Portuguese

Portuguese  Spanish

Spanish

Popular Technology Among Brazilians Can Generate Risks: Know How to Prevent Frauds in the Contactless Payment System and Understand How This Type of Scam Works.

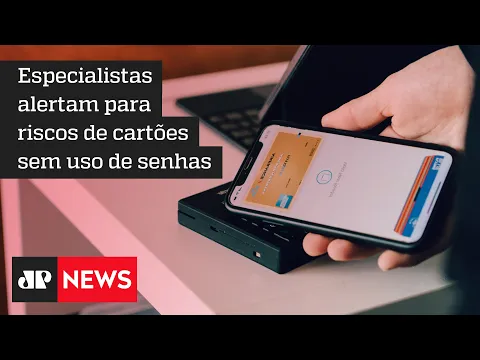

Contactless payment has gained a lot of ground due to the ease and speed it offers users when making transactions. This popular technology allows transactions to be completed without the need to insert the card or type passwords, thus ensuring a faster shopping experience. However, the contactless payment system also brings some challenges, particularly regarding the security of users’ financial data.

How Frauds Occur in Payments

With the growth of the contactless payment system, issues of vulnerability to fraud have gained prominence. The growing popularity has been accompanied by an increase in attempts to exploit potential flaws in the system, making security a priority for both users and retailers.

Fraudsters often attempt to compromise the security of this popular transaction technology by manipulating payment terminals. A common method involves the installation of devices or software that intercept signals from cards.

-

Brazilian Joins Homeownership Consortium, Faces Decade of Dual Payments Totaling $141,000, Surpassing Traditional Mortgage

-

Helicopter Drops 180 Tons of Sand and Gravel on Swedish River to Revive Ecosystem Damaged by Decades of Exploitation

-

Brazilian Company Launches Retro Smartphone with 48 MP Camera, T9 Keyboard, and Privacy Features for Social Media-Free Use

-

Self-Taught Chinese Farmer Builds 5-Ton Submarine from Scrap, Launches It in Anhui River

The main methods of fraud in the contactless payment system include the use of fake readers that capture card information, interference with terminals to divert data during transmission, and cloning cards using intercepted electronic information.

There are several measures that can be taken to increase the security of contactless payments. One of them is regular monitoring of banking activities through mobile apps, which allows users to quickly detect unusual activities. These precautions may include: setting alerts for each purchase made, using physical protections for the card that block unauthorized reading, and immediately reporting any unknown transactions to the bank.

Safer Contactless Payment System by Retailers

Retailers also play a vital role in ensuring that their contactless payment system is protected against fraud. This involves not only regular maintenance of terminals but also training employees to spot suspicious activities.

Implementing these practices includes regularly applying security updates directly from trusted suppliers, monitoring and restricting access to terminals to prevent unauthorized tampering. It is also essential to provide periodic training on new fraud techniques and financial security.

The rapid evolution of popular technology demands constant updates on security methods from both consumers and merchants. Staying informed about the latest threats and available technologies allows for more effective implementation of preventive measures.

Thus, workshops and training focused on security have become essential tools for reducing risks. With collaboration among parties involved in the payment chain, it is possible to create a safer environment, reducing vulnerabilities and ensuring that contactless payments remain reliable and efficient for all users.

Growth of the Contactless Payment System

The technological revolution and growing digitalization have significantly impacted the payment methods sector. In the Payment Methods statistics released by the Central Bank (BC), a progressive increase in the use of digital payment instruments by the population is noted. In the latest data collected by the BC, released in early June and referring to the year 2023, a new payment method has been increasingly utilized by the population: contactless transactions.

According to a survey by the BC, the percentage of credit card transactions made through contactless methods has significantly increased in comparison to other forms of capture (magstripe, chip, and non-presential) from 23.1% to 31.1% in transaction volumes over the last quarters of 2022 and 2023.

-

-

-

-

8 people reacted to this.