Portuguese

Portuguese  Spanish

Spanish

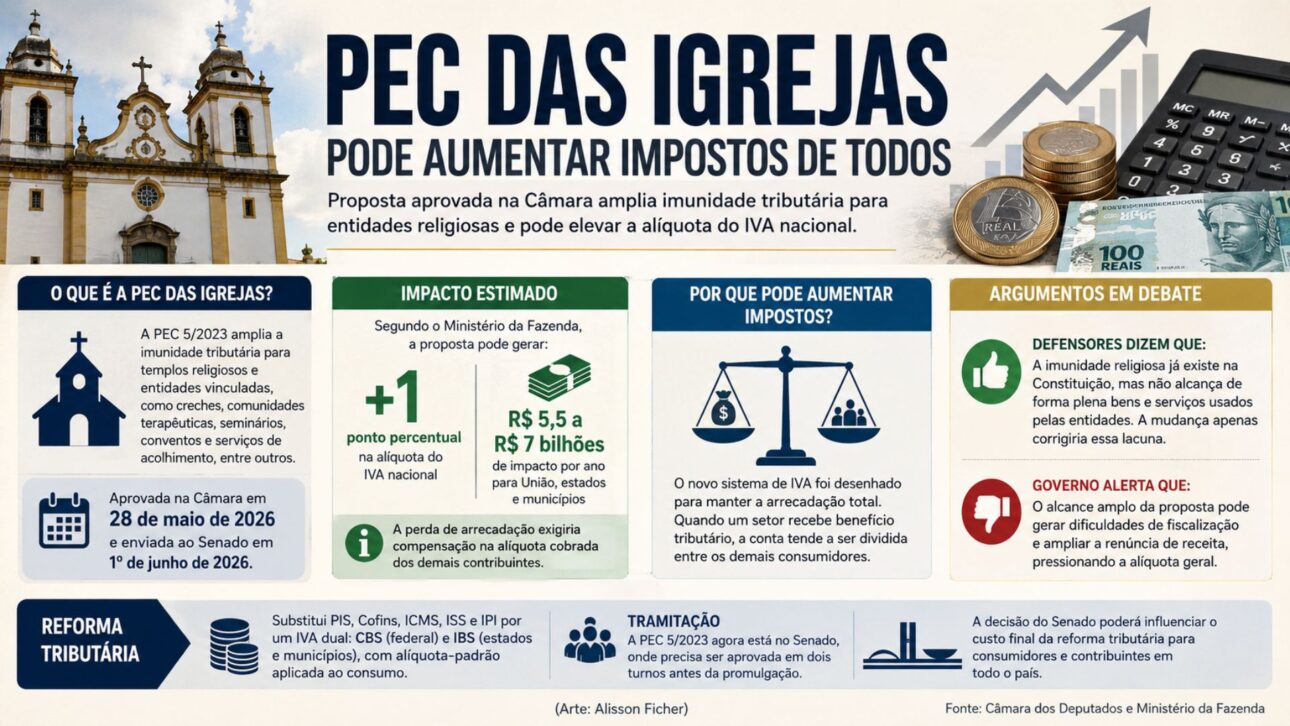

Proposal under review in the Senate expands the tax immunity of religious entities and raises the discussion on the effect of tax benefits on the new consumption system, amid the calibration of tax reform and the estimates of billion-dollar losses presented by the economic team.

The proposal that expands the tax immunity of religious entities may increase the rate paid by other taxpayers in the tax reform, according to a warning made by Finance Minister, Dario Durigan, on Tuesday (09).

According to the economic team, the so-called Churches PEC, already approved by the Chamber of Deputies, may raise the national VAT rate by 1 percentage point if also approved by the Senate.

The measure under review is PEC 5/2023, presented on March 15, 2023, which amends the Constitution to expand the tax immunity of religious organizations and institutions linked to them.

-

Brazil to Issue “Panda Bonds” in China, Aiming to Raise Up to 5 Billion Yuan at Lower Interest Rates Than Dollar Debt

-

NATO Faces Internal Tensions as U.S. Pushes for Increased Defense Spending, Targeting 5% of GDP by 2035, with Warnings for Countries Near 2% Level

-

Brazil to Introduce B16 Diesel with Increased Soybean Oil Content for Trucks by 2026

-

Brazil’s July Bolsa Família Payments May Include Extra $150 and $50 for Families with Children, Pregnant Women, and Updated CadÚnico Registration

According to the proceedings recorded by the Chamber of Deputies, the text was sent to the Senate on June 1, 2026, after being approved by the House’s parliamentarians.

Impact of the Churches PEC could reach R$ 7 billion per year

In an interview with UOL, Durigan stated that the expansion of the tax benefit would have a direct impact on the rate of the new consumption taxes created by the tax reform.

“If more benefits are approved, in this case, everyone in the country will be paying 1% more of our VAT starting next year,” declared the minister.

The estimate attributed to the Ministry of Finance indicates an annual impact between R$ 5.5 billion and R$ 7 billion for the Union, states, and municipalities, if the expansion of immunity is confirmed by Congress.

According to the economic team’s assessment, a greater waiver in a certain segment needs to be considered in defining the general rate, as the tax reform was designed to preserve total revenue.

The text approved by the Chamber provides that immunity covers goods and services related to the maintenance and operation of temples, religious entities, and charitable or benevolent organizations linked to these institutions.

Among the activities mentioned in the proposal’s discussion are daycare centers, therapeutic communities, seminaries, convents, shelter services and non-profit initiatives associated with religious entities.

Tax Reform and National VAT Enter the Center of the Debate

The tax reform replaces PIS, Cofins, ICMS, ISS, and IPI with a dual VAT model, formed by the Contribution on Goods and Services and the Tax on Goods and Services.

In the new system, the Contribution on Goods and Services will be under federal jurisdiction, while the Tax on Goods and Services will be managed by states and municipalities.

The standard rate will be broadly applied to consumption, with exceptions, specific regimes, and differentiated treatments defined in complementary legislation and in rules related to the transition.

When a sector receives differentiated treatment, according to the logic presented by the Treasury, the revenue that is not collected needs to be considered in the calculation charged to other taxpayers.

This is the point used by the economic team to criticize the expansion of benefits, as new exceptions may pressure the general rate of those not covered by exemptions or immunities.

During the vote in the Chamber, Congressman Pedro Uczai (PT-SC) stated that the change could increase the standard rate by 0.5 percentage points.

Durigan’s statement raised the alert to 1 percentage point, although the minister did not publicly detail all the technical assumptions used to reach this estimate.

Proposal Defenders Cite Constitutional Protection for Churches

Parliamentarians in favor of the PEC state that religious immunity already exists in the Constitution, but does not fully cover the consumption of goods and services used by the entities.

The author of the proposal, Congressman Marcelo Crivella (Republicanos-RJ), stated in the Chamber that the intention is to correct this gap and allow the constitutional protection to have a practical effect also on purchases made by the institutions.

In the assessment presented by Crivella during the proceedings, immunity already applies to income and assets, but does not cover all items acquired for religious, social, or assistance activities.

For the congressman, the change would not create a new privilege, but would adjust taxation to the daily functioning of temples and organizations linked to religious institutions.

Deputies who defended the proposal also cited assistance actions maintained by churches as an argument to expand the tax protection provided for in the text approved by the Chamber.

During the plenary discussion, parliamentarians stated that religious entities provide social services and that part of these activities can reduce demands directed at the public authorities.

Treasury points out risk of control and oversight

According to Durigan, the main point of concern is the scope of the proposal and the difficulty in separating which goods and services would be directly linked to the essential activities of the entities.

The minister stated that the Treasury presented alternatives to limit the effects of the PEC and reduce risks of revenue loss, without publicly detailing all the suggested measures.

The economic team considers that the approved wording may allow broad interpretations of what would be necessary for the functioning of religious organizations and institutions linked to them.

In a VAT system, this definition has a direct effect on the calculation base of new consumption taxes and on the distribution of the burden among taxpayers.

Besides the revenue impact, Durigan classified the proposal among measures that, in the government’s assessment, could pressure public accounts in a scenario of high interest rates and external uncertainties.

The minister also linked the expansion of tax benefits to the risk of increasing the perception of fiscal imbalance, an argument used by the economic team against agendas with revenue loss.

Senate still needs to analyze PEC 5/2023

The PEC awaits analysis by the Federal Senate, where it will need to go through a new vote before eventual promulgation by the National Congress.

As it is a proposed amendment to the Constitution, the text does not require presidential sanction if approved by both Houses.

The Chamber approved the proposal on May 28, 2026, and the processing record notes the formal submission to the Senate on June 1 of the same year.

Until the analysis by the senators, the scope of immunity, the fiscal impact, and the relationship with the tax reform rate should remain in the debate among the government, parliamentarians, and religious entities.

The discussion takes place during the implementation phase of the new consumption tax system, a period in which the standard rate and exceptions need to be calibrated.

The decision of the Senate may influence not only the entities benefited by the PEC but also the final cost of the tax reform for consumers and taxpayers throughout the country.