Portuguese

Portuguese  English

English  Spanish

Spanish

Understand How Consumer Financing in Brazil Reveals Hidden Connections Between Industrial and Financial Capital, Directly Impacting the Consumer and Showing How the Credit System Can Influence the Market and the Economy of the Country in an Amazing Way.

Consumer financing in Brazil hides a little-understood dynamic, yet it reveals how the financial system profits from the consumer’s desire to buy before having the money on hand.

According to economist José Kobori, in his participation on the Flow Podcast, financing causes the consumer to pay much more for what they buy, benefiting the financial sector at the expense of industrial production.

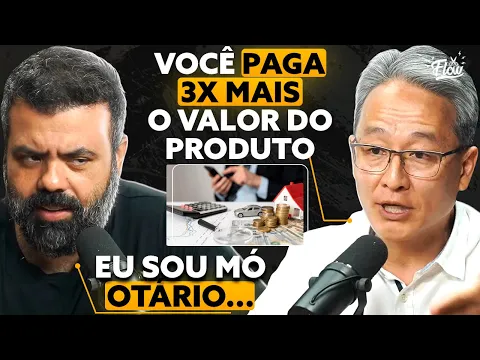

“I produce a microphone, you finance it in 24 installments, and in the end, you pay for three microphones.

-

Hotel Nacional connects the colors of Brazil on the Rio waterfront, transforms Oscar Niemeyer’s facade into a giant postcard, and makes even those passing by São Conrado look twice.

-

Ancient footprints in the Bàsura Cave reveal how a human group and a dog illuminated deep tunnels with pine branches.

-

In Florianópolis, a community with just over 40 families lives without buses or mail service, preserves mills, distilleries, and centuries-old farms, and reveals a rural side of the Island of Magic that many people don’t even imagine exists.

-

The GPS signal disappeared in large areas of the planet, and this alarmed experts, but a study analyzed events and placed Russian early warning satellites at the center of the investigation.

The manufacturer received one, while the financial sector pocketed two,” Kobori illustrated clearly.

The economist, who is also a writer and finance professor at IBMEC, took the opportunity in the conversation to expose the contradictions of Brazilian and global capitalism.

For him, financing is the link that connects “industrial capitalism,” which manufactures tangible goods, to “financial capitalism,” which capitalizes future consumption with high-interest rates.

This relationship reflects an economic model that prioritizes financial profit over real production, resulting in imbalances that affect the end consumer.

From Practice to Company Mergers

José Kobori shared his journey that took him from informal trade on the streets of Brasília to an executive position in major companies, passing through steel and copier sales until reaching the mergers and acquisitions (M&A) market.

This experience, according to him, is fundamental to understanding the real processes of companies, unlike many analysts who study only cold numbers without knowing the daily operations of the industry.

“A seller’s dream is to negotiate increasingly complex deals.

I moved from toys to copiers and now I sell entire companies,” Kobori recounted.

This practical perspective is reflected in his critique of financial experts who, in his view, are unaware of the real functioning of companies.

“Those who have never worked on a production line know little about the soul of a business,” he stated, pointing out that this disconnection contributes to wrong decisions and market bubbles.

The Shock Between Financial Capital and Industrial Capital

Kobori outlined a historical panorama that begins with the Industrial Revolution and reaches the current scenario of global financialization.

In industrial capitalism, he explains, the production of goods generates wealth but also limits wages and pressures suppliers and taxes to increase profit margins.

This process creates a contradiction: workers and consumers end up without enough income to purchase the products they helped to manufacture.

It is at this moment that financial capital appears, offering easy but expensive credit.

“Desire for consumption is financed with interest; profit is produced by those who produce nothing,” Kobori summarized, warning that the increase in credit masks social inequalities and expands financial dependence.

This phenomenon is visible in Brazil, where personal credit grows even amid rising interest rates, reflecting consumer behavior that often does not calculate the real cost of financing.

The Critical Role of Analysts and the Reality of Companies

The economist emphasized that many financial analysts rely solely on numerical data, ignoring aspects such as corporate culture, production processes, and governance.

This limited view, according to him, fuels misguided decisions and fosters speculative bubbles.

“Evaluating a company without understanding its operations is an enormous risk,” Kobori warned.

He explained the due diligence process in mergers and acquisitions, where the buyer performs a real “X-ray” of the company, seeking to uncover hidden liabilities or issues that may jeopardize the business.

Cases of controllers who are unaware of financial or strategic details are frequent, and this lack of management can collapse the value of the company post-purchase.

Financial Education to Escape the Traps of Interest

To combat the vicious cycle of expensive financing, Kobori advocates for the popularization of financial education.

Understanding personal cash flow, knowing how to differentiate wants from needs, and understanding basic investment concepts are essential tools to avoid indebtedness.

“Saving before consuming breaks the cycle of always paying more,” he highlighted.

Moreover, he advises consumers to stay updated with the financial statements of publicly traded companies to understand where the profit margin embedded in products and services goes.

This practice helps raise awareness about the real price paid in the market and can influence more responsible consumption choices.

Easy Credit, But High Cost

The economist also drew attention to the advertising that encourages long installments as if they were simply easy options.

However, what seems “affordable” hides the total effective cost (CET), which can double or triple the final price of a product.

Typical examples include smartphones, automobiles, appliances, and even courses financed in dozens of installments.

“The problem is not using credit, but being unaware of the real price of time,” Kobori warned, emphasizing that consumers pay dearly precisely because they do not understand the impact of compound interest over time.

Technology as an Ally of Conscious Consumption

As the conversation drew to a close, Kobori expressed moderate optimism when asked if there is hope for a balance between production and finance.

According to him, technology cheapens access to information, and those who are willing to learn can dodge financial traps.

“The generation that grows up listening to podcasts and consuming educational content has more tools to make conscious choices,” he concluded.

This reflection suggests that the dissemination of financial knowledge can transform consumer behavior and, hopefully, redefine the relationship between production and credit in Brazil.

Do you believe that financial education can truly change how Brazilians deal with financing or is this reality difficult to reverse? Leave your opinion!

Be the first to react!