Portuguese

Portuguese  English

English  Spanish

Spanish

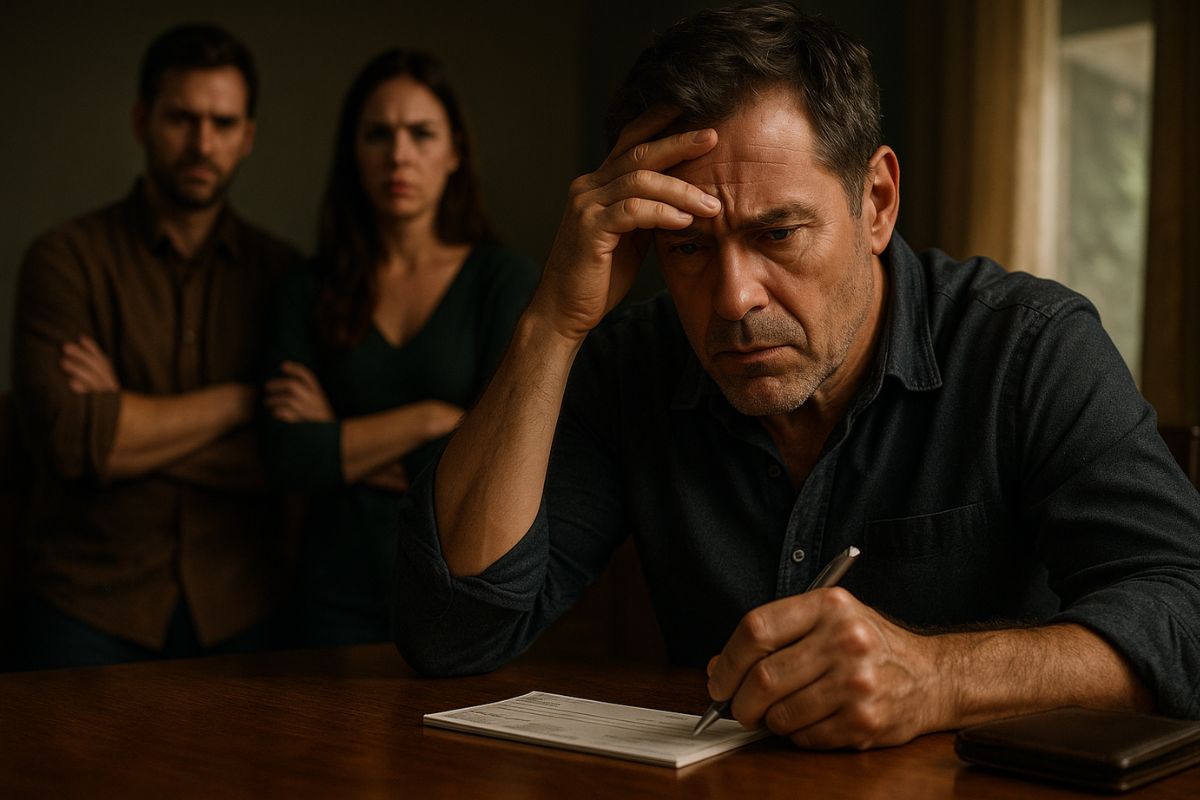

Experts Warn That Moving a Joint Account of a Deceased Person Without Caution Can Lead to Family Disputes and Legal Actions

The question about joint accounts after the death of one of the holders is more common than one might think. Many people believe they can continue to move the money freely, but lack of knowledge about legal rules can create serious problems with heirs, including lawsuits.

According to the channel Law in Focus with Camila, there are two types of joint accounts — solidary and non-solidary — and each has different consequences in case of death. Understanding this difference is essential to avoid family disputes and legal wear and tear.

Difference Between Solidary and Non-Solidary Joint Accounts

The solidary joint account allows independent movement by the holders.

-

Banco do Brasil sues famous influencer for million-dollar debt and intensifies debate on delinquency, risks of seizure, and direct impact on Gkay’s credibility.

-

The Senate approves a bill that criminalizes misogyny, hatred, or aversion towards women, and includes the crime in the Racism Law with a penalty of up to 5 years.

-

Chamber Approves Bill That Allows Pepper Spray for Women Over 16 and Imposes Strict Rules for Purchase, Possession, and Use as Self-Defense

-

Chamber Approves Law to Combat Leucaena, Fast-Growing Plant That Dominates Land and Threatens Native Species in Various Regions of the Country

This means that, during their lifetime, any of the account holders can withdraw or transfer amounts without needing the other’s authorization.

On the other hand, the non-solidary joint account requires the signature of all holders for any transaction, making it more restrictive.

In the event of death, the distinction is crucial. If the account is non-solidary, the funds can only be released through probate or a court order.

This process ensures that heirs have legal and organized access to the estate.

Can I Move a Solidary Joint Account After Death?

In a solidary joint account, the surviving holder can continue to move the funds, but with a significant risk: by law, half of the balance automatically belongs to the deceased and must be included in the probate.

In other words, even if you have access to the full amount, you can only safely use the portion corresponding to your right.

If you withdraw more than what is due to you, the heirs can legally demand the return of the withdrawn amount.

Practical Example of How Heirs Can Contest

Imagine a joint account with a balance of R$ 1 million.

According to the legal rule, R$ 500 thousand belongs to the surviving holder and the other R$ 500 thousand must be allocated to probate.

If the surviving account holder withdraws the entire amount without including half in the succession process, the heirs may file a lawsuit to reclaim their share.

According to Law in Focus with Camila, this is more common than one might think.

Many families come into conflict precisely because there was a lack of clarity in the management of money after the holder’s death.

How to Act Correctly in These Cases?

Experts recommend always formalizing the allocation of money in probate.

Even in a solidary account, where there is freedom to withdraw, the ideal is to separate the amount that belongs to the deceased and ensure that it is shared among the heirs.

Improper movement of the joint account can lead to not only civil actions but also accusations of bad faith.

Therefore, the guidance is to seek legal assistance as soon as the death occurs, to avoid erroneous decisions and family litigation.

Is It Worth Having a Joint Account?

A joint account can facilitate financial management for couples and families, but it also brings risks in case of death.

Before opening this type of account, it is important to evaluate whether the practicality outweighs the possible legal issues.

Experts indicate that, in many cases, other asset solutions, such as wills or specific powers of attorney, may be safer than simply having a joint account, especially when there is a risk of conflict among heirs.

Moving a joint account after the death of one of the holders can lead to serious lawsuits and family disputes.

The rule is clear: part of the balance must be allocated to probate, even if the other account holder has access to the account.

Have you gone through this situation or know someone who faced this problem? Do you think a joint account is truly worth it or is it a trap for heirs? Share your experience in the comments — your opinion can help others avoid conflicts.

Seja o primeiro a reagir!