Portuguese

Portuguese  Spanish

Spanish

Research Reveals That 69% of Brazilians Split Purchases and 42% Use Their Card Weekly. Understand the Risks and Changes in Consumer Behavior.

The credit card has stopped being just a payment tool for larger purchases and has become central to Brazilian households’ budgets. According to a recent survey by Fiserv, 69.3% of consumers in Brazil split their purchases and 41.7% use their card at least once a week, revealing an increasing level of reliance on this payment method.

This data is not surprising when considering the economic scenario: accumulated inflation in recent years, high cost of living, and difficulty in maintaining purchasing power have turned the credit card into an extension of monthly income.

Installment Payments as a Consumption Standard

The habit of splitting purchases has consolidated in Brazil to the point of being viewed as something “natural” for most consumers. Among card users, nearly 7 in 10 choose to divide the value of their purchases, even for low-value items.

-

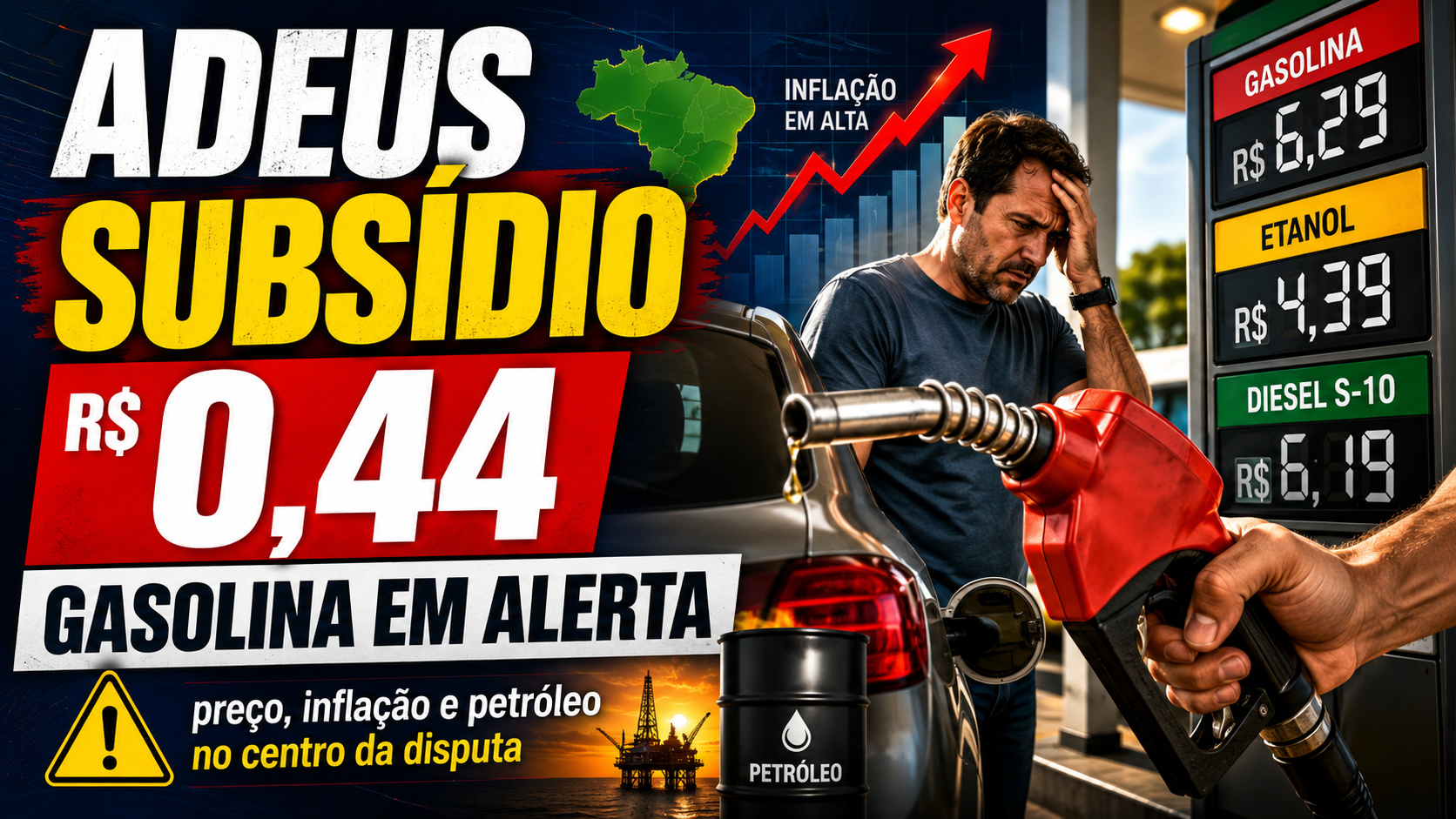

Brazil to Phase Out Gasoline Subsidy, Fuel Prices Set to Rise Amid National Debate

-

Brazil Aims to Boost Critical Mineral Production to 12.2% of Global Output, Targeting Battery and Tech Industries

-

Brazil’s New National Mining Plan Aims to Transform Fertilizer Market and Reduce Foreign Dependency from 87.3% to 34.9%, Boosting Agriculture and Food Production

-

Brazilian Government Plans to Auction Over 500 Road Bridges on São Paulo Stock Exchange in 2026, Promising New Wave of Concessions

Personal finance experts point out that when used in a planned manner, installment payments can be a useful tool for organizing the budget.

However, the frequency and number of simultaneous installments increase the risk of losing control over finances, especially when the monthly bill already arrives compromised by past purchases.

Weekly Use of the Credit Card Reveals Behavioral Change

Another highlight from the research is that 41.7% of Brazilians use their cards weekly — and not just for high-value purchases. It is now common to find consumers using credit for recurring expenses such as grocery shopping, pharmacy visits, and even basic service bills, like electricity and internet.

This behavior is driven by cashback programs, points accumulation, and the convenience of digital payments but also reflects a scenario of financial tightness, where consumers “push” expenses to the next month as a way to maintain some immediate cash flow.

The Risks Behind Convenience

Despite the practicality, the increasing reliance on credit cards brings significant risks. The main one is the revolving credit, triggered when the consumer does not pay the total amount due. With interest rates that can exceed 450% per year at traditional banks, revolving credit turns small debts into unpayable amounts in a few months.

Frequent use of installment payments also reduces the margin for unexpected expenses since it limits credit and part of future income. Therefore, any financial surprise can quickly lead to delinquency.

The Weight of Delinquency and Worrying Data

The National Confederation of Shopkeepers (CNDL) points out that the credit card leads the ranking of debts among delinquents in Brazil: 85% of consumers with negative credit have outstanding bills related to overdue bills.

The problem is not restricted to lower-income groups. The survey reveals that middle-class families also frequently use credit cards, often as a solution to maintain their consumption patterns in the face of declining purchasing power.

Reasons for High Dependence on Credit Cards

Several factors explain the consolidation of the card as the main form of payment in Brazil:

- Ease of Access: fintechs and banks offer quick approval, often with no strict income verification.

- Reward Programs: points, miles, and cashback incentivize constant usage.

- Digital Payment Integration: contactless purchases and integration with digital wallets enhance convenience.

- Pressure on Family Budgets: with high prices, the card acts as a “safety valve” for unplanned expenses.

How to Reduce Risks of Frequent Use

Experts recommend simple practices to prevent the card from becoming a problem:

- Always pay the total bill amount by the due date.

- Limit the number of installments and avoid accumulating future commitments.

- Use credit only for planned purchases and true emergencies.

- Periodically review the available limit to avoid surprises in the budget.

The Warning for the Future of Consumption

The growing dependence on credit cards raises important questions about the future of consumption in Brazil. On one hand, it ensures immediate access to goods and services, as well as providing security and benefits that other means do not offer. On the other hand, the ease of use and high-interest rates create a scenario conducive to mass indebtedness.

While the numbers show that most Brazilians no longer view the card merely as a complement but as an essential part of their budget, the risk is that this dependence will continue to grow, exacerbating delinquency and limiting purchasing capacity in the medium term.

The question remains: is the country heading toward a consumption model increasingly based on easy and expensive credit, or will there be room for a change in habits and greater financial planning?