Portuguese

Portuguese  Spanish

Spanish

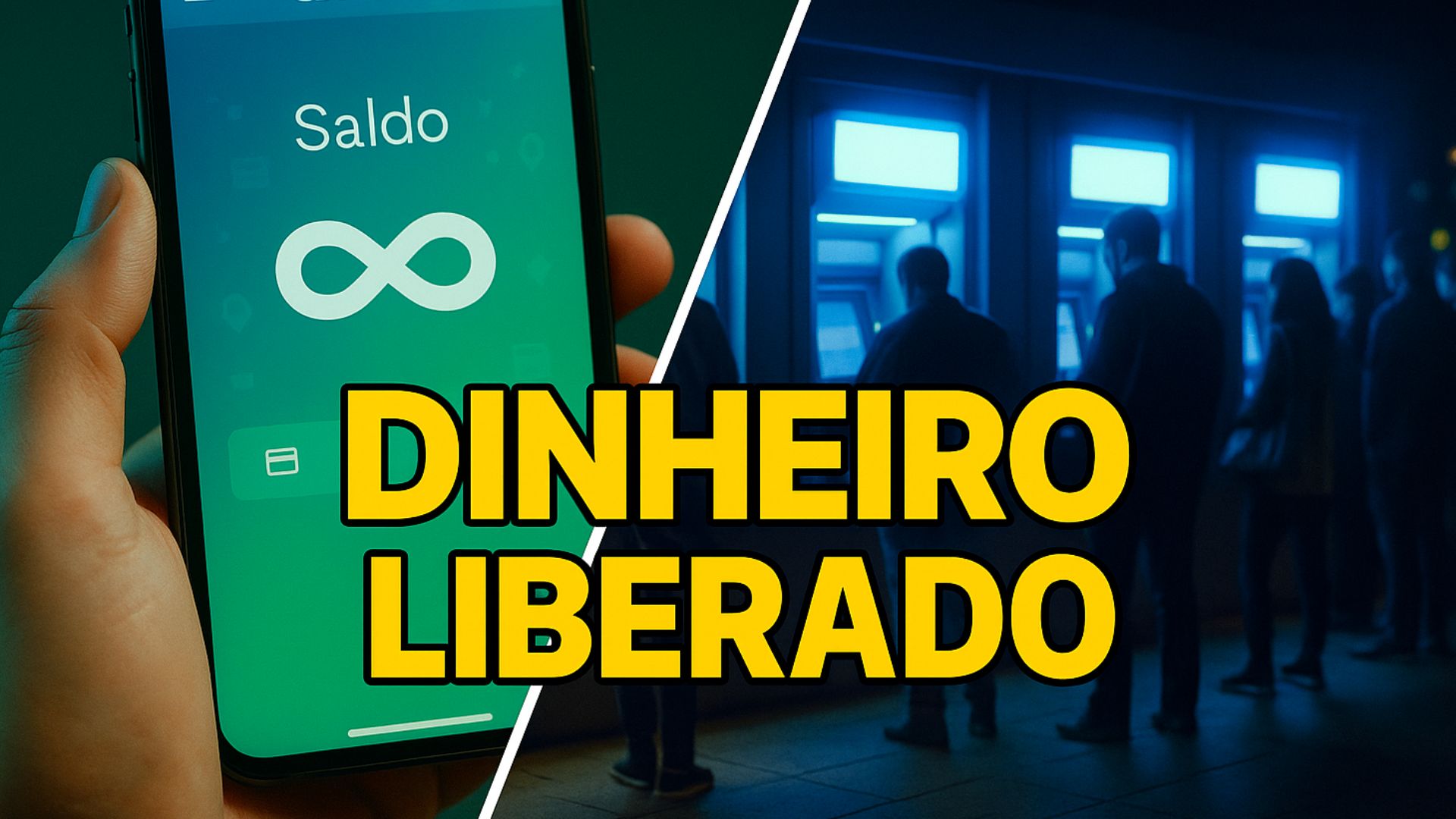

A failure in the Bank of Ireland app allowed customers to withdraw money beyond the available balance, causing lines at ATMs and police action to contain the movement in the streets.

When a digital glitch meets popular curiosity, the result can spiral out of control.

That’s what happened with the Bank of Ireland app, whose instability opened, for a few hours, a rare gap: customers were able to move money above their balance and beyond normal limits.

The news spread on social media, lines formed at ATMs, and the police were called to monitor the movement at branches and terminals.

-

Former Atacadão Employee Turns Online Cake-Baking Lessons into a Confectionery Brand with Factory, Store, Delivery, and Nearly $400,000 in Revenue

-

Brazilian Startup Sells Nearly 9 Million Surprise Bags of Near-Expiry Food, Prevents Thousands of Tons of Waste, Aiming for $42 Million Revenue by 2026

-

How to Prevent Brown Recluse Spider Bites: Common Hiding Spots and Free Tips to Reduce Risks

-

Natto: The Unusual Japanese Superfood Gaining Popularity on Social Media and Driving Record Exports

What Happened and Why It Caught Attention

There was a technical failure in the bank’s app and internet banking that allowed unauthorized transactions.

During the instability period, users reported transfers “above their normal limits” and in-person withdrawals, even with insufficient balance.

The combination of mistakenly approved transactions and the viral spread of videos boosted traffic to ATMs in different cities.

As soon as the Bank of Ireland noticed the anomaly, it released statements reiterating the central guidance: everything that was transacted would be debited later from the accounts.

Meanwhile, the Garda, the Irish police, reported being aware of the “unusual volume of activity” and maintained a preventive presence to ensure order in areas with high demand.

How the Operational Gap Worked

The inconsistency occurred in the real-time limit synchronization between channels.

Under normal conditions, the system cross-checks balance, transaction ceiling, and customer history to block what exceeds the permitted amount.

On the night of the glitch, part of these controls failed sequentially: there were attempts through the app, approvals outside the standard, and then, accounting compensation with debits from the account.

Reports indicated two main paths.

In one, customers were able to withdraw up to 500 euros directly using their cards at ATMs.

In another, the strategy was to transfer amounts to accounts in other institutions or digital wallets and then make withdrawals of up to 1,000 euros at terminals.

In both cases, the bank stressed that the amounts would be charged according to the usual debit rules.

What the Bank Said and How the Police Acted

The institution classified the episode as a “glitch” and apologized for the unavailability of some digital services throughout the night, claiming that normalization was gradual in the following hours.

In all notes, it repeated the key point: there was no “free money” and the transactions would be debited as soon as the systems stabilized.

For customers facing payment difficulties, the guidance was to seek assistance to negotiate terms.

On the public safety side, the Garda described the situation as atypical but under control.

Patrols were deployed to high-traffic areas, especially after the rise in lines and gatherings.

There was no announcement of widespread blocking measures, but rather monitoring and targeted actions to preserve order.

Instability, Normalization, and Messages to Customers

As traffic increased at ATMs, many customers also faced slowness or access fluctuations in the app and internet banking.

The restoration was communicated in stages, with alerts that residual instability in the app might persist.

In practice, the official recommendation remained the same throughout the day: any amount withdrawn or transferred during the failure window would appear as a debit on the account of the holder.

The bank informed the economic authorities and the financial system supervisor about the incident.

The public exposure of the problem reopened debates about operational resilience and contingency plans in the banking sector, particularly in situations where technical failures create incentives for herd behavior.

After the Rush, Came the Settlement

As compensations and reconciliations progressed, the Bank of Ireland adopted an additional measure: it extended the deadline for customers to regularize unauthorized overdrafts generated during the failure.

The offer of three additional months for settlement was presented as a way to reduce the impact on customers and avoid a concentration of defaults in the short term.

This was not a forgiveness but rather financial accommodation for those who ended up with a negative balance due to the unauthorized approvals.

Without publishing consolidated figures of those affected or the total amount involved, the institution kept the communication focused on three axes: normalization of services, subsequent launch of debits, and support channels for negotiation.

The reiterated official recommendation was clear: those who found themselves in the red after the glitch should contact the bank to discuss adjustment alternatives.

What Makes the Case Instructive for the Public

For the consumer, the episode sends a direct message.

Withdrawals and transfers approved due to a technical error do not equate to extraordinary credit.

They are inconsistencies that, once corrected, reappear as debits in the statements.

The attempt to exploit gaps can lead to negative balances and additional costs, such as interest and fees, if there is no negotiation.

From a technical standpoint, the case highlights a sensitive point in banking systems engineering: ensuring that limit rules and anti-fraud checks function consistently across the app, internet banking, and ATM networks, even under peak demand or intermittencies.

It also reveals the importance of clear and timely public messaging to reduce misunderstandings that encourage unnecessary trips to branches and terminals.

Crisis Lessons: Communication and Tactical Blocks

In critical incidents, banks tend to combine immediate communication with tactical blocks on higher-risk operations.

This dual approach helps contain the expansion of atypical transactions while technical teams work on corrections.

In the case of the Bank of Ireland, the strategy included successive alerts, reinforcement of guidance on future debits, and police presence for traffic management in areas with lines.

Although there is no “one-size-fits-all manual” for all glitches, the experience shows that coherence between channels, real-time monitoring, and coordination with authorities are central elements to reduce damage.

Transparency about what will be charged and how to negotiate any negatives tends to lessen noise and prevent the narrative of “free money” from gaining traction.

And For Those Who Saw the Lines?

Those who followed the images of crowded ATMs only saw the most visible face of the problem.

The less apparent process involved compensations and transactions that, over the following hours, recalculated balances and reversed unauthorized approvals.

At the end, this meant the arrival of debits and, in some cases, the need for agreements to restore account balance.

The curiosity continues: in situations like this, what is more effective in preventing the multiplication of unauthorized withdrawals and transfers — immediately reinforcing transactional blocks or first investing in clear public communication to discourage rushing to the ATMs?

Hey there You have done a fantastic job I will certainly digg it and personally recommend to my friends Im confident theyll be benefited from this site