Portuguese

Portuguese  Spanish

Spanish

Buying a Car Through Financing Is a Common Practice in Brazil, But Involves Many Details That Go Unnoticed by a Large Part of Consumers. The Down Payment, Interest Rates, and the Payment Term Are Deciding Factors in the Final Value of the Asset. A Practical Simulation Helps to Understand How These Elements Combine and Directly Impact the Buyer’s Pocket.

A Renault Kwid financed can seem like a good option for those who do not have the full amount upfront. But attention must be paid to the interest rates and conditions.

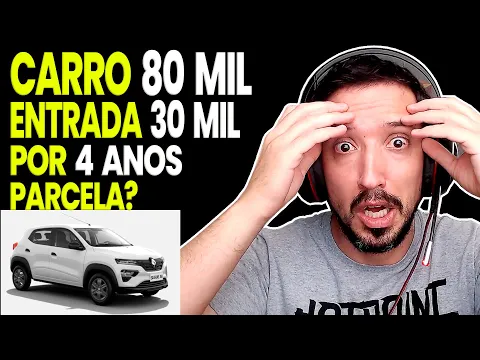

A practical example helps to better understand how these numbers work. Below, see what happens with a Kwid financed for R$ 80,000.00 with a down payment of R$ 30,000.00 over a four-year term. The simulation was made by the channel Pipoco Investidor.

Kwid Financed — Simulation with a Down Payment of R$ 30 Thousand

In this case, the value of the Kwid considered is R$ 80,000.00.

-

Man Revives 1962 Mercury Comet with Parts from a Damaged Nissan Leaf, Achieving Electric Conversion for Under $6,000

-

British Mechanics Convert Classic Land Rover Defender to Electric, Maintaining Original Look with 483 Horsepower and 75 kWh Battery

-

Chevrolet Onix Turbo AT 2020: Affordable Used Hatchback with Turbo Engine, Automatic Transmission, and Six Airbags

-

Rolls-Royce Turns Heads with 30-Inch Floating Wheels, 6.6-Liter V12 Engine, and 563 Horsepower

The down payment applied was R$ 30,000.00. This represents 38% of the total value of the vehicle, below the ideal of 40% to 50%, an amount recommended for lower interest rates.

The financing term is 48 months, or four years.

The interest rate used in the simulation is 1.8% per month. It is worth remembering that this rate can vary depending on the customer’s profile.

People with a good credit history, who pay their bills on time and do not accumulate debts, usually manage to get lower rates. Those with a low credit score generally face higher interest rates.

With these conditions, the fixed monthly installments amount to R$ 1,564.47. Over the four years, the total amount paid will be R$ 105,094.37. Of this amount, R$ 25,094.37 is solely for interest.

Impact of Interest on the Financed Kwid

The amount paid in interest represents 24% of the total financing amount.

This is nearly the amount of the down payment. This number shows how interest can weigh on the final cost of the financed car, especially when the down payment is less than 40%.

According to the simulation, if the down payment were higher, the interest would decrease considerably.

For example, with a down payment of R$ 40,000.00, the percentage of interest would drop to around 20%.

The installments would also be smaller, which would bring more relief to the buyer’s budget.

Therefore, making a larger down payment is one of the most effective ways to save on financing. The larger the initial amount paid, the smaller the financed amount, and consequently, the lower the interest.

Advancing Installments Also Helps

Another important tip is to try to pay off future installments in advance. This practice, popularly known as “paying backward,” can significantly reduce interest.

This happens because by advancing installments, the buyer decreases the outstanding balance and the contract duration, which reduces the total amount of embedded interest.

Even if the buyer does not have a very high down payment at the time of purchase, it is possible to organize over time to advance installments.

With this, the final cost of the financing can drop significantly.

The suggestion is clear: avoid spending on unnecessary things.

Focus on paying for the vehicle, and whenever possible, advance installments. This effort can represent considerable savings over the months.

Table with the result of the simulation for financing a car worth R$ 80,000.00, with a down payment of R$ 30,000.00, financed in 48 installments, with interest of 1.8% per month:

| Description | Value |

|---|---|

| Car Value | R$ 80,000.00 |

| Down Payment | R$ 30,000.00 |

| Down Payment Percentage | 38% |

| Financed Amount | R$ 50,000.00 |

| Term | 48 months (4 years) |

| Monthly Interest | 1.8% |

| Fixed Monthly Installment | R$ 1,564.47 |

| Total Paid in Installments | R$ 75,094.37 |

| Total Paid (Down Payment + Installments) | R$ 105,094.37 |

| Total Interest Amount | R$ 25,094.37 |

| Percentage of Interest on Total Amount | 24% |

Ideal Down Payment Makes a Difference

The ideal, according to the example, is to offer a down payment of at least 50% of the vehicle’s value. In this scenario, the interest burden is significantly reduced.

However, even a down payment starting from 40% already brings important benefits when negotiating with banks or financial institutions.

In the mentioned case, the down payment of R$ 30,000.00 was below this threshold, and the interest remained at 24%. With R$ 40,000.00 as a down payment, the interest rate dropped to 20%.

These four percentage points make a difference in the total amount to be paid until the end of the contract.

Organization Is the Secret

Those planning to finance a vehicle should consider not only the installment amount but the total to be paid at the end. Often, installments that seem affordable hide high interest rates and overall costs.

Therefore, it is important to evaluate the down payment amount, the payment term, and the interest rate.

Additionally, maintaining a good financial history helps to secure better conditions, with lower rates and softer installments.

Planning and discipline are essential for those intending to take on medium or long-term financing. And even after closing the contract, it is still possible to reduce costs through the anticipation of installments.

At the end of the 48 months, with a down payment of R$ 30 thousand, the total amount paid will be R$ 105,094.37.

This represents an increase of R$ 25,094.37 compared to the initial value of the car. A difference that reinforces the importance of careful evaluation before buying the financed Kwid.

It is important to highlight that the values presented throughout the article are part of a simulation based on a hypothetical scenario. The actual financing conditions, such as interest rates, installment amounts, and credit approval, vary according to each consumer’s profile and the policies of financial institutions. To obtain precise and personalized results, it is advisable to consult directly with banks, financial institutions, or authorized dealerships.

Financiamento no Brasil é uma loucura de todo tamanho. A loucura é maior que o Kwid.

Pior que a loucura é fazê-la por um kwid, que não deveria custar mais que 40k. A situação de veiculos no Brasil está absurda. Kwid mais rodado que B.surfistinha custando 60 mil. Com o novo C. Tributário vai piorar.