Portuguese

Portuguese  Spanish

Spanish

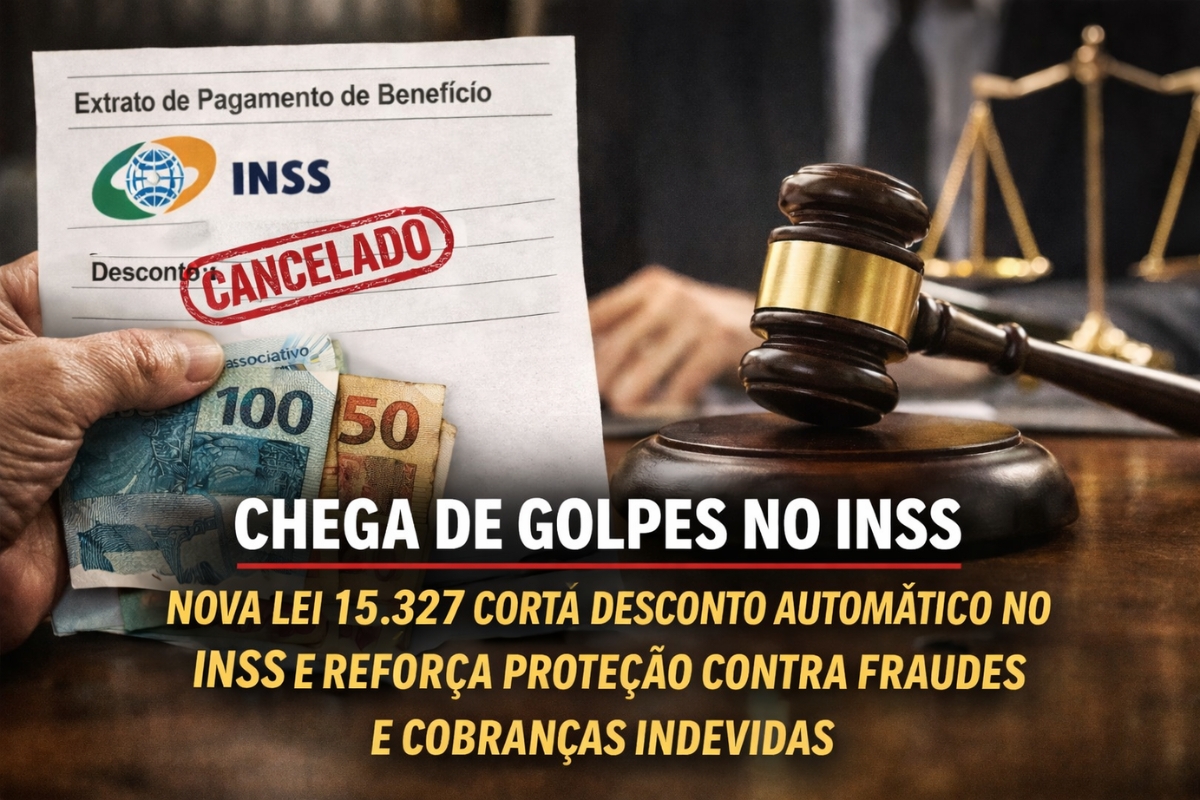

On January 7, 2026, a safeguard against automatic charges on INSS was introduced, with full refunds for irregular deductions and new requirements for consigned loans.

The president Luiz Inácio Lula da Silva enacted on January 7, 2026 the Law 15,327 of 2026, with vetoes, creating a new protection framework for retirees and pensioners of the INSS.

The main change is straightforward: the deduction of association fees from the pension benefit is prohibited, even when there is authorization from the beneficiary.

The law also strengthens accountability for undue deductions, expands tools against fraud, and imposes new layers of security on consigned credit.

-

U.S. House Approves Bill to Protect Children on Social Media, Limit Addictive Features, and Demand New Measures from Platforms, But Senate Differences Could Stall Progress

-

78-Year-Old Brazilian Farmer Wins Legal Battle for Ownership of 108,000 m² of Land After Decades of Dispute with Federal Government

-

Brazilian Supreme Court Pauses Fines for Workplace Regulation Violations for 90 Days, but Companies Must Still Address Harassment and Overwork

-

Seniors Over 60 Can Travel for Free Across Brazil: Elderly Statute Ensures Two Free Bus Seats and 50% Discount When Full for Low-Income Passengers

Associative Deductions from INSS Benefits Becomes a Prohibited Practice

The payroll of the INSS can no longer be used for associative charges.

Associations, unions, and similar entities are prohibited from making any automatic deductions from pensions and retirements.

The prohibition applies even when there is authorization from the beneficiary, ending this mode of charging within the social security system.

Those Who Wish to Maintain Association Must Pay Outside the Social Security System

Retirees and pensioners who wish to associate with an entity may continue, but through other means.

The rule establishes that charges must occur outside the INSS, with alternatives like direct payment.

In practice, the associative link will no longer have automatic deductions from the benefit and will depend on an external channel.

Undue Deductions Lead to Full Refund and a 30-Day Deadline for Reimbursement

The law provides for an objective response when irregular deductions occur in the benefit.

Upon identifying an undue deduction, whether from association fees or consigned credit, the beneficiary is entitled to a full refund of the amounts.

The reimbursement must be made by the associative entity or the financial institution responsible for the irregular deduction, within 30 days after notification or a final administrative decision.

Fraud Allows Seizure of Assets Based on Decree Law 3,240 of 1941

The fight against irregularities gains a heavier instrument.

The Law 15,327 of 2026 amends the Decree Law 3,240 of 1941, allowing the seizure of assets in cases of offenses related to undue deductions from INSS benefits.

The measure may affect the assets of the investigated party and also property transferred to third parties or linked to legal entities used to sustain the irregularities.

Benefits Are Blocked for New Consigned Loans and Require Unblocking via Biometrics or Qualified Signature

Consigned credit now operates with an automatic entry block.

All benefits are blocked for new transactions, requiring prior, personal, and specific authorization for each benefit.

Unblocking must occur via biometrics or qualified electronic signature.

After each operation, the benefit remains blocked, and contracting via power of attorney or telephone is prohibited.

LGPD Gains Strength in the INSS and Vetoes Active Search and Direct Reimbursement by the Autarchy

The law reinforces the application of LGPD in the INSS environment, with clearer rules on the handling of insured individuals’ information.

There is also a provision for express communication about unauthorized data sharing.

Among the vetoes, provisions requiring active searches for beneficiaries harmed by undue deductions and sections allowing direct reimbursement by the INSS, with subsequent charges to the responsible entities, were excluded.

The provision transferring to the CMN the definition of maximum interest rates for consigned loans was also vetoed, along with rules mandating biometric structures in all face-to-face service units and disconnected transitional devices.

The Law 15,327 of 2026 eliminates automatic associative deductions from the INSS benefit and imposes a stricter safeguard for new consigned operations.

With full refunds, a 30-day deadline for reimbursements, and tightened controls, protection for retirees and pensioners will rely less on automatic charges and more on direct and verifiable authorization.