Portuguese

Portuguese  Spanish

Spanish

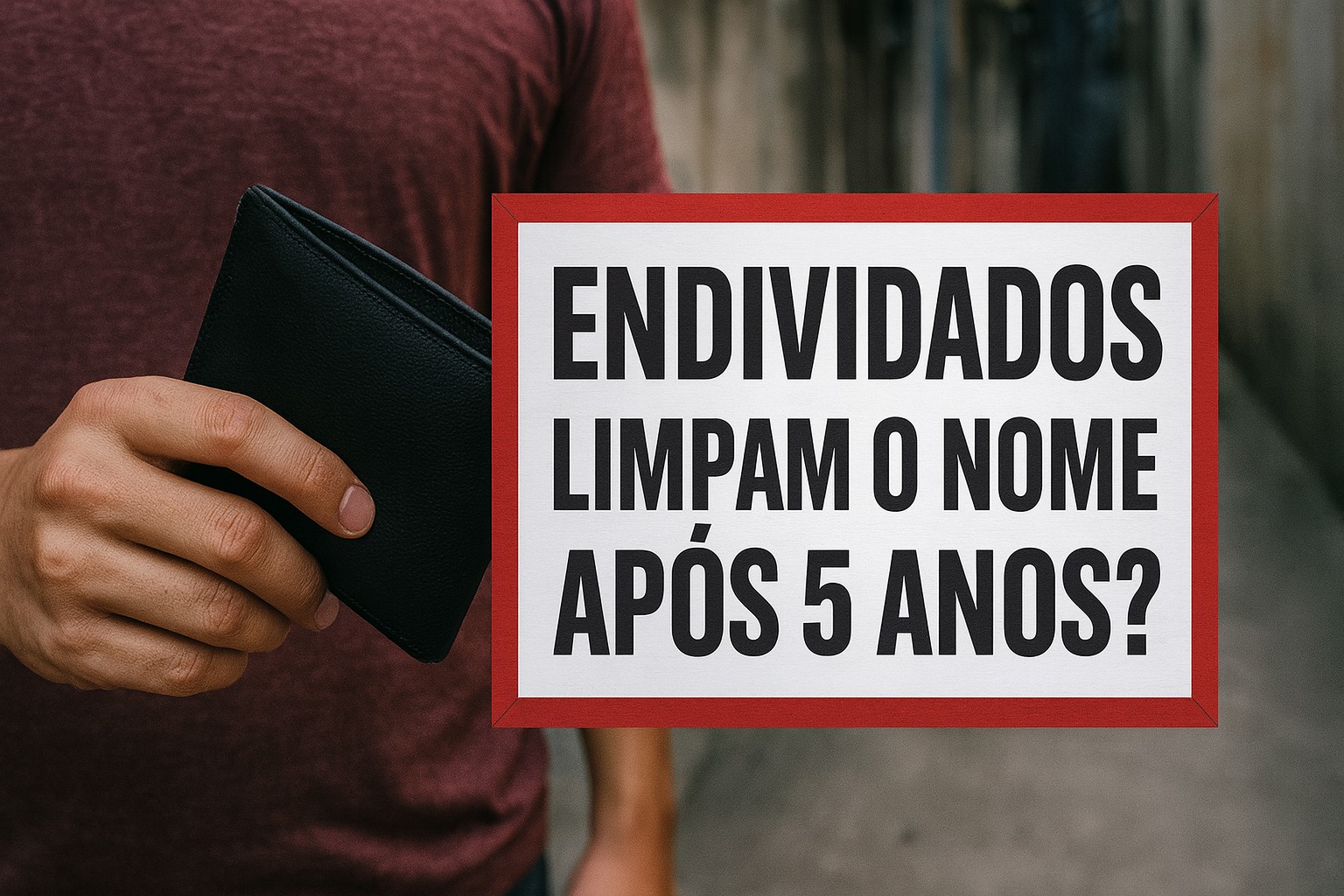

Old Debts Do Not Disappear After Five Years; Understand What Prescription, Expiration, and the Consequences of Remaining with a Negative Name Mean

One of the main doubts of consumers with negative credit is what happens to a debt older than five years, the so-called “expired debt.” It is important to clarify that, even after this period, the debt can still be collected. Therefore, the debt does not disappear automatically and continues to exist until it is paid.

Contrary to what many people think, a debt does not erase itself after five years. It simply can no longer be collected through legal means, but the creditor can still make attempts to reach an agreement.

Therefore, avoiding default is essential. If it occurs, seeking a quick negotiation can reduce interest and bring peace of mind.

-

Owner of Havan Visits Paraguay to Discuss Lower Taxes, Local Suppliers, and International Expansion with President

-

Brazilian Construction Retail Chain Closes After 60 Years, Begins Liquidation Sale Across Five Cities

-

Brazil Approves Landmark Bill Requiring Workplace Adaptations for Autism Inclusion

-

Brazil’s Micro-Entrepreneur Program May See Major Changes: Income Cap Could Increase to R$ 130,000, Annual Inflation Adjustments, and Allow Hiring of an Additional Employee

Next, check the practical implications of having a debt older than five years in your name.

Can a Debt Be Collected Through Legal Means After Five Years?

This is the question for many consumers. The answer is no. Debts older than five years can no longer be legally collected. This happens because the statute of limitations takes effect.

The statute of limitations for debt is the time limit that the creditor has to take legal action and demand payment. Once this period has passed, the creditor loses the right to collect the debt through judicial means.

In most cases, this period is five years. It applies to credit cards, loans, financing, medical agreements, and purchases made in stores through bank slips. The countdown begins from the due date.

Therefore, if the creditor does not file a legal action within this period, the debt will be considered expired.

And What If There Is Negotiation?

The statute of limitations can be interrupted in some situations. This occurs, for example, when the creditor and debtor establish a new agreement.

Imagine that the consumer has a credit card debt. The bank offers an installment plan with lower interest and an extended period.

The debtor accepts and signs this contract. In this case, a new obligation is created, with new terms.

Therefore, the five-year period starts to count again from the date of the new contract. This detail is very important for those looking to renegotiate old debts.

Debts That Can Be Collected After 5 Years

Although most debts expire in five years, there are exceptions. Some types of debts have different statute of limitations.

See Clear Examples:

- 1 year: insurance debts and hotel or inn accommodation debts.

- 2 years: alimony debts and labor debts.

- 3 years: rental debts and promissory notes.

In other words, not all debts follow the same five-year rule. Each type of debt has a time frame defined by law.

Difference Between Expiring and Expiring

Many people confuse the terms “expire” and “expire.” They are not synonyms.

A debt can only be collected when it expires, that is, when the legal time period passes without the creditor taking judicial action.

The expression “expired debt” is popular, but it does not mean that the obligation disappears. The debt continues to exist, even without the possibility of judicial collection.

Therefore, not paying for five years does not eliminate the problem. The consumer’s name may remain in negative status, and financial difficulties may continue.

Consequences of Having a Negative Name

The most important aspect of understanding this topic is to realize the practical consequences of being in negative status. Those with a negative name face restrictions that affect their daily lives.

Among the main ones are:

- difficulties opening a bank account;

- inability to acquire credit cards;

- restriction when requesting loans (in some cases, credit is available for those with negative status, but with very high interest rates, which can lead to more debts);

- barrier to contracting telephone lines, landlines, or mobile;

- difficulties making purchases on credit;

- impediment to financing assets, such as real estate or vehicles;

- restriction on participating in consortia;

- obstacles to signing contracts with service providers;

- even issues obtaining entry visas to some countries.

Therefore, in addition to the discomfort of dealing with an old debt, a negative name directly impacts the consumer’s quality of life and opportunities.

How to Know If You Are in Negative Status?

The simplest and most official way to check if your name is negative is by consulting credit protection registries.

The consumer can access the website of SPC (Credit Protection Service) or Serasa, using their CPF. These platforms inform whether there are debts registered in their name.

Another, less pleasant way is to discover it in practice. For example, when trying to open a credit account, request a loan, or even hire a service. A denial in these situations may indicate the existence of financial issues.

How to Clear Your Name

The definitive solution to this problem is to pay the debt. After settling the debt, the creditor removes the delinquency record. The name goes back to being clean, and the consumer regains access to financial services.

With the CPF regularized, it is possible to open a current account, request credit, finance assets, and resume a healthy financial life.

The Importance of Resolving the Problem Early

The longer the debt remains open, the greater the interest and complications.

Even though there is no judicial collection after five years, the debt will continue to exist and bring restrictions.

Therefore, resolving it quickly is always the best way forward. Negotiating can generate significant discounts and reduce charges. In addition, it gives the consumer peace of mind to plan for the future.

Does the Name Clear After the 5-Year Period?

According to Brazilian law, the debt does not disappear after five years, but the record in credit protection agencies should be removed within this timeframe, according to the Consumer Protection Code.

This means that the consumer’s name goes back to being clean, even if the debt has not been paid. However, the debt continues to exist and can be collected extrajudicially.

Therefore, the consumer regains access to credit but still has the moral and financial obligation to pay the owed amount.

In summary, debts older than five years do not disappear. They can no longer be legally collected but continue to exist.

The creditor may attempt negotiations, and the debtor may face serious restrictions by remaining in negative status.

Therefore, the expression “expired debt” should not mislead the consumer. The debt does not disappear on its own. Resolving the outstanding issue is essential to regain financial health, access credit again, and avoid further complications in the future.

With information from Jornal Contábil.

Matéria mal escrita. O STJ já tem definido que até de forma extrajudicial não pode cobrar após a prescrição. E não, uma dívida não pode permanecer em nenhum cadastro, mesmo no SCR. Se ocorrer o devedor por entrar na justiça para retirá-lo. O Direito não socorre a quem dorme, o credor deve entrar na justiça para que a prescrição não ocorra.