artificial intelligence.

Samsung and SK Hynix produce about 75% of all global DRAM. Samsung reported revenue of 26.7 trillion won in the semiconductor division in the third quarter of 2025, driven by mass production of HBM3E memory.

SK Hynix achieved revenue of US$ 17.5 billion in the same period. Both companies are already advancing in the development of HBM4, with mass production expected by the end of 2025 and capacity already committed for 2026.

Southeast Asia grows as a new industrial hub after redirection of global trade

The tariff war between the United States and China caused a 30% drop in bilateral trade, resulting in approximately US$ 130 billion in redirected Chinese exports.

Southeast Asian countries, such as Vietnam, Thailand, and Malaysia, absorbed much of this demand. ASEAN exports grew by about 14% in 2025, consolidating the region as a new global industrial hub.

Relevant investments include US$ 23.2 billion from Samsung in Vietnam and US$ 1.6 billion from Amkor Technologies in local infrastructure.

Europe faces double pressure from US tariffs and competition from Chinese products

Europe faces a scenario described by McKinsey as “double compression.” On one side, American tariffs raise the cost of European exports. On the other, cheaper Chinese products increase internal competition.

Chinese electric vehicle exports to Europe grew by 50%, surpassing 800,000 units.

Germany recorded, for the first time, more imports of Chinese vehicles than exports to China. The industrial surplus of the European Union suffered a reduction of US$ 40 billion.

China maintains record surplus as it becomes a global supplier of industrial inputs

Despite trade restrictions and a drop in exports to the United States, China achieved a record trade surplus in 2025.

The country redirected exports to emerging markets and reduced average prices by about 8% to maintain competitiveness.

The most relevant transformation was structural: China began exporting machines, industrial components, and productive capacity, consolidating itself as the “factory of factories.”

Brazil expands commodity exports and remains outside the AI value chain

Brazil expanded exports to China in 2025, especially of soybeans, iron ore, oil, and meat.

According to McKinsey, the country has one of the largest trade distances in the world, reflecting its dependence on China as a strategic partner.

Despite this, Brazil remains outside the semiconductor and artificial intelligence value chain, primarily acting as a supplier of raw materials.

Global semiconductor market approaches US$ 1 trillion and exposes geopolitical risk in Taiwan

The projection for 2026 indicates that the global semiconductor market will reach US$ 975 billion, with expectations of exceeding US$ 1 trillion before the end of the decade.

The ten largest chip manufacturers have a combined market value of US$ 9.5 trillion. Much of this production is concentrated in Taiwan, an island with 36,000 km² located in one of the most sensitive geopolitical regions on the planet.

The United States expanded restrictions on the export of advanced chips and equipment to China between 2024 and 2025. China responded by restricting exports of strategic materials such as gallium, germanium, and rare earth magnets.

This scenario created a division in global trade, with flows defined by geopolitical alignment rather than just economic efficiency.

The SEMI projects global semiconductor equipment sales of US$ 133 billion in 2025, US$ 145 billion in 2026, and US$ 156 billion in 2027.

Countries like India and Japan have implemented aggressive local production incentive programs. The goal is to reduce external dependence and ensure technological autonomy in a scenario of increasing international tension.

Now we want to know: who really controls the future of the global economy dominated by artificial intelligence?

In just five years, the map of global trade has undergone a profound transformation. Growth has shifted from being driven by traditional sectors to relying on a highly concentrated technology supply chain.

In your view, does this new configuration make the world more efficient or more vulnerable?

Seja o primeiro a reagir!