Portuguese

Portuguese  Spanish

Spanish

How To Divide A Salary Of R$ 3 Thousand Simply: See How Much To Allocate For Fixed Expenses, Leisure, Emergency, And Investments.

With the cost of living rising and the budget tight, understanding how to divide a salary of R$ 3 thousand can make all the difference at the end of the month.

The proposal below presents a practical division that can help with financial organization, highlighting fixed expenses, variable expenses, and the beginning of building an emergency fund.

The strategy follows a simple logic. First, separate the essentials, such as bills, groceries, and rent. Then, anticipate the expenses that vary each month.

-

From a 12-square-meter room to leading a $4.8 billion fuel empire with over a thousand stations

-

El Niño Threatens Brazilian Food Production, Economists Predict Rising Prices for Coffee, Corn, and Rice

-

Brazil’s First Freight Railway Built from Scratch, EF-118 Connecting Espírito Santo to Rio de Janeiro, Goes to Auction in October Attracting Chinese Giant in Multi-Billion Dollar Bid for Southeast Rail Network

-

Audit in Rio de Janeiro’s State Government Uncovers Ghost Employees Across All 77 Departments, Leading to Over 4,000 Dismissals and Significant Cost Savings

Finally, allocate a portion, even if small, for the future. This includes an emergency fund and, subsequently, investments.

Fixed Expenses: The Biggest Burden On The Budget

The majority of the salary should be dedicated to fixed expenses. These are the expenses that do not change frequently and are essential for daily maintenance.

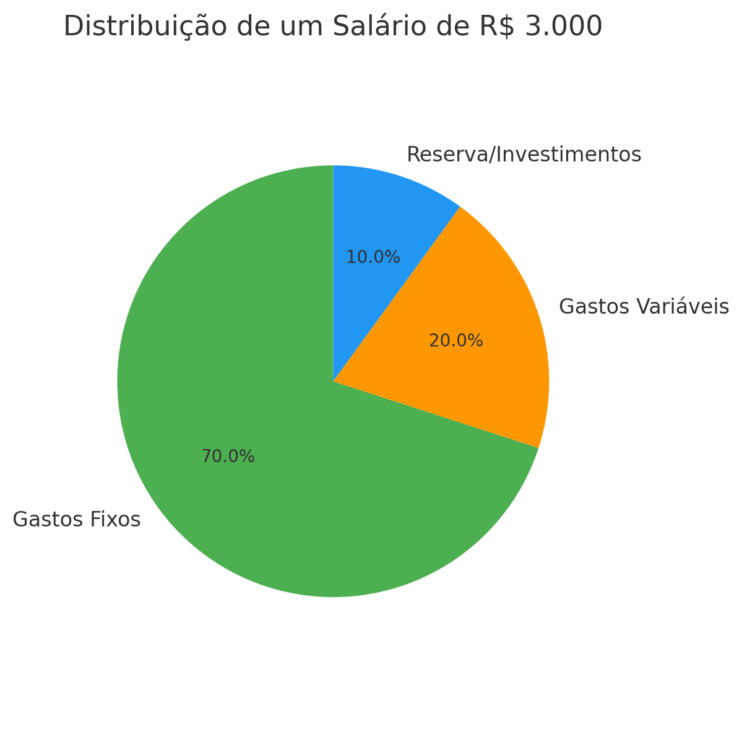

In this example, the recommendation is to use 70% of the salary, which equates to R$ 2,100, for these expenses.

This category includes utility bills, rent, transportation, groceries, and other monthly commitments that cannot be avoided.

These are expenses that require priority and often have a defined due date. For this reason, they need to be at the top of the list.

Even if it seems heavy, allocating this amount helps ensure stability. Knowing that this part is committed makes it easier to see what is left and plan other expenses more clearly. It is the foundation to avoid going into the red before the end of the month.

Variable Expenses: What Changes Each Month

The second part of the budget involves what are called variable expenses. In this example, they account for 20% of the salary, or R$ 600.

Here, the expenses related to leisure, streaming services, and also the so-called “frivolities” — impulse purchases, outings, meals outside the home, among others, come into play.

These expenses are important for maintaining quality of life and well-being, but they need to be controlled.

Without limits, they can compromise the budget and hinder the formation of a reserve or the payment of essential bills.

This group also includes unplanned expenses. An unexpected repair, a medical appointment outside the plan, or any emergency that requires a quick outlay.

For this reason, even though they are variable, these expenses should be closely monitored. A good tip is to write down everything spent in this category to avoid surprises at the end of the month.

Emergency Fund And Investment: Thinking About The Future

Finally, the 10% remaining of the salary, which corresponds to R$ 300, should be allocated to building an emergency fund. This is the step that many people overlook, but it makes all the difference in the medium and long term.

The emergency fund acts as a financial cushion. It is used to cover unforeseen events without resorting to loans or debt.

It can be a layoff, a health problem, or any situation that affects income or requires an immediate expense.

The guidance is to start slow, with what is possible, and maintain regularity. The accumulated amount should ideally reach a total that covers three to six months of fixed expenses. In the case of this example, it would mean saving between R$ 6,300 and R$ 12,600.

Only after completing this reserve can the R$ 300 per month be redirected to investments. The aim here is to make the money work, creating new sources of security for the future. It is at this stage that one begins to discuss financial applications.

The Importance Of Control

Even though it is just an example, this salary division model helps create a starting point. The proposal here is clear: understand where the money is going. Each person has a different reality, but the concept applies to any salary range.

Knowing how much is spent on bills, how much goes to leisure, and how much can be saved is the first step towards a balanced financial life. Many do not know exactly how much they spend on apps, dining out, or small purchases, which impairs overall budget control.

Another important point is to have discipline. It is of no use to set up a spreadsheet or follow an ideal division for just one month. Control must be continuous. Small habit changes, such as avoiding impulse purchases and canceling rarely used services, already help maintain balance.

Personalization Is Essential

Each reality requires adjustments. It will not always be possible to strictly follow the 70%, 20%, and 10% division. The important thing is to understand the logic and adapt according to needs and possibilities.

There are months when variable expenses may be lower, creating room to save more. In others, emergencies may require adjustments.

The most relevant thing is to be aware of each expense. The proposed division serves as a simple reference that can be adapted. The important thing is to keep an attentive eye and seek balance, without neglecting leisure, but also without compromising the future.

Knowing how to manage a salary of R$ 3 thousand is not just a matter of numbers. It is an exercise in awareness and responsibility.

Even with little, it is possible to start building a reserve, avoid debt, and improve the relationship with money. And it all starts with a simple question: where is my money going?